In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- We believe high grade bond yields are likely to remain range-bound over the near term. Significant yield changes would necessitate meaningfully higher inflation data or substantial labor market deterioration.

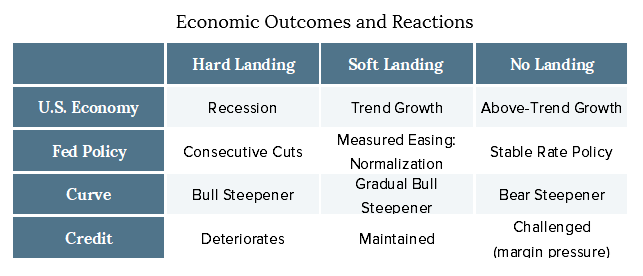

- Going forward, we believe the two most likely economic outcomes are a hard or soft landing. Our strategies are positioned to outperform in both scenarios based on sector weights (bias to agency/municipal/defensive corporates) and yield curve positioning (longer duration).

- Our Core and Municipal strategies are positioned to:

- Preserve capital with a strong bias to high quality (sector and issuer credit strength).

- Benefit from total return as rates adjust to a more balanced economic environment (yield curve positioning and maturity extension).

- Produce a high level of current portfolio income (bias to higher-yielding spread sectors and above-average coupons).

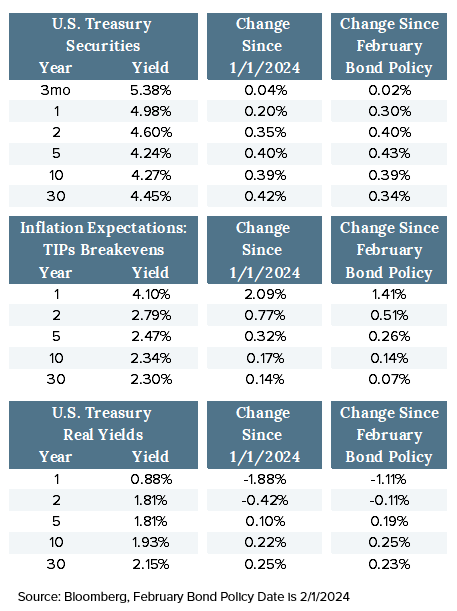

Treasury Yields as of 3/30/2024 (Post-Fed Meeting)

- Nominal interest rates moved higher and relatively evenly across the yield curve between the January and March Fed meetings, driven by higher inflation expectations in the 1- to 5-year range and higher real yields in the 5- to 30-year range.

- This behavior reflects rising inflation expectations based on recent CPI and PCE data and an increased likelihood that the Fed may not ease rate policy to the degree many expected.

- The 3-month/10-year Treasury inverted yield curve flattened by roughly 36 basis points (bps) between Fed meetings.

- The 2-year/10-year Treasury curve was effectively unchanged.

- The “bear steepening” of the 3-month/10-year Treasury curve reflects that short-term rates have remained tied to unchanged Fed policy, while higher inflation and real rate expectations are discounted in longer-term yields.

- This suggests an increased level of market conviction for a “higher-for-longer” rate cycle.

- Bond yields are likely to remain range-bound over the near term.

- An inflation breakout would be needed to push yields meaningfully higher.

- Significant labor market deterioration would be needed to pull yields meaningfully lower.

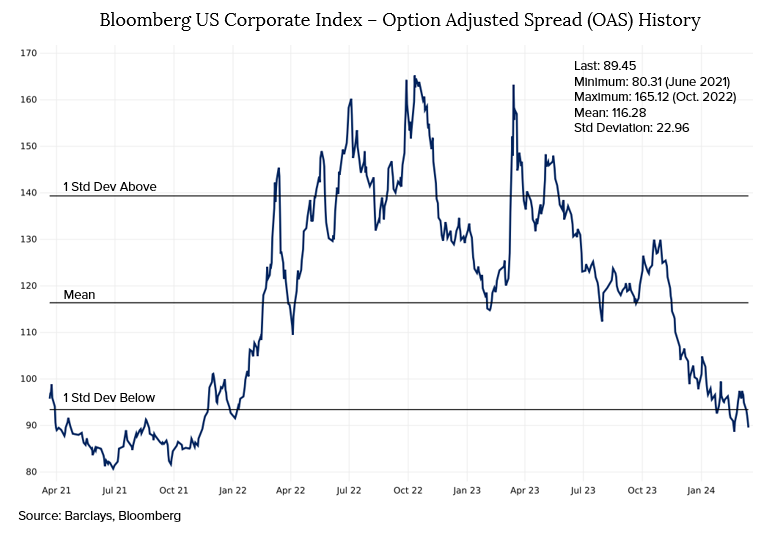

Corporate Bond Market

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- The US Corporate Index OAS tightened by roughly 9.5 bps between the January and March Fed meetings, reflecting continued fundamental strength and investor demand despite record issuance.

- Technical Support: Attractive nominal yields continue to support strong investor demand:

- YTD New Issues are 3.7x oversubscribed vs. 3.5x in 2023

- Despite record YTD issuance of roughly $500B (+43% year-over-year)

- As the Fed begins lowering the Fed Funds target rate, a portion of money market fund balances (roughly $6T) will seek higher yielding alternatives (demand estimated at roughly $400 - $600B)

- Fundamental Support: Corporate balance sheets have been leaning conservative to prepare for recession:

- Cash balances are higher

- Share buybacks and capital expenditure growth are down

- A supportive macro environment with economic growth and loosening financial conditions

- Through the end of 2023, EBITDA margins continued to increase, and Net Leverage metrics were steady

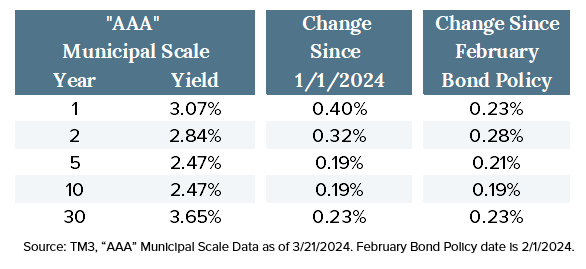

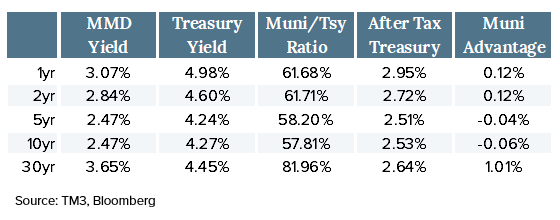

Municipal Bond Market

- Municipal Bond “AAA” scale yields have moved higher across the curve since the January Fed Meeting.

- New issue supply has been higher than expected year-to-date, but demand has more than offset any potential technical pressure. Retail investor mutual fund flows have been positive for 19 straight weeks.

- The increase in municipal yields has primarily been driven by correction in sympathy with Treasury security performance.

- Municipal bonds have outperformed Treasury securities on a relative basis, however, leading to lower Muni/Treasury ratios and relative value richness.

- Revenue bonds have outperformed General Obligations, and within the Revenue sector, Healthcare and Transportation bonds have been the best relative performers.

- This confirms a demand bias toward lower quality as investors stretch for yield.

- Looking forward, municipal headwinds include:

- Rich relative valuations

- A heavier supply calendar

- Treasury market volatility as the Fed transitions policy

- Municipal tailwinds include:

- Absolute yield levels

- Credit strength

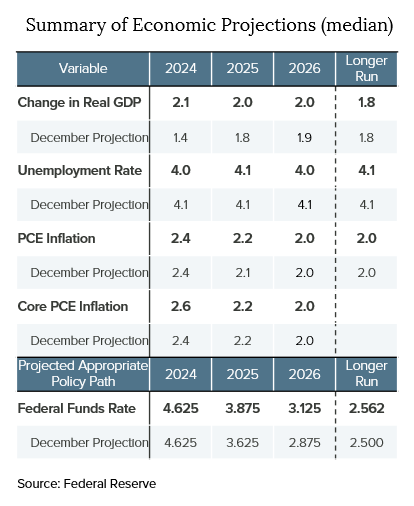

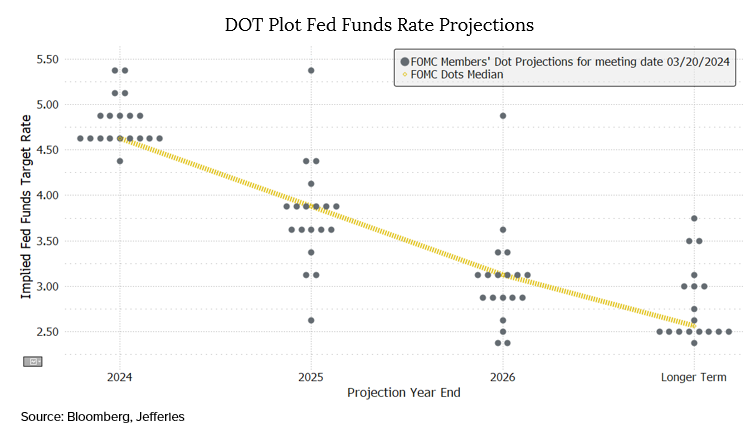

Summary of Economic Projections & DOT Plot

- Revisions to the economic and policy path projections include:

- Increases to projected Real GDP in 2024, 2025, and 2026.

- Modest decreases to the projected unemployment rate in 2024 and 2026.

- A modest increase in projected PCE Inflation in 2025 and in Core PCE inflation in 2024.

- 25 basis point increases to the projected Fed Funds Target Rate in 2025 and 2026, and a 6 basis point increase in the long-run projection.

- In summary, the SEP and DOT Plot illustrate the Fed acknowledging the strength of the economy and likelihood of “higher for longer” rate policy.

- There are now seven dots of 3% or higher in the "Longer Term" category, compared with four dots in December, signaling a growing belief in a neutral rate greater than 2.5%.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-2403-3

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.