Crawford Investment Counsel’s (Crawford) investment philosophy was born fifty years ago when investing in high-quality growth stocks or “nifty-fifty” type companies was the major market trend. One day during a portfolio review session, the firm’s founder, John Crawford, III, was asked by a client, “Where’s the yield?” After discussing this with members of the firm where he worked at the time, doing some research, and pondering it internally, John ultimately asked the client if they would rather focus on growth or yield within the portfolio. The question essentially asked the client to choose one or the other, to which the client responded, “Why not both?” It was from this conversation that the “growth and income” strategy Crawford was founded upon was launched.

John’s answer to this client’s request for both growth and income/yield marks the genesis of Crawford’s investment philosophy. Quality became non-negotiable, and valuation emphasized to a greater degree than it had been by “nifty-fifty” investors at the time. John set out on a quest for stocks that were down in price, paid a handsome yield, and increased their dividends consistently. A core belief was (and still is) that upward movement for the dividend reflects growth in intrinsic value, rising cash flow, and increased earnings per share. Fifty years and many market cycles later, the firm still embraces this overall investment mantra today, but with far more rigor, information, and resources behind the effort than ever before.

It is interesting to note that the period of time in which this strategy and philosophy was created was not entirely different from the economic and market circumstances today. As it is currently, inflation was on the rise. In the early 1970s, stocks were not cheap, and the economy was suffering from high energy prices which led to what we saw as some great opportunities in high-quality, blue chip stocks offering high levels of income and strong prospects for growth. Today, we observe a quite similar backdrop. We see that our philosophy was effective back then and it has proven successful since; we have no doubt it will continue to provide satisfactory outcomes for our investors.

Over time, the importance of the dividend, and more specifically, appreciation for what a stable, safe, and rising dividend might signal, became more and more ingrained in Crawford’s security selection process. The dividend quickly became a hallmark of quality for Crawford, and the firm’s investment philosophy was anchored with the dividend. This led to further work and discovery, ultimately resulting in a group of like-minded professionals pursuing differentiated investments on behalf of clients with a focus on what we like to call Dividend Integrity.

At Crawford, we define dividend integrity as simply the ability of a company to sustain and/or raise its dividends over time, consistently rewarding shareholders in the process. For Crawford, dividends are the initial indicator of quality. Once this criteria is satisfied, we move forward in our fundamental research process. We believe that the ability of a company to regularly pay and sustain dividends is often indicative of quality characteristics like balance sheet strength, consistent cash flows, low earnings variability, and high return on equity. Secondary attributes often include strong management teams, substantial market share positions, a business with low capital requirements, and sound capital allocation practices. Companies with all these attributes typically also have the internal fortitude to increase payments to shareholders over time.

For obvious reasons, the only thing we see as better than stable dividends are dividends with the propensity for growth. We’ve noted before that dividend growth is often a silent factor in investing and one of our favorite investment characteristics. We believe dividend integrity has many benefits, including a positive influence on a portfolio’s risk/return tradeoff, enhanced consistency and visibility, and a stable and often growing stream of income. All of these factors coalesce to reduce risk, smooth out the ride, and ultimately create a higher likelihood of earning positive returns.

This may sound simple, but the devil is in the details. And by “details,” we are referring to our comprehensive, in-depth security research process. This process includes developing an investment thesis; doing traditional balance sheet, income statement, and cash flow analyses; creating models; and gauging valuation, among other fundamental analyses that take place. For each security, the result is a report that highlights quality, valuation, and an investment thesis that drives our internally generated TSR (Total Shareholder Return) framework. The net result of our work results in a set of fundamental investment characteristics that are sound and compelling, both in absolute terms and compared to the broader market for stocks.

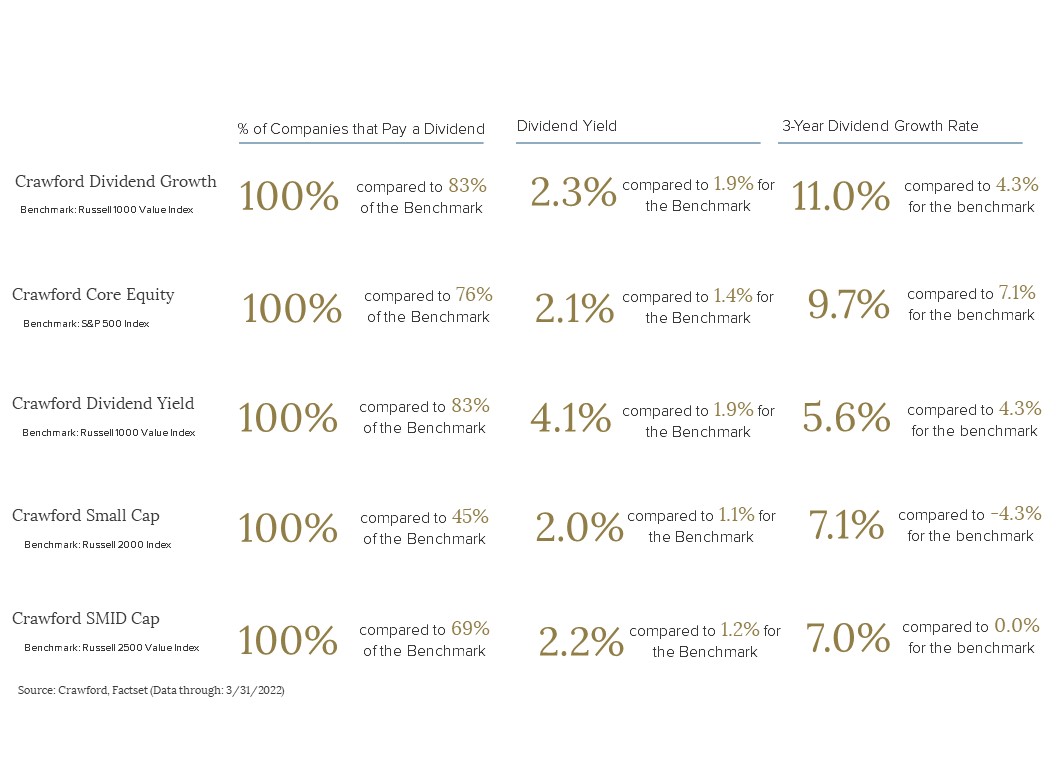

As indicated by the characteristics above, Crawford strategies have a high degree of dividend integrity. While it is true there are good stocks that do not pay dividends, we choose not to invest in these. Our approach embraces the reality of uncertainty. Because of this, through a number of incremental (and some not-so-incremental) measures, we narrow the range of outcomes, improve our chances for success, and align ourselves with strong companies that demonstrate dividend integrity. Income comes in regardless of what happens in the broader market. This is valuable for a number of reasons, not the least of which is that it reduces an investor’s need to sell assets in a period of market distress, like what we are experiencing today. We believe this is an outcome that should be avoided at all costs, and we have seen patient investors rewarded by staying the course and focusing on dividend integrity. To that we say, “Why not both?”

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-148

COVID Update

Since the initial vaccine was approved earlier this week in the U.S., we think an update on COVID is in order

Winning By Not Losing

Mitigating losses in a weak market environment, like the one we are experiencing today, is a key aspect of the way we invest at Crawford.

The Parable of Tom the Turkey

Our past experience makes us wary of investments that are too good to be true. We know investments that go up like an escalator typically come down like an elevator.