Many investors have likely heard the name Blackstone the last few years. Blackstone is one of the largest commercial real estate investors in the world. Recently, there have been a lot of frustrated investors within their largest “non-traded” REIT vehicle known as “BREIT,” as withdrawals of the fund were limited to just 2% of NAV (Net Asset Value) due to difficult market conditions including higher interest rates. With the promises of steady income and capital appreciation, investors essentially gave up liquidity by investing in the largest non-traded REIT in history.

At Crawford, we offer a way to invest in the same high-quality property types that Blackstone acquires AND have daily liquidity. We created the Crawford Real Estate strategy to participate in the same trends that Blackstone seeks to capitalize on with one important caveat. The caveat: we offer liquidity as we invest in the highest-quality, liquid, publicly traded REITs in the market. Ironically, Blackstone and other private equity companies have been so enamored with high-quality, publicly traded REITs, a few of our strategy’s holdings have been acquired, including PS Business Parks and Switch. Blackstone has also acquired peers of our core data center holding: Equinix and the only other lab space REIT than our core holding: Alexandria.

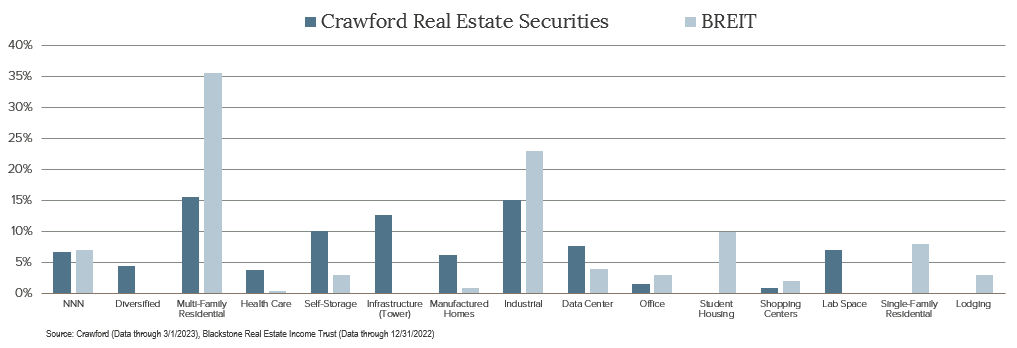

As you can see below, the Crawford REIT holdings offer greater diversification but are heavily weighted toward the same property types that Blackstone favors. We believe this serves us well as the largest private equity players will indeed need more acquisitions in the future to grow, which could help serve as a floor on valuations for our holdings. Meanwhile, we are observing improving fundamentals and receiving steady dividend income.

At Crawford, we will continue to invest in publicly traded real estate with a private equity mindset, while offering something Blackstone and others cannot provide everyone today: liquidity.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The companies identified above are examples of a holding and is subject to change without notice. These companies have been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment recommendations or decisions we make in the future will be profitable.

CRA-23-053

The Incredible Shrinking P/E Ratio

The decline in share prices combined with stable earnings projections means Price to Earnings ratios have declined significantly over the past six months.

Low Margin for Error

As profit margins regress toward the mean, we believe investors should be focused on companies with strong balance sheets and excess free cash flow.

Expect the Unexpected

At Crawford, our strategies are engineered to embrace the reality of uncertainty. We prefer to pursue an active management process that seeks diversification across sectors, industries, and position sizes.