Successful Outcomes:

It’s Not Just What You Earn, But How You Earn It

At Crawford Investment Counsel (“Crawford”), our overall investment philosophy starts with our belief of quality in the interest of narrowing the range of potential outcomes for our clients. Through narrowing the range of outcomes, we believe we can improve our chances of success, tend to mitigate the likelihood of adverse returns, and enhance our investors’ return patterns. In short, a sequence of returns can be critical to portfolio success, while the experience of large drawdowns can be detrimental to the terminal value of that very portfolio. At Crawford, we believe that, at the forefront of any investor’s mind should be both the significance of the pattern of their investment returns and the threat of principal erosion or permanent loss of capital. To the extent withdrawals are taking place, lower but more stable returns can actually result in higher terminal portfolio values. At Crawford, we have witnessed the asymmetrical quality that numbers have to them, and we seek to protect against this.

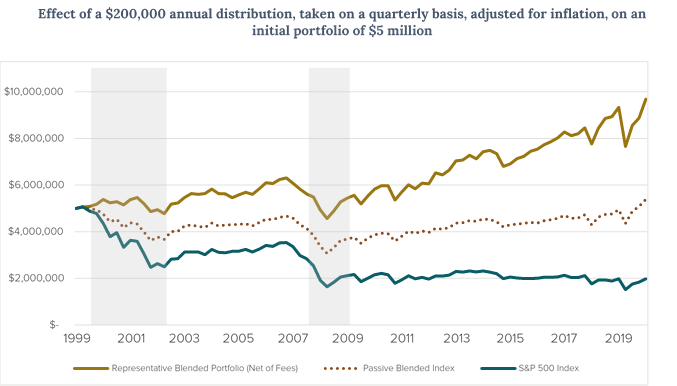

To put it simply, we believe that the pattern of returns earned can be more important than absolute returns. As previously stated, the figure below represents that a more consistent pattern of returns can actually lead to higher terminal values in a portfolio, especially when clients have spending needs to be met. The chart represents the 20-year performance of various investments with an initial value of $5 million coupled with an annual withdrawal of $200,000 (4% initial spending rate) adjusted for inflation each year. Throughout this 20-year period, the S&P 500 Index generated a total return of 6.6%. While this return is higher than the required initial withdrawal rate of 4%, a client invested in the S&P 500 Index would have experienced principal erosion. In other words, even though S&P 500 Index generated an annualized return above the required distribution rates, our analysis shows the investor would have ended up with absolute market value that is lower after 20 years. This is a direct product of the pattern of returns.

Source: Crawford, eVestment, Federal Reserve Bank of St. Louis; Time Period: 12/31/1999 – 12/31/2020

Source: Crawford, eVestment, Federal Reserve Bank of St. Louis; Time Period: 12/31/1999 – 12/31/2020

Investors are forced to make trade-offs. In many cases, we feel high returns are not worth the risks. We believe excessive volatility in pursuit of long-term return generation is not an acceptable option for many investors, particularly those who need to meet spending needs. Taking the unacceptable outcome of invading principal over a multi-year period into consideration, and respecting the strain that withdrawals can put on a portfolio in a low-return environment, we believe that the more consistent, stable returns that Crawford offers its clients over the long-term are a trade-off worth making.

How do we earn these consistent and stable returns? At Crawford, we have found that quality is a factor that favorably influences both risk and return. We believe the dividend and predictability are silent factors that help enable our investors to obtain income and growth of income, benefit from the fundamental progress of the businesses they’re invested in, and experience valuation improvements, all of which work together to contribute to total investment return over the long-term. With our focus on quality and value, we feel Crawford is able to both sustain strong participation in rising markets and offer superior protection during down markets. Through our strategies, we believe our clients are subjected to less volatility, providing a higher likelihood of earning a positive return each year, and mitigating the risk of abandonment, something that we believe is an underestimated risk associated with investing.

The potential to change investment strategy at the wrong time is a significant risk factor that threatens the ability to compound results at an attractive rate and can shift a temporary loss of capital to permanent status. Because of the consistency we seek to provide our clients with, we believe our investors have a higher likelihood of staying with their investment programs. Ours is a common-sense approach, rooted in what we believe is quality, and starting with the dividend. Through this approach, our clients can sleep well at night and maintain the confidence to invest and stay invested for the long-term. The emphasis on quality at Crawford, coupled with a value-based approach to total investment return leads to successful outcomes for our clients.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

Past performance is not indicative of future results. Crawford has the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. Not every account will have these exact characteristics, and there is no guarantee that another portfolio would have better or equal performance than the representative portfolio presented here.

The Passive Blended Index consists of 60% S&P 500 Index and 40% Bloomberg Barclays Government/Credit Bond Index. The S&P 500 Index is the Standard & Poor's Composite Index and is widely regarded as a single gauge of large-cap U.S. equities. It is market-cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization. The Bloomberg Barclays Intermediate Government/Credit Bond Index is an unmanaged index that tracks the performance of intermediate term US government and corporate bonds. The Bloomberg Barclays US Government/Credit Bond Index is a broad-based flagship benchmark that measures the non-securitized component of the US Aggregate Index. It includes investment grade, US dollar-denominated, fixed-rate Treasuries, government-related and corporate securities. The volatility (beta) of the portfolios may be greater or less than the benchmarks. It is not possible to invest directly in these indices.

CRA-21-165.1

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

The Rising Importance of Dividend Yield

We are likely moving from a period of above-average investment returns from stocks and bonds to a more normalized or lower return environment.

Quality: The Differentiated Investment Factor

We believe quality is a differentiated investment factor with various benefits including attractive long-term returns, protection in market declines, smoother patterns of return, and income production.