Last fall, we highlighted the Federal Reserve’s (Fed) problem of fighting inflation in the face of loosening fiscal policy. In 2023, it is evident the Fed will be in a different position as it fights inflation by both tightening fiscal policy and, in a weird twist, no longer fighting itself. Entering this period of triple tightening is likely to be a key step in fighting inflation. We define triple tightening as the Fed raising interest rates, the Fed’s balance sheet shrinking, and reduction in fiscal programs to recipients. The interaction of all three should have an amplifying impact on inflation and possibly some other consequences.

Federal Reserve Raising Rates. In March of 2022, the Fed began a series of eight federal funds rate increases that raised the overnight rate from 0.08% to the current 4.57%. By simply turning on the TV, an almost never-ending stream of experts were talking about higher rates and the inflation fighting process. We would make two points. First, in early March of 2023, the market is realizing the Fed is serious about “higher for longer,” which means rates are likely to continue to increase and stay at these higher levels through 2023. Second, raising rates has a delayed impact on the economy and inflation, such that there is a 9 to 12 month lag. Thus, most of the impact from the rate increases in 2022 are just beginning to be felt in early 2023. The Fed has effectively used raising interest rates to curb inflation in the past.

Federal Reserve Shrinking Its Balance Sheet. To control interest rates, the Fed has the ability to enter the market and purchase government-backed securities and issue Federal Reserve Liabilities, which is a fancy word for dollars. That is why at the top of a dollar bill it reads “Federal Reserve Note.” To a large extent, the Fed makes this market by increasing the amount of dollars, thus lowering rates, or lowering the amount of dollars, thus increasing rates.

Until 2010, the Fed’s balance sheet had never been greater than 16% of gross domestic product (GDP). The quantitative easing following the Great Recession in 2008-2009 saw the Federal Reserve greatly expand the money supply, and then the COVID crisis resulted in even more expansion. In April 2022, the Fed’s balance sheet was almost $9 trillion, or 35% of GDP. For our purposes, it is enough to simply understand that there has been a large amount of money in the U.S. financial system for over a decade.

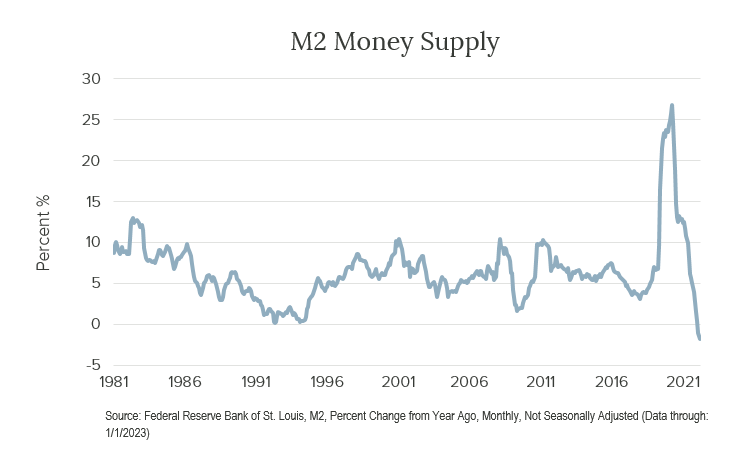

Now that the Fed has started to shrink its balance sheet, it could have an outsized impact on the already aggressive rate increases discussed above. Below is a chart that shows the growth in the money supply (M2). For the first time since October 1929 (pre-data below), the money supply in the United States is in decline. Moreover, the Fed has only started decreasing its balance sheet, reducing it by ~$625 billion since April of 2022. Chairman Powell’s goals are to reduce the balance sheet by about $1 trillion annually, while still maintaining an “ample reserves regime.” A normalized balance sheet is not expected (i.e. a reduction of $4 trillion), but it appears this will be a multi-year process.

Tightening of Fiscal Policy. Through legislative expirations, three programs could expire over the next several months that would result in the tightening of fiscal policy, especially impacting lower income consumers.

- Medicaid. Congress enacted additional payments to the states for Medicaid to help offset the increased medical spending during COVID. These payments sunset from a 6.2% boost in the first quarter of 2023 to 1.5% in the fourth, resulting in a $30 billion monthly drag by the end of 2023.

- SNAP. To ensure food safety during COVID, there was a similar increase in SNAP (Supplemental Nutrition Assistance Program). This increase begins to roll off in March 2023, and the expected impact is ~$30B per month by the end of this year.

- Student Loans. While the outcome is less certain, the Student Loan Repayment plan is scheduled to begin rolling off in September of this year, resulting in a $20 billion monthly drag by the end of the year, as standout loan borrowers began repaying loans that have been in deferral mode.

All in, these three programs represent the equivalent of ~$960 billion in lower spend over a rolling two-year period. If the policies are not replaced or refunded by another means, it could reduce GDP in the 2.5%-3.5% range over the course of 2023 and 2024, everything else being equal.

In this environment, we believe it is especially timely to focus on quality. Companies with strong balance sheets are positioned to weather difficult economic conditions. Companies with significant and dependable cash flow have an advantage in tightening financial environments. At Crawford, we have helped our clients survive the ups and downs of the stock market for over 40 years with quality, dividend-paying stocks as the backbone to their portfolios. We believe this strategy should survive, even in a triple tightening environment.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-052

The Bond Market vs. the Fed

There is currently a dichotomy between the Federal Reserve’s (Fed) actions and the bond market’s behavior.

Why Are So Many Gamblers Looking to Be Zeroed Out?

Our process and these companies weren’t built in a day, and serious investors should remember that wealth rarely comes from short-sighted endeavors.

Stocks: Rent or Own?

Today, many are effectively “renting” stocks in an attempt to create short-term trading gains, rather than owning equities for long-term total investment return.