Most consumers will tell you that online shopping is on the rise. Today, many order consumable items like detergent, razor blades, and paper towels online, and a growing percentage do so with automatic replenishment. Ask the average U.S. consumer how many retail visits they make each week now versus a year or two ago, and the answer would be “not nearly as many.” But this is not simply due to the lingering effects of the Covid pandemic. The truth is, the online “retail experience” is superior in many ways including price, availability, convenience, etc. It is little wonder that e-commerce continues to take share of the average consumer’s wallet.

At Crawford Investment Counsel (Crawford), we seek high-quality, unusually consistent companies with sustainable competitive advantages. We invest in companies with forward-thinking management teams who allocate capital in a fashion that we see both rewards shareholders and allows the underlying businesses to thrive and prosper. With the secular trend of e-commerce continuing to grow at the expense of traditional brick and mortar retail, we find what we believe is a long-term investable theme. We believe this theme dovetails well with our emphasis on high-quality companies that offer consistent growth.

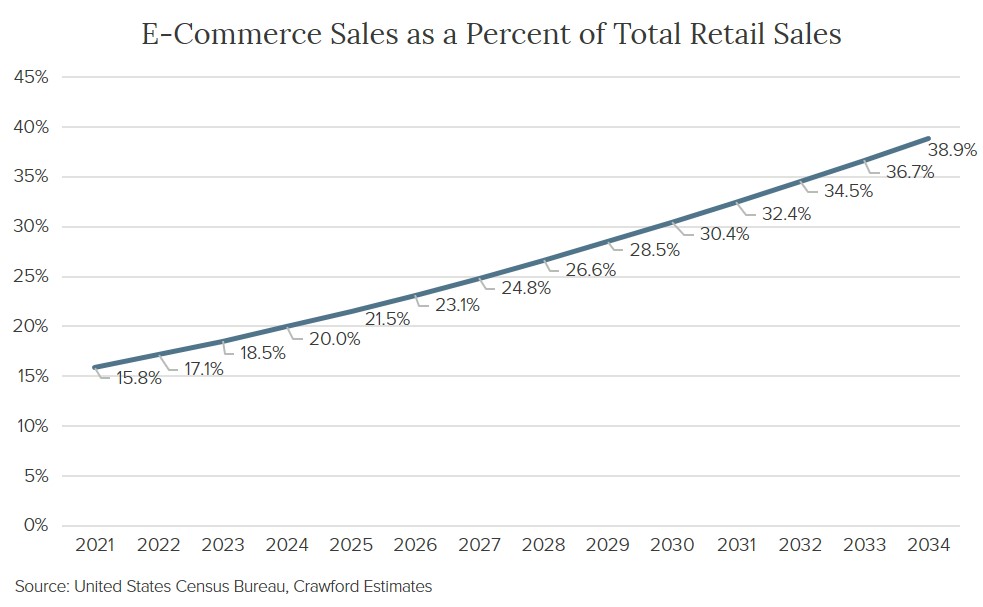

Assuming normalized growth rates for retail sales at low teens, e-commerce sales will account for roughly one-third of total retail sales in 2031.

At Crawford, we invest in businesses that we feel have management teams that embrace the future and invest in e-commerce and omni channel endeavors. This is not to say that businesses cannot be successful with brick and mortar retail. In fact, we prefer businesses that manage brick and mortar retail with keen financial acumen and demand that each individual store delivers Free Cash Flow and positive ROIC (Return On Invested Capital). These businesses also reward long-term shareholders with a growing dividend. On the other hand, we seek to avoid companies we believe are facing secular headwinds. Consequently, across the entire complex of our investment strategies, very few of Crawford’s retail holdings have even a small fleet of mall-based stores.

Specifically, we have gravitated to a small cadre of thoughtful, forward-looking retailers who allocate capital in what we believe to be the direction of retail’s future. In some cases, that means utilizing automated robotics in warehouses for e-commerce or in-store fulfillment. In other cases, it means solving the same-day delivery equation. Omni channel capabilities provide shoppers with the ability to connect in-person, virtually, or in some combination of the two. This is proving to be an important competitive advantage. Generally, we have avoided mall-based retailers, as we believe the statistics paint a bleak picture of secular decline.

Retailing has always been a tough business with slim margins and high fixed costs. Immediate price discovery via smartphones has only contributed to the difficulties these businesses have faced. Crawford strategies favor “traffic-advantaged” retailers in strip centers or free-standing locations rather than malls. We believe balance sheet strength is one of the pillars of quality, and owning land and a four-wall store bolsters the balance sheets of these business. These merchants own a valuable land asset, and ownership of these land assets means they are not encumbered by long-term, onerous leases. The retailers we favor have what we see as enlightened management teams who have looked to the future of retail, investing in ship-to-store, ship-from-store, BOPUS (Buy Online Pick Up in Store), and curbside pickup, as well as automation in distribution centers and fulfillment centers. The ability to provide same-day or two-day shipping, in some cases to over 90% of the U.S. population, means they are able to compete with pure online options and provide prosperous returns to shareholders. We are confident that our retail holdings will not be victims of the coming continually evolving retail apocalypse, but instead will be beneficiaries.

In conclusion, our portfolios at CIC are thoughtfully curated with publicly traded retailers in the way of good traffic, sustainable competitive advantages, astute management teams, and growing dividends. These advantages are accompanied by strong balance sheets and unburdened by lease obligations. We expect our retail holdings within Crawford’s strategies to perform well, not in spite of the demise of the mall, but in part because of it.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-123

The Parable of Tom the Turkey

Our past experience makes us wary of investments that are too good to be true. We know investments that go up like an escalator typically come down like an elevator.

Real Estate Investing with a Private Equity Mindset

At Crawford, we will continue to invest in publicly traded real estate with a private equity mindset, while offering something many others cannot provide everyone today: liquidity.

REITs for the Long Run

REITs are not traditional common stocks, but many of the companies in this area fit very well with our investment priorities and methodology.