We have noted that 2022 has been a year of uncertainty. Investors have been forced to face changing conditions in both the capital markets and the underlying economy. We see that this uncertainty is yielding to some identifiable trends that are dominating investor preferences and permeating economic discussions. We feel the stock market volatility and downdraft reflect both an uncertain future and a picture that has some potentially negative implications. Today, there is an absence of a consensus view of our economic future because it is unclear whether changing dynamics are of a shorter or longer-term nature. As a means of trying to move beyond uncertainty to a more convicted view of what lies ahead, we are focusing on a number of dynamics that all have important implications for profit margins, corporate earnings, and ultimately, stock and bond prices. We are reviewing these changes within the context of pendulum shifts and are considering how formative they may be in shaping the longer-term course of the economic and business environment.

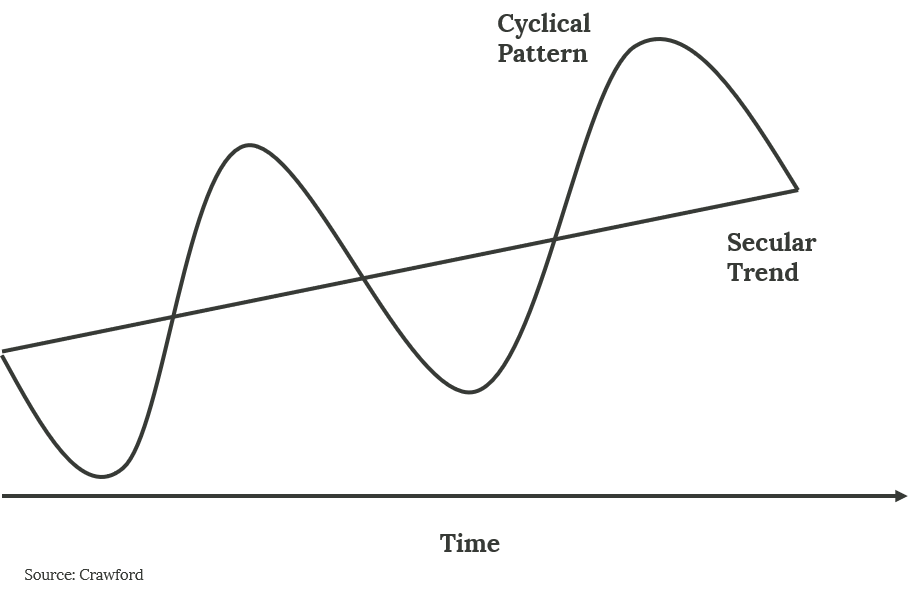

The pendulum idiom can be helpful when considering change. A pendulum swings one way until its momentum is exhausted, reverses, gains momentum, and then repeats the process over and over again. The concept goes back to Galileo and refers to the force of gravity, kinetic energy, and acquired momentum of a swinging pendulum. Perfect equilibrium is short-lived. We can use the concept of pendulum shifts within economic and business conditions as we attempt to determine when trends are about to exhaust themselves and reverse course. This can be likened to the subject of secular versus cyclical trends.

A secular, or long-running trend, can contain cyclical, or short-term trends, within it. The difficulty lies in determining the difference between the two. From an investment standpoint, aligning with secular trends is more important, for they lend themselves to better outcomes and are consistent with long- term investing. It can be helpful, however, to be aware of cyclical trends, for they sometimes turn into secular trends, or pendulum shifts.

Let’s review some of the changes occurring with an eye to their nature as either cyclical or secular. Our goal in examining these trends is to move as best we can from uncertainty to clarity.

INFLATION AND INTEREST RATES. The long-term trend toward low inflation and interest rates, we feel, has been the most prominent secular trend of our time as investors. This trend powered decades of bull markets in both stocks and bonds. Now, after declining to all-time lows during the pandemic, interest rates and inflation have risen sharply. Inflation at over 8% is at a 42-year high, and interest rates have inflected as the Federal Reserve has made a dramatic pivot to a materially higher federal funds rate. This inflection point in interest rates has many proclaiming the end of the secular trend of low interest rates. A pendulum shift in inflation and interest rates would imply that we are headed for a significant change of direction over the longer term. We believe it is premature to assume the end of the secular trend of low inflation, but we are certainly experiencing a cyclical increase.

LABOR VERSUS BUSINESS. In a recent piece entitled The Corporate Juggernaut, Can it be Stopped?, we concluded that business is likely to maintain its dominance over labor, due primarily to the secular trends in monopoly and monopsony. However, there have been recent stirrings that suggest a reversal toward labor, most notably wage pressures and high profile unionization moves. Widespread labor shortages imply greater leverage by labor and a potential shift in the balance of power. Whether secular or cyclical, the issue of labor momentum will be one for business to confront.

DEMAND FOR GOODS AND SERVICES. There is no question that there has been a major shift in the last year or so toward more purchases of goods and fewer purchases of services. We see that this change was clearly brought on by the shutdowns during the Covid extremes, combined with aggressive fiscal stimulus that bolstered purchasing power (demand). This has all created some distortions within the economy resulting in shortages and the ability for suppliers of goods to raise prices. We are now seeing consumer behavior re-normalize with the share of goods purchases declining and services spending increasing.

GLOBALIZATION VERSUS ONSHORING. Globalization, in its narrow definition, refers to international trade and reliance on foreign sources of production because they can be produced cheaper. Again, due to Covid restrictions, geopolitics, and subsequent snarling of the supply chains from international sources, many believe that the long standing trend in globalization may be reversing. The thinking behind a pendulum shift in this area is logical, and businesses want to put themselves in a more secure position from a sourcing standpoint. The onshoring of production could produce a surge in capital spending, offsetting to some degree the negative aspects of global trade peaking some five or six years ago. Time will tell on this issue as more evidence develops, but we acknowledge the possibility of this to be a secular change underway.

We have highlighted four major trends that have at least experienced temporary change, and which may be in the process of a true pendulum shift. In the weeks ahead, we will be exploring these and many others in greater depth. It is too early to state with conviction that these trends are permanent, and therefore to what degree they will alter the longer-term picture for the economy and markets. We can say, however, that on balance, the trends that we have discussed are challenging for the corporate sector. Interest expense, while still reasonably low, is now higher, labor costs have presented a challenge, and real economic growth (adjusted for inflation) is slowing. We do not wish to imply that these are insurmountable issues for companies, but uncertainty is now yielding to an environment where things are not as favorable as they have been. All have implications for corporate profitability, and record margins are going to be pressured.

As we entered 2022, we were highlighting a number of excesses in the environment. It seemed reasonable at the time to be cautiously optimistic, but to invest in such a way that should the correction of these excesses become extreme we were protected as much as possible by the overall quality of the portfolios. Now, we see more clearly some of the challenges that businesses may confront from pendulum shifts in a number of areas. Just like investing for too many excesses, we believe the best way to move through a period of potential pendulum shifts is to be especially focused on balance sheet strength, profitability, and earnings consistency – all aspects that relate back to corporate quality as a dominant investment characteristic in the composition of the portfolio.

Please reference our related Podcast for more detail:

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-155

Exploiting Inefficiencies to Produce Alpha: Crawford Dividend Yield Strategy

Over most time periods, the Crawford Dividend Yield strategy’s results have been strong on an absolute, relative, and risk-adjusted basis.

Prevailing Through Challenges: Interview with Small Cap Manager

We are really pleased with our strategy’s recent outperformance, because there have been several underlying trends in the market working against us.

JNJ: Dividends and Divestitures

There are few stocks that have been held for 41 years at Crawford Investment Counsel. One is Johnson & Johnson (J&J).