As a stock market investor, there are few guarantees. However, at Crawford Investment Counsel (Crawford), we believe that if one has a well thought out investment discipline and remains invested over the long term, suitable investment results will follow. Equities in the U.S. have historically compounded at very attractive rates, generating considerable wealth in the process. The continuation of this long-term trend is certain, given the history of market returns over substantial periods of time. We believe It’s safe to assume that returns will continue to accrue to shareholders in the future. What is not certain is the exact pattern of returns or the sequencing of results.

Known as ergodicity, an investor can achieve favorable rates of return over the long term, but also can experience periods where stocks earn well below their long-term averages. The uncertainty around how the market will perform over a multi-year period relates to the cyclicality of investment returns and tends to be heavily influenced by starting valuations (Price to Earnings (P/E) ratio, dividend yield, etc.). In summary, the stock market functions like a money machine over time, but it pays investors when it “wants to,” so to speak, not necessarily when they need to be paid. Herein lies a good portion of the inherent uncertainty with investing.

We’ve talked about patterns of returns and how we feel this is particularly important for investment portfolios that are subject to a spending policy or annual withdrawals to meet financial expenses or commitments. The bottom line is that we believe you have to earn at or above your spending or withdrawal rate over time. But this is not always enough, for the stock market can go through long periods of sub-average results, leading to the potential for permanent loss of capital in the process. We see that Positive compounding is powerful, but compounding in reverse can be equally as powerful and sometimes even more so. Spending decreases portfolio value, which exacerbates the effect of any decline in the market. This can be a slippery slope and can put investors at risk of impairment to portfolio values. And we haven’t even factored in the deleterious effects of inflation over time.

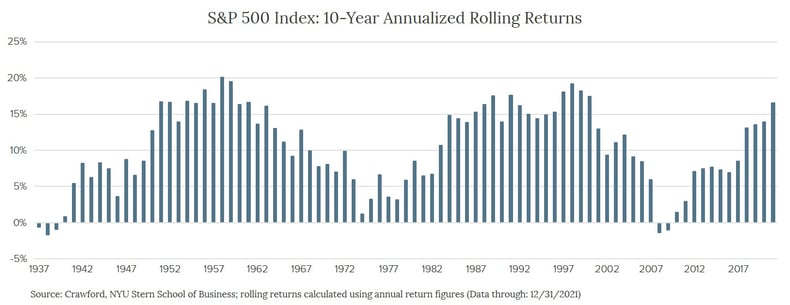

The chart below looks at rolling 10-year returns for the S&P 500 Index which is widely understood as a barometer for the market at large. Clearly, returns are cyclical, but the scarcity of periods where stocks earn negative returns over any 10-year period speaks to the fact that most long-term investors tend to enjoy the benefits of owning stocks. Note that we have just completed a period of above-average ten year results. Typically, strong decades of returns are followed by much more pedestrian results, or relatively poor decades. We also note that starting with low valuations, as measured by lower P/E ratios and higher dividend yields, has historically led to much better future returns than investing at high valuations. These phenomena are clearly related, justifying our case that valuations are a good predictor of future results. Although we began by stating that returns are uncertain, historical patterns indicate some signaling and information. Today, valuations are not cheap relative to history, further implying more modest returns in the coming years.

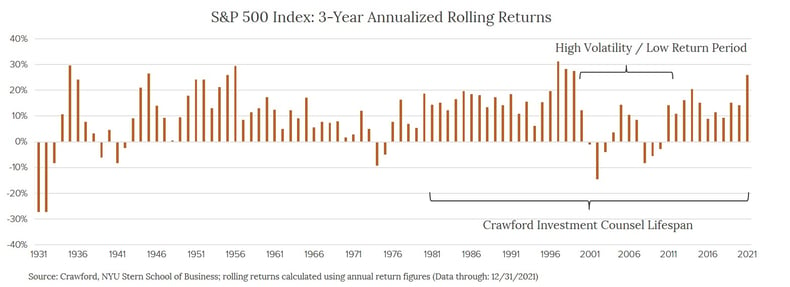

But what about a shorter period of time, such as three years. This seems to be more applicable for most since by the time one gets to ten years it may well be too late to “catch up.” The chart below examines 3-year rolling returns for the S&P 500 Index. These are more cyclical or variable than the 10-year numbers, since the time frame is far shorter. Somewhere between three and five years is more likely to be the time horizon many utilize to evaluate an investment program or determine whether the portfolio is meeting needs and accomplishing objectives.

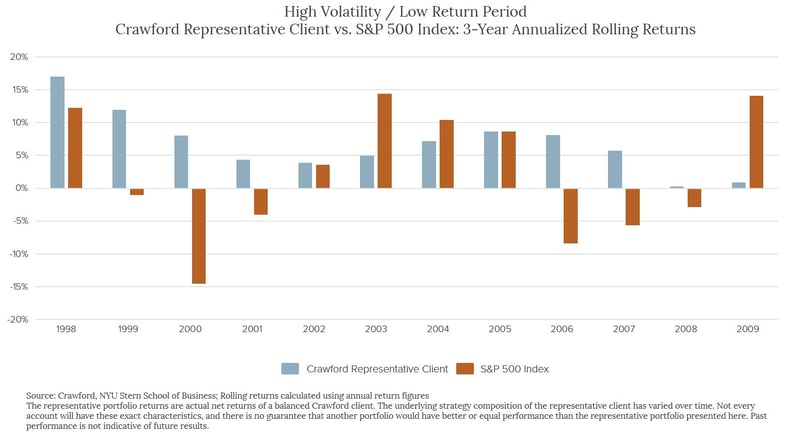

So, what to do with the degree of cyclicality or variability present in market returns over shorter periods of time? Most diversify between stocks and bonds or some other asset category in an effort to smooth returns and achieve objectives. This is prudent. But at Crawford, we believe we have a far superior way of dealing with uncertainty. It begins with dividends, and it focuses on quality, valuation, and the fundamental progress of the businesses owned in the portfolio. These are all safeguards that enable us to deliver alpha, or outperformance relative to the level of risk assumed. Conveniently, this value-add we provide occurs when our clients need it most. Take a look at the following chart; it is the same 3-year rolling return chart over a high volatility period compared to a Crawford representative client’s returns. By offering solid participation in strong up markets and excess return when markets are providing modest returns, we help overcome the sequencing problem and remove some of the uncertainty associated with return patterns. It’s a smoother ride, and there are many other benefits that come along with this.

One such benefit is related to our previous statement that the market pays you when it “wants to.” Crawford’s equity strategies pay you each and every year with a reliable and consistently rising stream of income from the dividend. Steady and increasing cash flow from the portfolio means investors have a higher likelihood of positive results. This is important when returns from the market are below 6% per year, a threshold many need to achieve or else they risk invading principal. Crawford’s clients have to “sell less” in any market to fund spending needs due to the rising cash flow provided by dividends and dividend increases. This is especially critical in down markets, as a good portion of the cash needed is already coming in naturally via the dividend.

Uncertainty about the future can lead to poor decision-making and, in some cases, abandonment of a strategy or investment program. This rarely happens to Crawford’s clients, and we believe that the pattern of returns is a big part of the reason why. We believe remaining invested is critical to long-term success, and a more consistent pattern of returns includes compounding returns at an attractive rate, ultimately resulting in higher terminal values. It’s a large part of the reason we have consistently applied the same philosophy for over 40 years.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-133

The Total Shareholder Return Trifecta

We invest to achieve an investment trifecta by selecting stocks that provide our investors with all three components of total investment return: fundamental business progress or growth, dividend yield, and valuation improvement

Bursting the Bubble: Speculative Fervor Then & Now

Long-term success comes from staying disciplined, avoiding speculative frenzies, and focusing on remaining invested in high-quality investments that can weather the test of time.

Terminal Value: A Lesson in Asymmetry

We believe that at the forefront of any investor’s mind should be both the threat of principal erosion or permanent loss of capital and the significance of the pattern of their investment returns.