Free cash flow is a key concept in business and financial arenas. It can be defined as the actual cash generated from operating a business over a period of time minus investments in capital expenditures. Cash flow is the lifeblood of companies, and it provides the internal resources necessary to consistently self-fund reinvestment for growth. For public companies, it also ideally enables some return of capital to shareholders through dividends and (in some cases) share repurchase.

At Crawford Investment Counsel (Crawford), we seek to invest in high-quality companies. The level of consistency in free cash flow generation is an important criteria in our quality screening process, along with other attributes such as high profitability and conservative balance sheet management. Many lower-quality companies currently face significant resource drain from a combination of potential recession and overreliance on external borrowing at previously low, but now relatively high, rates of interest. We expect the higher-quality companies we own to benefit from this more difficult operating environment due to their internal funding advantage.

As our experienced research team evaluates prospective stocks for long-term ownership, there are several investment scenarios we gravitate toward. The most common investment case involves businesses with historically strong free cash flow which are currently trading at discounted relative valuations due to temporary cash flow weakness. In these scenarios, if we believe the below-historical-trend cash flow will revert within a year or two, we view the company as an attractive investment opportunity. Valuation could very well correspond with the upward normalization of cash flow.

A less frequent but potentially more powerful investment opportunity emerges when our extensive due diligence suggests a company is approaching a transition to structurally higher cash flow generation. This generally happens as a function of successful business evolution, often resulting from permanent change. An example of this could be the divestiture of a volatile and lower cash flow generating division and possible replacement through acquiring a stronger one. If this process is successful, the reshaped company is often able to grow profit more rapidly, meaning investors will value it more richly over time.

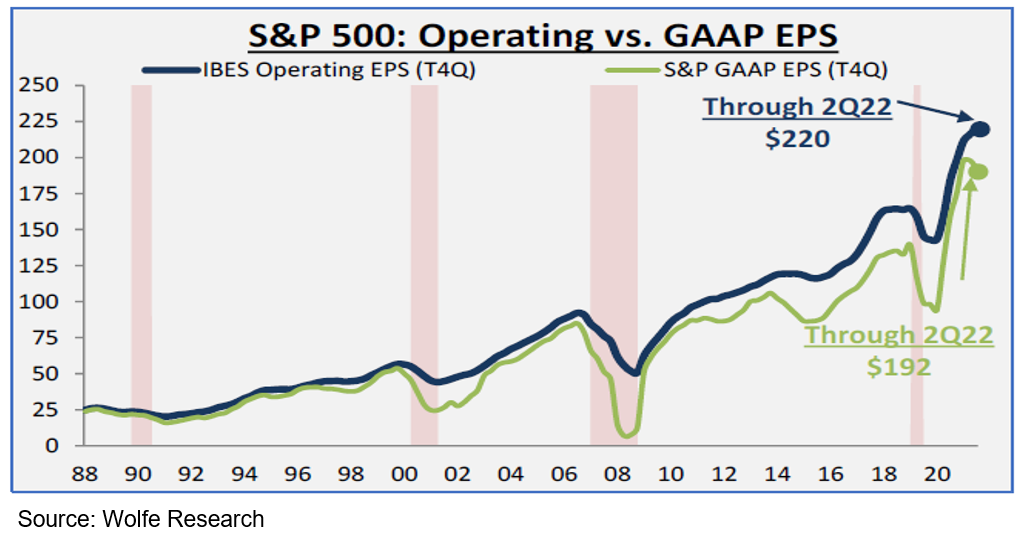

Confronted with a complex world, it is human nature to try to simplify how we process information and communicate ideas: to convert cumbersome messages into sound bites. This also applies to stock valuations. As a result, Price-to-Earnings- or P/E-based valuation frameworks dominate the general media and financial news. However, given the rise of “operating” EPS over time with many non-standard accounting adjustments (creating a more than 10% higher level of earnings than GAAP recently), P/E ratios have become less comparable across companies and far less informative of underlying free cash flow dynamics.

For this reason and since substantial free cash flow (to reinvest for growth and return capital to shareholders) is a key component of our investment approach, we believe valuation metrics that directly incorporate cash flow generation are often more enlightening. In order to mitigate investment risk by owning businesses with stronger balance sheets, we also pay attention to Enterprise Value (EV), which represents a company’s market capitalization plus total debt and minus cash and cash equivalents. EV takes into account a company’s debt and cash levels in addition to its stock price, ultimately relating those values to the firm’s cash profitability. Our preferred valuation metric to combine the cash flow and strong balance sheet characteristics of quality is forward-looking EV/Free Cash Flow. Applicable to most sectors, we believe EV/Free Cash Flow multiples can serve as a great yardstick as to whether a company is over- or undervalued when combined with our fundamental, bottom-up company due diligence.

Many of the companies we invest in generate better than average free cash flow and maintain less debt-laden balance sheets, such that they will generally trade at lower relative free cash flow and EV-based multiples than relative P/Es. This creates opportunities over time to invest at favorable entry points as other investors perceive valuation to be higher than we do. In fact, we would argue that a durable market inefficiency exists because investors consistently underestimate the multi-year growth potential of high cash flow generation companies from deploying internal resources into new profit enhancement projects and/or returning an increasing level of capital to shareholders.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-22-275

Bursting the Bubble: Speculative Fervor Then & Now

Long-term success comes from staying disciplined, avoiding speculative frenzies, and focusing on remaining invested in high-quality investments that can weather the test of time.

The State of the Consumer

At Crawford Investment Counsel (Crawford), we believe the financial condition of the U.S. consumer has rarely been better.

Example of Investment Thesis: AstraZeneca

In the first installment of the Company Fundamental Investment Series, Senior Research Analyst and Director of Core Equity Strategy, Frank Pinkerton, walks us through an investments thesis.