Currently, there is a significant commercial push for international investing, mainly driven by larger investment companies using their airtime to proclaim that “Europe is Less Expensive than the U.S.” or that “Chinese Companies Offer Better Growth.” We have heard this before. While some of it may be accurate, it is part of a cyclical pattern that often leaves individuals investing in markets they do not understand and who find themselves without a seat when the music stops. Predicting geographic returns is highly uncertain and has been an inferior way to invest.

At Crawford Investment Counsel, we are focused on what we see as higher-quality companies that pay dividends which has two broad functions.

First, dividends contribute to investment return and help our clients generate current income without selling their holdings. Second, quality and dividends are inexorably linked and act as buffers in down markets that allow our clients to feel less pain and avoid selling at the wrong time.

In international investing, we take a similar approach, emphasizing that quality is of utmost importance. Our portfolios offer exposure to international markets, but mainly through American and established European companies. We prefer businesses with the majority of their revenue in established, regulated, capitalist markets. These three market characteristics – established, regulated, and capitalist – have proven to be what we see as the most important aspects of markets that foster longer-term appreciation for investors. We expect this trend to continue. However, within these markets are companies that have the opportunity to move geographically to accelerate growth and improve returns.

Let’s look at a specific example. Our initial thesis for investing in AstraZeneca was transformation, as a new CEO joined the company and rejuvenated the research and development effort. While our shareholders have benefited from the new product success, we have also prospered from management’s expansion in international markets. AstraZeneca invested heavily in its respiratory products in emerging markets, especially China. In these countries, air quality standards are lower, and there is a higher case of respiratory diseases, such as asthma. As a result, AstraZeneca developed an extensive sales and distribution network, including a highly technical artificial intelligence scheduling system that allowed patients and parents to find centers to treat their or their child’s asthma. This is one of the reasons that AstraZeneca has grown its emerging market revenue significantly above the industry for the last five years.

This is an instance where we outsourced the investing decision regarding geography to AstraZeneca, which established a multi-billion dollar market. Our initial due diligence was on AstraZeneca’s new management’s ability to expand its pipeline, but as the China opportunity came forward, it was easy to see how this global pharmaceutical company could port technology from Europe to China and build a large franchise. So we made an investment in a high-quality, diversified global pharmaceutical company with a history of consistent dividend growth, which would have fulfilled the objectives of our strategies on its own. It just so happened that AstraZeneca also brought significant emerging market growth and, through a deliberate strategic effort, now has almost a third of its revenue in higher-growth markets.

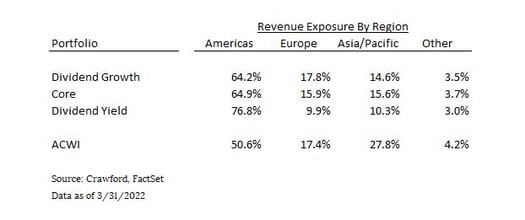

We start at the individual company level for our investment selections and monitor interactions at the portfolio level. The chart below shows the revenue by geographic region for all of the companies held in our three large-capitalization strategies – Dividend Growth, Dividend Yield, and Core. The ACWI and the MSCI All Country World Index are the most commonly used vehicles to track global market components and returns.

As you can see, the Crawford portfolios are purposefully overweight in the Americas as the United States markets hold the most companies that fulfill our quality and dividend criteria, along with the sustainability of returns that are fostered in regulated capitalist markets. Our portfolios are also underweight Asia/Pacific, because those markets do not possess the characteristics that we believe foster sustainable, long-term investing. More broadly, we have lower exposure to higher-production markets (i.e., China, Vietnam, etc.) and higher exposure to more mature consumption markets (the United States).

In this piece, we highlighted AstraZeneca, but the same trend permeates through many of our other investments, such as Coca-Cola, UPS, and IBM. In our view, the safest way to gain greater, sustainable, profitable growth in international markets is to find companies we understand in the local markets and let management expand already strong franchises globally to capture more significant growth. We believe this has proven to be a sound strategy to optimize returns and reduce uncertainty or risk in the process.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-134

The U.S. Remains a City on a Hill

U.S. exceptionalism, whether thought of in its broader original context, or the more restrictive financial and economic context, is essential to the future well being of our country.

You Are Here: Intersection of Quality and Value

Crawford seeks to be at the intersection of value and quality. Here is how we get there.

Stocks: Rent, Own, or Just Stay in a Hotel?

If owning a stock with a six-month time horizon is analogous to renting, then options contracts can be compared to staying in a hotel.