At Crawford, we seek to invest in higher-quality, consistent companies that produce more predictable earnings and dividends. Investing is about the future, which is uncertain, so we seek to improve our chances of success by focusing on companies that display fairly constant demand for their products and services. This tends to eliminate many highly cyclical or overly economically sensitive companies whose businesses may be more volatile in nature.

We have found that a number of companies within the Industrials sector offer us moderate economic sensitivity and exposure to attractive end markets with barriers to entry and sound profitability. These companies typically are utilizing technology to foster automation or improve outcomes and enjoy both niche businesses and high market shares. All of this leads to high visibility, attractive cash flow generation, and above-average quality. As you might expect, the fundamental characteristics of this sector align well with our orientation toward the dividend as an initial indicator of quality.

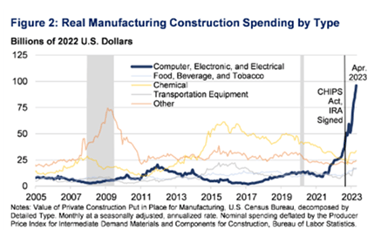

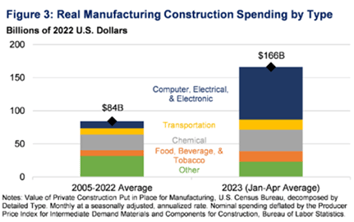

Related to this sector, one of the strikingly positive aspects of our economy today is the capital spending boom. There has been an increase in construction spend for manufacturing facilities, and this surge appears to be unique to the U.S. In fact, real manufacturing construction spending has doubled since the end of 2021. Manufacturing construction is just one element of a broader increase in U.S. non-residential construction spending. In other words, investments in new factories and on-shoring of manufacturing capacity has not crowded out other types of construction spending.

The recent boom is driven by demand for computer, electronic, and electrical manufacturing, and spending on this kind of construction has nearly quadrupled since the beginning of 2022. This is a newly dominant component of manufacturing in the U.S., and the progress comes in part from a supportive policy environment. The Infrastructure Investment and Jobs Act, Inflation Reduction Act, and CHIPS Act have all provided direct funding and tax incentives for public and private manufacturing construction. Meanwhile, overall spending in other manufacturing segments remains at long-term levels, meaning the new activity is not cannibalizing other investment.

Admittedly, some of the increase in spend is necessary due to rising costs in recent years. But the charts below illustrate that recent spending (relative to historical averages) is not solely due to inflationary pressures.

Much of this recent boom has been semiconductor investments related to the expansion of existing or entirely new chip fabrication plants (fabs). These fabs are located in established and growing semiconductor hubs across ten states. With American “fabless” design firms relying on semiconductor foundries in Taiwan for the majority of their chips, re-shoring of chip fabrication is a significant step toward more secure supply chains amid increasing tensions with China. In addition to fabs, there have been two announced investments in semiconductor equipment facilities. Equipment facilities near fabs allow for increased collaboration between chipmakers and equipment suppliers, giving chipmakers greater access to leading-edge technology and accelerating innovation.

In total, over 70 new semiconductor ecosystem projects have been announced in the U.S., all spurred by the CHIPS Act. This, along with over $250 billion in private investments in 22 states, creates 45,000 new high-quality jobs in the semiconductor ecosystem. This will support hundreds of thousands of additional jobs throughout the broader U.S. economy, as well. While the striking trends present today may cool, the CHIPS Act has fostered an ongoing opportunity for investment in this sector. We are encouraged by this progress and believe it bodes well for Crawford’s investments within the Industrials sector.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2 and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-2403-2

Origins: Crawford Dividend Growth Strategy

The old saying, “necessity is the motherhood of invention” is a good way of introducing the story of the origin of the Dividend Growth strategy.

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

Growth of Income: Two Paths, One Philosophy

Our Dividend Growth and Dividend Yield strategies offer two distinct paths to harness the power of dividends, allowing investors to align their portfolios with their specific income and return objectives.