The distinction between gambling and investing is often lost, especially in today’s fast-paced society. While both activities require an initial outlay of capital, we view three key distinctions between gambling and investing.

- Edge. We try to be “The House.” In investing, our internal research department searches for what we believe are strong, dependable businesses that generate excess cash. Think of the excess cash and reinvestment of that cash as the investor’s advantage in being “The House” and tilting the odds in their favor. On a long enough timeline, gamblers will always lose because the odds are against them. Exploiting behavioral biases and owning quality enables Crawford to earn attractive returns with lower risk.

- Duration. We make decisions for our clients over a multi-year horizon period. The ability for companies to compound profits and reinvest over a longer period is key to growing wealth. This most-often cited idea is a foundational principle for successful investing. We consider a long-term investment horizon as a “time arbitrage.”

- Income. We invest in companies that pay a dividend, so our clients receive income over the investment period. The dividends help support current income needs, increase long-term returns, and dampen any knee-jerk reactions during downturns in the equity markets. Companies that effectively allocate capital, such as dividend-payers, outperform non-dividend-payers over time.

Currently in the market, the casino is open and thriving in the proliferation of zero day options. An option is a contract between two parties where the purchaser has the right to buy or sell an underlying security at a specific price on or before a certain date. A zero day option lasts only for the day it was purchased, thus the timeline for potential profit is very short, measured in hours. The prices on these contracts are in a very narrow range, typically a difference of 1% or less from the current price. To summarize, lots of traders, along with some gamblers, are making bets that a stock or stock index will move by a large amount in a single day.

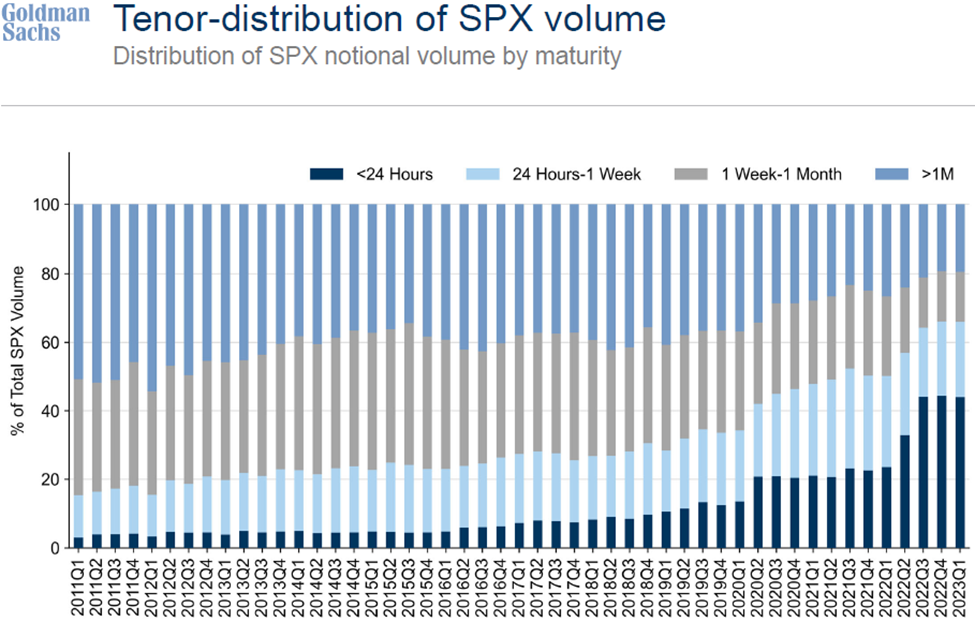

According to a recent report from Goldman Sachs, over the three months ending February 2023, there was at least $400 billion traded daily on zero day options. As seen below, this is now accounting for over 40% of the volume for S&P 500 options contracts, the most heavily traded index.

Why has this happened? Sophisticated investors including hedge funds began to notice a mispricing in options. The market volatility during early 2020 and again in mid-2022 increased, resulting in the price of very short options being too cheap. This is because the large market swings in a single day produced enough gains to more than compensate for losses when other options expired worthless. These sophisticated investors found an edge and exploited it.

Why does this matter? Trends of this nature are rarely sustainable. The success of pioneering investors typically gets competed away very quickly. Fads such as this typically make outsized gains for the initial traders, but follow-on gamblers are stuck holding ever increasing losses as the strategy begins to fail. There have been periods in the past where unusual options strategies have moved the equity market sharply in a small window.

In February of 2018, the market experienced what is referred to as “Volmageddon” with the S&P 500 selling off 12% in only ten days. Speculators found a virtuous feedback loop of buying inverse volatility exchange traded funds, selling options on the VIX, and entering into large complex options trades that lowered volatility. On January 29, 2018, these speculative bets began to rapidly unwind, and it took the S&P 500 index about six months to recover. Volmageddon did not damage the markets, as most investors looked through this volatile period. But the last gamblers out the door locked in large losses.

It is impossible to know how the increase in zero day options will impact the equity markets and your portfolio. At Crawford, we have helped our clients survive the ups and downs of the market for over 40 years with quality, dividend-paying stocks as the backbone to their portfolios. Our rigorous process identifies companies with an “edge” of generating excess cash and reinvesting that cash in a virtual cycle that should, over time, raise the dividend and increase the share price. Our process and these companies weren’t built in a day, and serious investors should remember that wealth rarely comes from short-sighted endeavors.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-054

Always Higher, Never Lower

The projected deadline for a government shutdown is June 1, as tax receipts collected through April 15, 2023 were slightly lower than originally forecasted. Why should this be watched more closely than usual?

Low Margin for Error

As profit margins regress toward the mean, we believe investors should be focused on companies with strong balance sheets and excess free cash flow.

Can Your Portfolio Withstand Divided Government?

In a period where fiscal policy and monetary policy seem to be at odds, we believe investors should participate in the market via high-quality companies.