In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- In view of the many unknowns and lack of predictability in the current fiscal policy climate, our Bond Policy remains defensive and unchanged.

- Our outlook is cautious as the probability of recession has increased at-the-margin.

- We will continue to maintain our defensive positioning, including an above-benchmark allocation to defensive corporate industry sectors, agency, and municipal credits.

- We will continue to manage yield curve positioning and consequent duration toward the longer/higher end of our intermediate range.

- This has allowed for the capture of higher yields and positioning for total return potential with the increased probability of lower interest rates at a future point in the cycle.

- We view current Municipal yield levels to be very attractive on an absolute and relative basis.

- We look for the traditional summer calendar cycle of negative net issuance (more redemptions than new issuance) to have a positive effect on prices and relative value over the June through August period.

- If the U.S. 10-year Treasury yield moves appreciably above 4.50% due to effects associated with policy implementation, we will look to extend a portion of our Core bond strategy toward the longer-end of our 15-year maximum maturity spectrum into Government and/or Municipal credit.

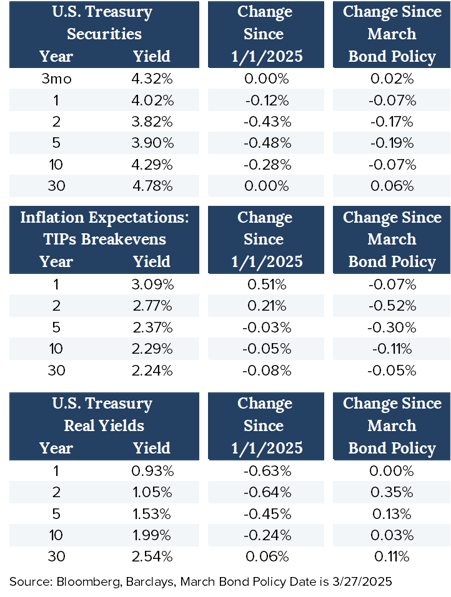

Treasury Yields as of 5/8/2025

- U.S. Treasury security yields fell across most of the curve since our March Bond Policy meeting, primarily driven by declines in market-driven inflation expectations (represented by TIPs breakevens).

- Real yields were mixed but generally higher across most of the curve.

- Movement in breakevens and real yields both reflect reduced expectations for Fed rate cuts and higher term premium.

- After the May 7 Fed meeting, Fed Funds futures for year-end 2025 fell back to 2 cuts, having reached a high of 4 cuts after “Liberation Day” policy announcements.

- “Liberation Day” (April 2nd) magnified the uncertainty pervading the U.S. economic environment as the market interpreted the implications of what collectively amounted to a 23% tariff rate increase.

- It is difficult to project the impacts of tariffs with much precision due to the idiosyncrasies associated with each country, product, and service against which the tariff is being levied.

- For example, it is unknown who will ultimately absorb proportionate cost increases among the end consumer and the export provider.

- Generically, it is estimated the announced tariffs would raise approximately $400 Billion in revenue for the U.S. Government, making it the largest tax increase since the 1968 Revenue Act.

- Further, tariffs at their announced levels are expected to increase PCE prices 1.0% to 1.5% this year.

- On April 9th, a 90-day suspension of reciprocal tariffs against all countries except China (whose tariff rate was increased to 125%) was put in place, feeding the lack of predictability households and businesses need to plan and invest.

- The realignment of global trade will have long-term consequences on the U.S. Treasury market.

- It may ultimately increase the cost of financing as foreign investors migrate away from dollar-denominated assets.

- The Balance of Payments is an aggregation of U.S. international transactions comprised of the Current Account (measuring goods and services trade) and the Capital Account (measuring the flow of invested capital).

- The Current and Capital accounts must sum to zero, so if policy is aimed at reducing the goods trade deficit in the U.S., that will necessarily be offset with a reduction in foreign investment capital, i.e., less foreign money buying Treasuries. This may lead to higher yields.

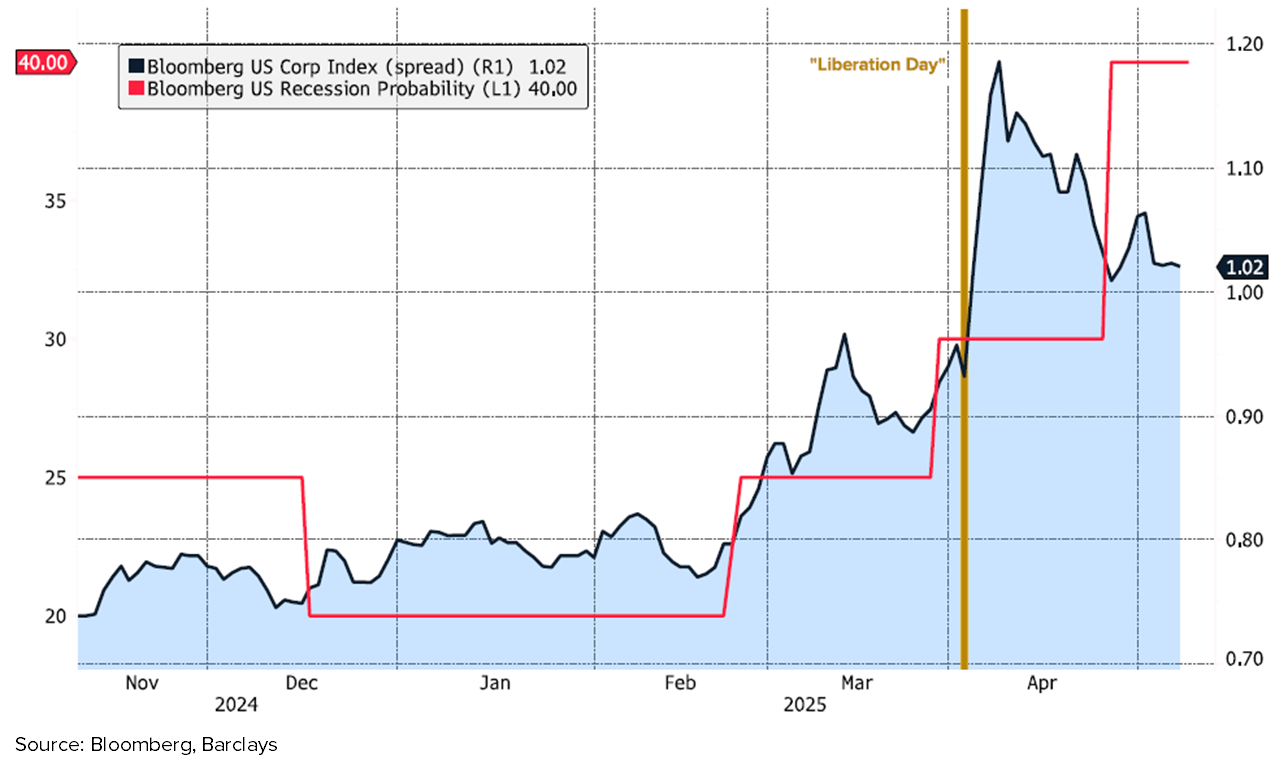

Investment Grade Corporate Bond Market

- The Bloomberg U.S. Recession Probability displays the median forecasted probability of recession. Forecasts are derived from the latest monthly & quarterly surveys conducted by Bloomberg and from forecasts submitted by various banks.

- Despite moving meaningfully higher off a low, rangebound level, investment-grade corporate yield spreads remain relatively “tight” in view of the increased potential for recession driven by tariff implementation.

- Absolute yield levels continue to support overall demand, but recent fund outflows demonstrate a weakening in retail investor sentiment.

- Given current policy implementation and the increased potential for negative economic effects, corporate spread levels are being considered subject to a “Gray Swan” event, which is defined as a shock that is predictable in theory but ignored until it occurs.

- In view of present circumstances, we will continue to maintain our defensive positioning, including an above benchmark allocation to defensive corporate industry sectors, agency, and municipal credits.

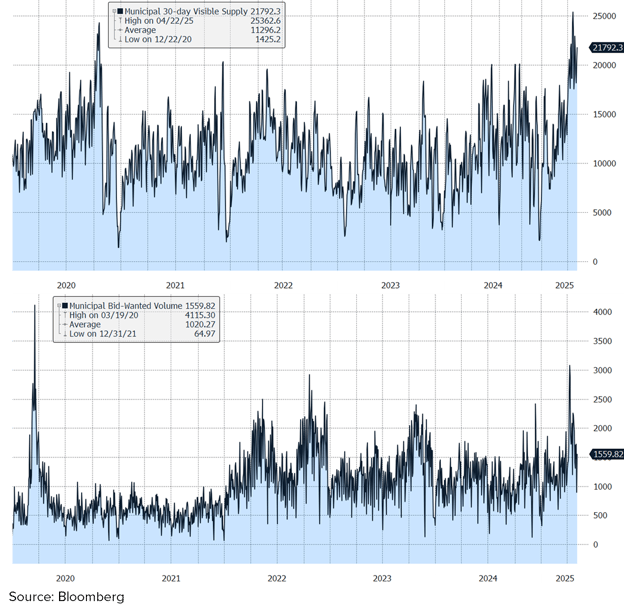

Municipal Bond Market as of 3/27/2025

- Over the first 2 weeks of April the Municipal Bond market experienced one of the most volatile periods in recent history.

- In addition to general bond market upheaval resulting from announced tariff policy intentions, municipal bonds suffered additional strain due to a heavy new issue calendar and seasonal investor selling to meet tax liabilities.

- Municipal bond “AAA” scale yields moved higher across the curve between March and May Bond Policy meetings.

- Recent upward pressure on yields has been driven by:

- Heavy new issue supply, including the highest volume for the month of April since 2008 and a year-to-date new issue supply volume record. Net supply pressure on yields is expected to last through May.

- Retail fund outflows reached levels last seen during the rate hike cycle of 2022, driven by tax-related (calendar-driven) selling and nervousness surrounding the implications of tariff policy and Federal cost cutting. Redemptions produced an escalation in Bid-Wanted volume to Covid crisis levels.

- Combined, these elements pushed the yield spreads and ratios to levels last seen in late 2023.

- Performance suffered relative to other high-grade bond sectors: lower rated municipal bonds underperformed higher quality and longer maturities underperformed shorter tenors.

- We view current Municipal yield levels to be very attractive on an absolute and relative basis.

- We look for the traditional summer calendar cycle of negative net issuance (more redemptions than new issuance) to have a positive effect on prices and relative value over the June through August period.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-2505-2

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.