Crawford Investment Counsel (Crawford) is focused on investing in what we believe to be high-quality securities. The dividend is an attractive and necessary feature of our investment process. This is because we believe income, or yield, is a factor that gives value to stocks, and perhaps most importantly, because we think dividends and quality are inexorably linked. While we like dividends, we particularly favor those companies with consistent records of increasing payouts. Real estate investment trusts (REITs) are not traditional common stocks, but many of the companies in this area fit very well with our investment priorities and methodology.

We feel the ability to invest in real estate while benefitting from the liquidity of the stock market is an attractive feature. And, the significant size of the underlying portfolios enables a high level of diversification within a particular property type.

A real estate investment trust (REIT) is a corporate entity, public or private, that owns, operates, and develops commercial real estate assets (CRE). REITs are required to distribute 90% or more of their taxable income to investors in order to maintain their tax-favored REIT status. A key distinction of REITs is the tax treatment on dividends. Currently, REIT dividends are passed directly to the investor and avoid the double taxation faced by common stocks, which has historically allowed REITs to have relatively higher dividend yields than common stocks. However, there is one caveat: REIT dividends are taxed at ordinary income tax rates versus 15-20% for common stocks. This tax treatment favors that REITs be held in tax-deferred accounts whenever possible.

History: REITs have existed since 1959 with several tax code changes along the way. The modern REIT era began in the early ‘90s with Kimco Realty’s IPO, followed in 1992 by six more, including Taubman, the first Umbrella Partnership REIT (UPREIT) structure. The UPREIT model was critical because it allowed real estate partnerships to contribute assets to the REIT in exchange for units of the new REIT partnership without triggering an immediate tax liability. This new structure set the stage for a transformative year in 1993, with 45 REIT IPOs, and another 43 in 1994. There would be an additional 59 IPOs the remainder of the decade. The listed REIT industry’s equity market capitalization grew from $16 billion at the end of 1992 to $125 billion at the close of 1999. Today, REITs own over $2 trillion of CRE with over $1 trillion in market capitalization, representing 15-20% of the overall U.S. property market. This growth led to REITs getting their own Global Industry Classification Standard (GICS) sector in 2016, becoming the 11th S&P 500 sector.

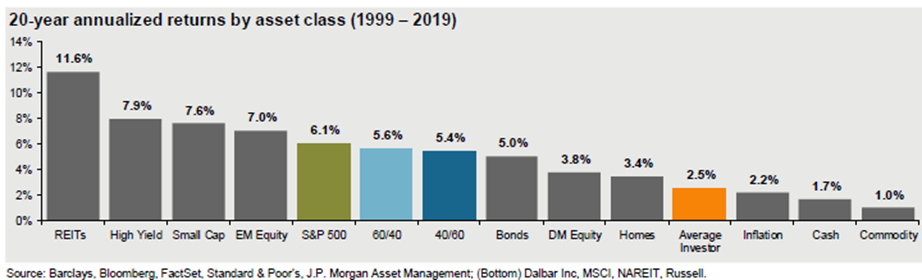

Track Record: The REIT industry’s historical return has led to increased interest in both private real estate and publicly traded REITs. According to J.P. Morgan, the REIT sector’s annualized 20-year return has beaten stocks, bonds, and commodities. We believe this is due to a combination of economies of scale and pricing power, or the ability to increase rents in excess of inflation over time. Secondarily, the average real estate capital structure employs more debt than common stock, which increases returns on capital when coupled with pricing power. These factors have increased interest in higher-yielding assets such as CRE.

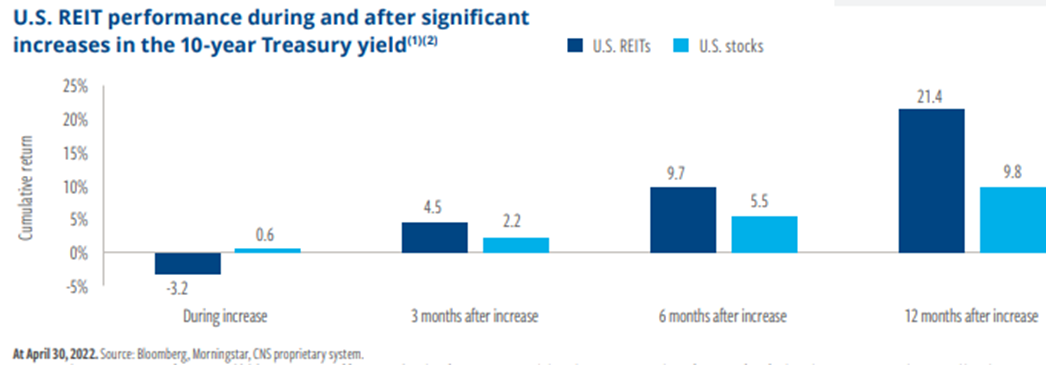

REITs and Interest Rates: According to Cohen and Steers, REITs have historically outperformed stocks 3-12 months after significant increases in the U.S. 10-year bond, which has occurred in 2022.

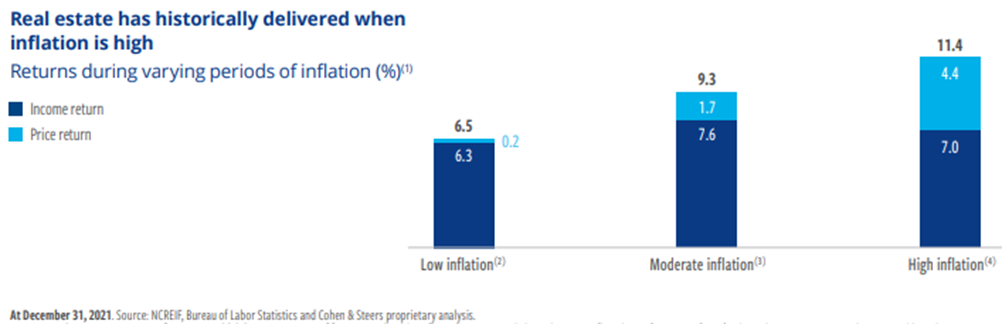

REITs and Inflation: REITs have historically done quite well during inflationary periods. We believe this is due to several factors including the ability to increase rents, built-in annual rent escalators, and the use of fixed rate debt. These factors allow REITs to pass through inflation while keeping their financing costs constant. In addition, higher inflation increases the cost to develop new buildings and thereby reduces new competitive supply in many cases.

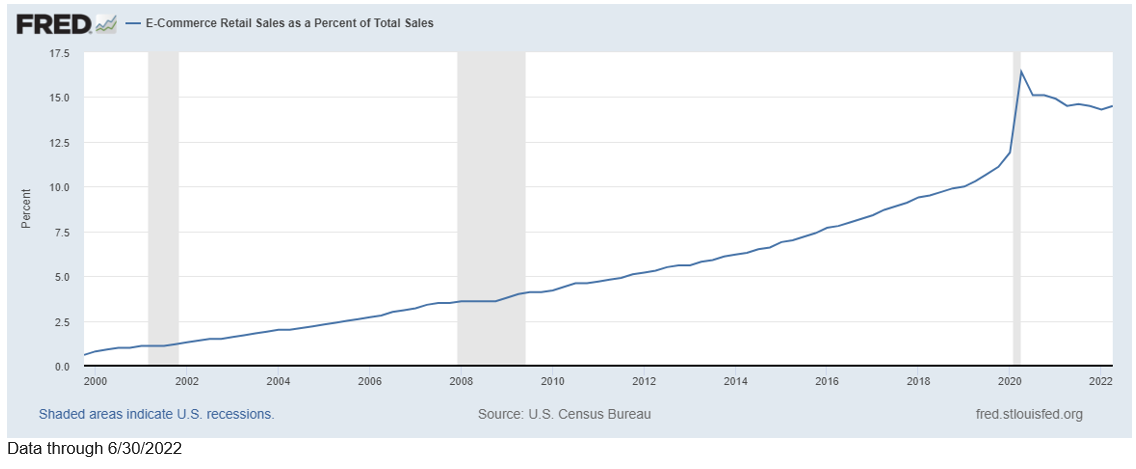

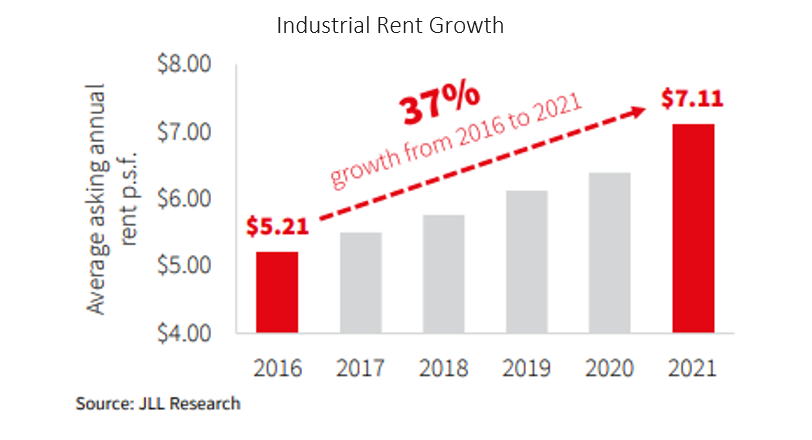

Coming out of the 2008 recession, most of the REIT market moved up in tandem with the broader stock market without much variation between property types. In fact, mall and retail REITs were top performers and a large part of market capitalization-weighted indices up until 2016. That trend changed materially in 2016, with the Amazon effect taking hold, creating distinct winners and losers. The incredible rise in e-commerce, which continues to accelerate, has directly benefited Industrial REITs at the expense of retail real estate. The secular trends in e-commerce accelerated in 2020 as a result of Covid lockdowns, and e-commerce sales spiked to 16% of total U.S. sales in 2020, a record. We believe this trend could have permanent implications for industrial and retail-focused real estate. Industrial asking rents in the U.S. alone have increased 37% since 2016 due to record low vacancy rates of ~3% nationally.

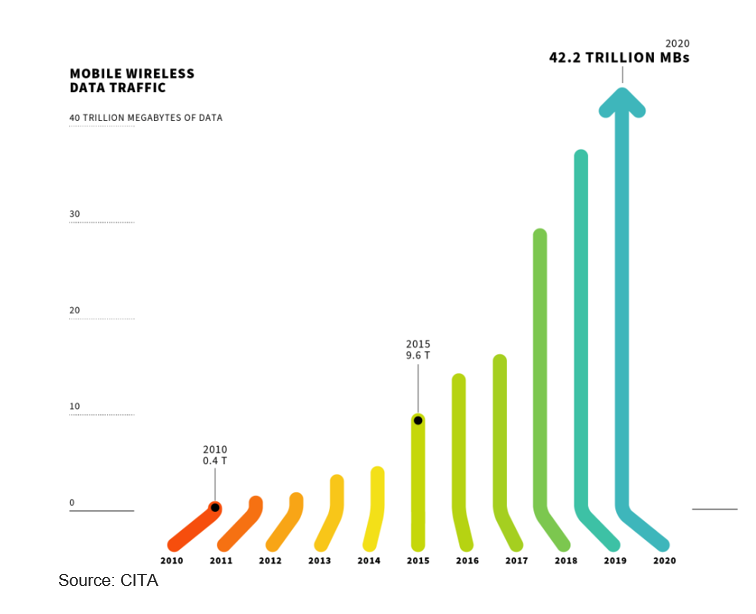

Towers and Data Centers: Tower infrastructure is the backbone of wireless data traffic, which has seen a steep change since 2017 according to the Cellular Telecommunications and Internet Association (CTIA). In 2020, 417,215 cell sites were in use, +19% since our 2018 report. Tower REITs are clear beneficiaries in the race to 5G supremacy. From 2017-2020, over $116 billion of spectrum was auctioned by the FCC. This spectrum is put to use on cell towers and data centers. Unlimited data plans have only reinforced the demand for space on towers, which drove $27.4 billion in capital investment by the wireless industry in 2018.

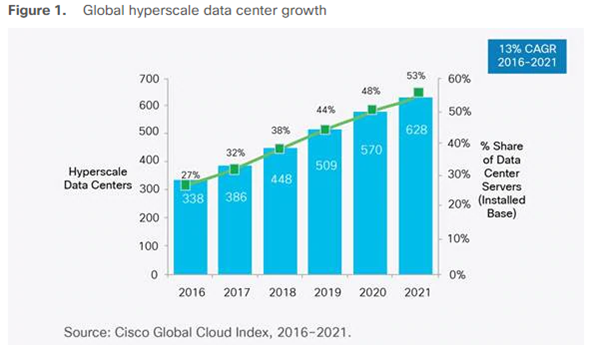

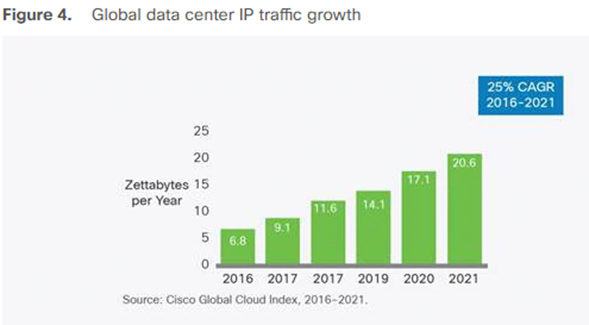

Data centers are also seeing explosive growth as cloud adoption becomes mainstream. According to Cisco, data center growth was expected to increase 13% through 2021. While initially alarming, this new supply is mitigated by the estimated 25% growth in IP traffic over the same period. Private equity firms and Tower REITs have also noticed the growth in cloud services. In 2022 alone, all four small capitalization data center REITs were acquired and included CoreSite Realty, QTS Realty Trust, Cyrus One, and Switch Inc. The only two remaining data center REITs are Equinix and Digital Realty.

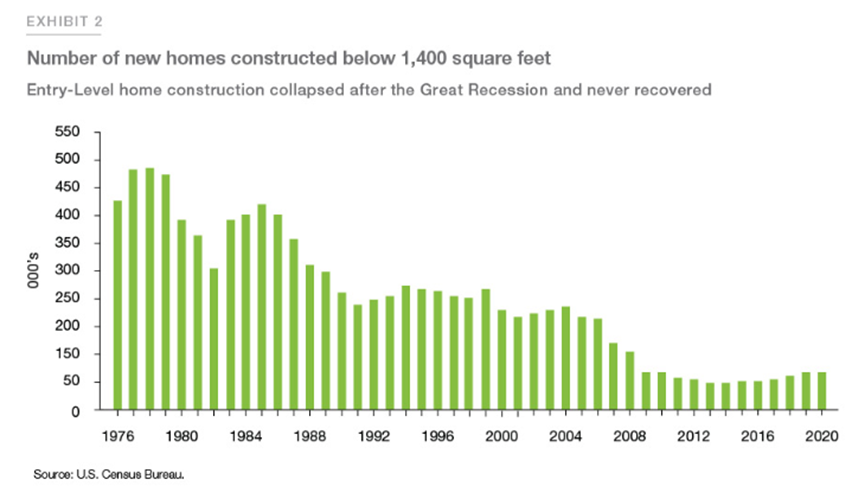

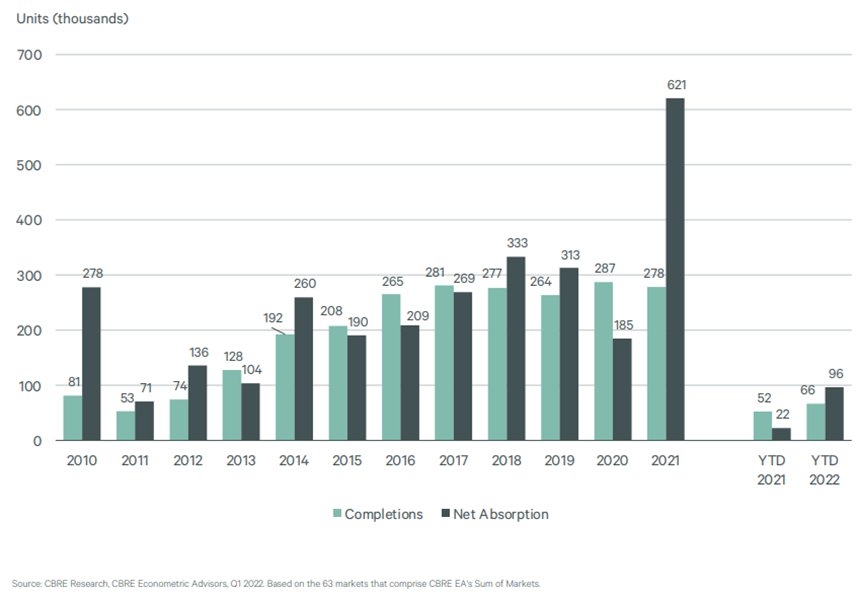

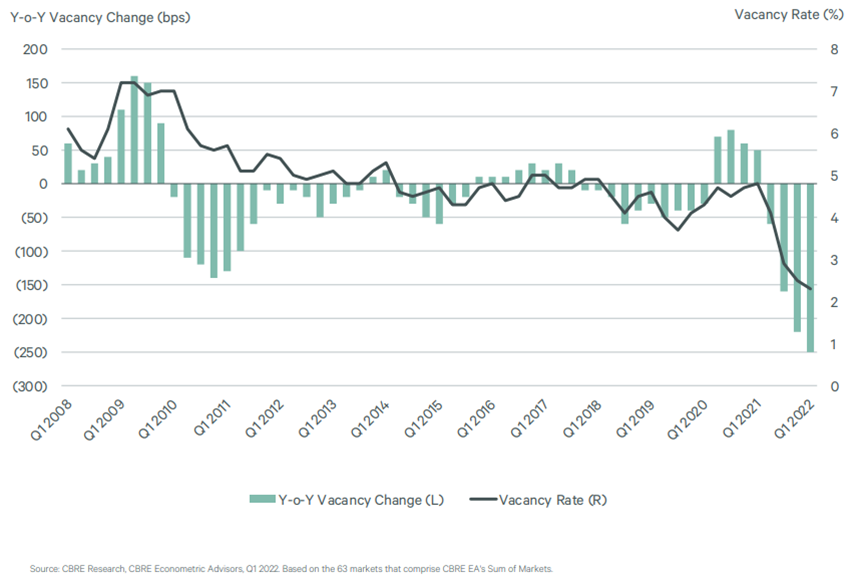

Multi-Family: The multi-family (apartment) sector is playing a major role in combatting the U.S. housing shortage. According to Freddie Mac, the U.S. is short 3.8 million housing units needed to keep up with household formation. The 2008 housing bubble is partly to blame, but so are labor availability, regulation, and other cost inflation.

This unfortunate environment has greatly benefited apartment owners and REITs, particularly post-Covid. In fact, 2021 was a record absorption year versus apartment development completions due to millennials entering the workforce as well as going from having a roommate to renting their own space. This has resulted in record-low vacancies and record-high rents. Given this backdrop, we intend to be overweight apartment REITs for the foreseeable future.

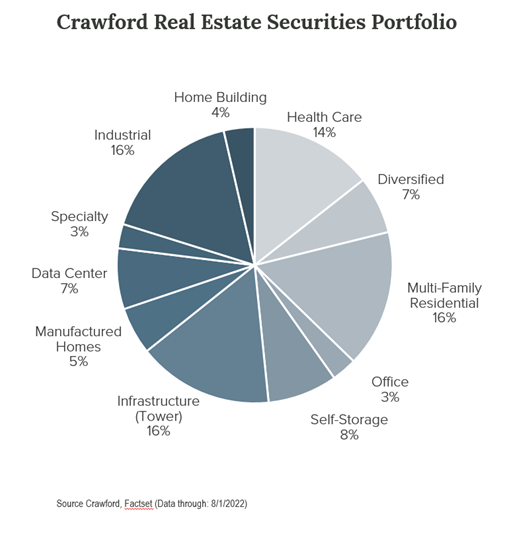

Crawford’s Real Estate strategy is to participate in the aforementioned secular trends while continuing to be mindful of the two primary factors that negatively impact real estate returns: new supply and leverage. Our holdings are diversified by property type and specifically weighted towards stable and consistent rent growth. These characteristics lead us to be overweight cell towers, apartments, industrial, and self-storage. Our healthcare exposure is not exposed to government reimbursements and is confined to premier, class A lab space, medical office, and senior housing.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-226

Rx for the Long Run

The stock market is a complex system. Millions of different individuals with different points of view come together to set pricing on publicly traded businesses.

Stock Rating System

We utilize a formal, subjective stock rating system to communicate how we are evaluating individual investment opportunities.

Watching & Waiting: The Return to the 2% World?

If the 2% world is considered to be the normal world, why are we so far off the mark, and what are the underlying conditions that would make it normal again?