“Investors are confronting one of the most uncertain periods of their lifetimes. Stocks are rallying anyway.”

-The Wall Street Journal; Why Stocks Are Rallying in the Midst of a War and Soaring Inflation; April 10, 2022

“I’ve lost confidence in our ability to predict where history is headed and in the idea that as nations “modernize” they develop along some predictable line. I guess it’s time to open our minds up to the possibility that the future may be very different from anything we expected.”

-The New York Times by David Brooks; Globalization Is Over. The Global Culture Wars Have Begun; April 8, 2022

At Crawford Investment Counsel (Crawford), we have been talking more and more about uncertainty as current events have unfolded. The Fed is in play, Putin is in Ukraine, and inflation is running hotter than just about anyone expected. We do not know just how these events will play out, and their impact to the investment environment is still uncertain.

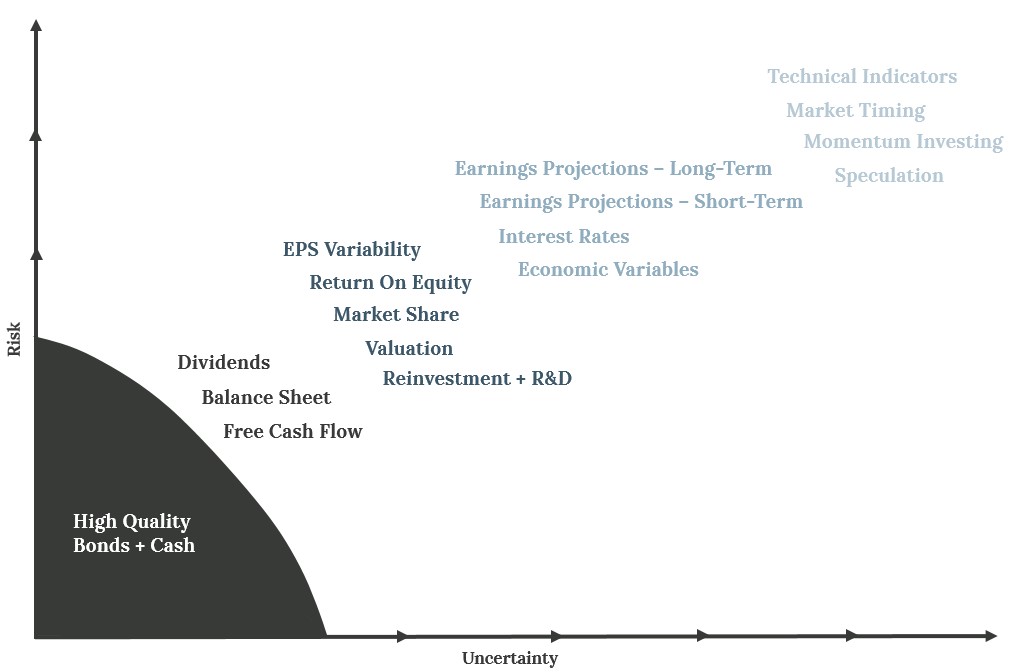

Traditionally, bonds and cash have helped dampen volatility and reduce risk, but this relationship has broken down in the current climate of higher inflation and rising interest rates. This is only partly why we believe an inflationary scenario is problematic. Despite this, we continue to believe that bonds and cash can be stabilizing influences on a portfolio. We believe they are still valuable portfolio tools to be utilized where appropriate. The current environment of uncertainty begs the question of how to invest in stocks in an increasingly risky world. Visually, our answer lies in the representation below, which establishes a somewhat linear relationship between uncertainty and risk.

Source: Crawford

As indicated above, as uncertainty increases, so does risk. Our response at Crawford is to focus first on quality. We believe this is a way to mitigate volatility, or reduce the potential for loss, and dividends serve as our initial window into quality. Because dividend-paying companies tend to be what we see as higher-quality companies with more predictable and consistent underlying business models, this orientation reduces uncertainty. Said another way, quality and dividends help narrow the range of investment outcomes. We believe traditional factors such as dividends, balance sheets, and free cash flow are primary indicators of quality, markers of business consistency, and characteristics that give value to stocks. We perform traditional balance sheet, income statement, and cash flow analyses. Beyond this, we search for quality by focusing on reinvestment rates and metrics such as EPS Variability, Return on Equity, and Valuation.

More forward-looking projections of earnings or economic variables represent higher risk and uncertainty, and techniques such as market timing or speculative investing represent the highest risk and most uncertain outcomes. The former is pursued with diligence and rigor with an understanding that future projections are just that. The latter is not employed at Crawford.

Historically, our portfolios have provided a smoother pattern of returns and excellent downside protection. We believe these can be critical factors leading to investment success, particularly in a world of uncertainty. Risk control is an important byproduct of our investment process. Crawford strategies routinely rank in the bottom decile of volatility against peers and have a very low relative beta factor. These statistical measures of risk control are structural and due to our strategies’ inherent quality biases. The result is what we believe are attractive upside and downside market capture rates over time. This trade-off has led to participation in the upside with protection and preservation of capital on the downside, ultimately producing substantially positive alpha over time.

Positive alpha generation is the holy grail of investing. The efficient market theory suggests that it cannot be done consistently. However, we have had meaningfully positive alpha statistics across the board since the inception of each of our six equity strategies. In summary, the alpha figures above are the excess annual returns generated by our strategies over and above what the risk level suggests should have been earned. We are very proud of these results and look forward to building on them in the future.

The information above gives us confidence that our strategies will be well-positioned in an increasingly uncertain environment. Higher volatility, or more risky strategies, are theoretically supposed to provide higher returns. But our experience is that on a risk-adjusted basis, each of our Crawford strategies performs higher than one would expect, given their lower risk profiles. This is part of the value Crawford provides. It illustrates that we have an investment ideology and framework for implementation that proves successful in periods of uncertainty.

Please reference our related Podcast for more detail:

Disclosures:

1 Annualized Alpha Since Inception time periods

Core Equity vs. S&P 500 Index: 1/1/2000 – 12/31/2021; Dividend Growth vs. Russell 1000 Value Index: 1/1/1981 – 12/31/2021; Dividend Yield vs. Russell 1000 Value index: 10/1/2010 – 12/31/2021; Small Cap vs. Russell 2000 Index: 1/1/2012 – 12/31/2021; SMID Cap vs. Russell 2500 Value Index: 1/1/2013 – 12/31/2021; Managed Income vs. NASDAQ US Multi-Asset Diversified Income: 4/1/2014 – 12/31/2021

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-109

Generating Income and Exploiting Inefficiencies

Our Managed Income Strategy generates attractive, income-oriented returns with lower risk by exploiting these opportunities in higher-yielding securities.

Interview with the Core Equity Portfolio Manager

At Crawford, all of our strategies help investors achieve a specific set of goals and solve for certain needs. Clients are attracted to the Core Equity strategy because it has a higher focus on growth than other Crawford strategies.

Winning with Quality in the Consumer Discretionary Sector

At CIC, we seek high-quality companies for long-term investment.