As investors in high quality small cap companies, we have faced a uniquely challenging environment since the beginning of the COVID-19 pandemic. While much of the recent industry commentary has focused on the interplay between Growth and Value investment styles, our analysis indicates that investor preference for low quality stocks has been the dominant driver of small cap stock returns over the past 18+ months.

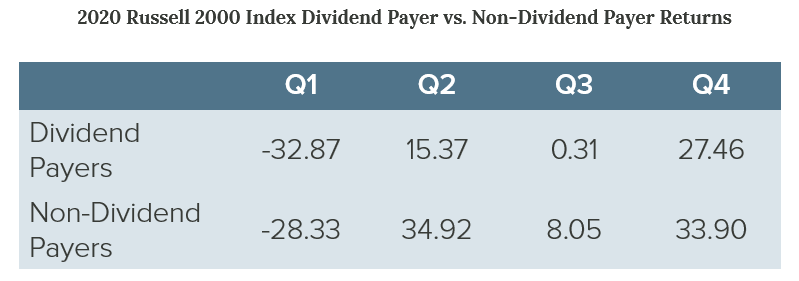

One indicator that the Quality factor has been out of favor with investors is the dramatic underperformance of dividend paying stocks throughout 2020. While we have observed previous episodes of underperformance by small cap dividend payers, the 41 percentage point difference in returns experienced last year is the largest in recent memory, even eclipsing the 36 percentage point gap seen at the height of the Tech Bubble in 1999.

Source: FactSet

We are certainly cognizant of the futility of attributing short-term stock performance to any one factor; however, we believe that investors were not specifically avoiding dividend paying stocks last year. Rather, for reasons we put forward later in this article, we feel the underperformance of dividend payers was symptomatic of investors’ preference for low quality business models that typically do not generate streams of reliable dividend payments.

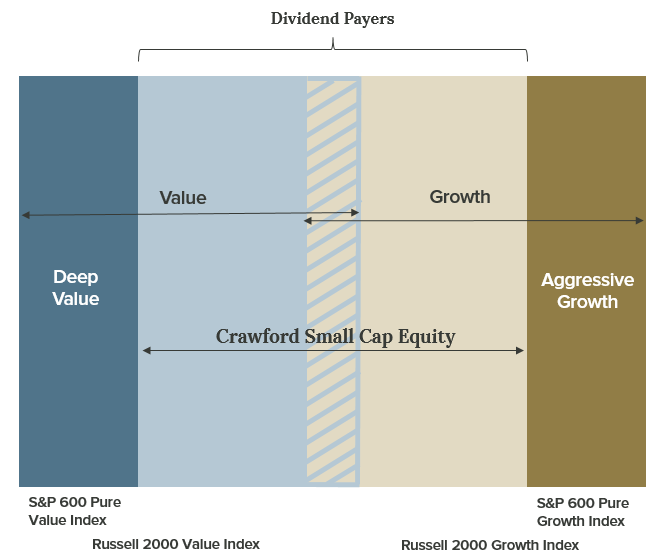

Before we take a deeper look at the market performance over the past few quarters, it would be helpful to visualize all small cap stocks falling somewhere within the range from Deep Value to Aggressive Growth (perhaps, better described as Speculative Growth), as depicted in the following exhibit. Traditionally, stocks in the value category have been associated with relatively low valuation multiples and slower earnings growth while, conversely, growth stocks often feature relatively high valuations and high investor expectations.

While it is often difficult to precisely classify stocks as either Value or Growth, we submit that quality attributes diminish the further one moves toward either end of the scale. On the Deep Value side, we often find mature companies with disrupted business models, levered balance sheets and highly cyclical revenues. On the other hand, the Aggressive Growth segment of the market is populated by companies in the early stages of their lifecycle that have low/no profitability and weak free cash flow generation. Neither category is appealing to us as quality investors seeking to minimize return volatility for our clients. In fact, our focus on stocks with sustainable dividend payouts appropriately precludes us from participating at these extreme ends of the Value-Growth spectrum.

In order to zero in on the performance of Deep Value and Aggressive Growth small cap stocks, we are using the S&P 600 Pure Value and the S&P 600 Pure Growth indices. While not perfect, we believe these benchmarks provide reasonably accurate representation of their respective market segments.

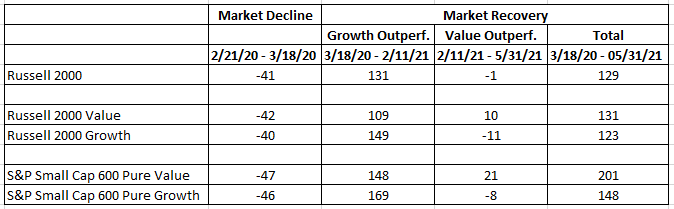

Performance data for the relevant small cap benchmarks is shown in the table below. We have chosen to disaggregate the small cap market recovery into two distinct periods based on which investment style was outperforming.

Source: FactSet

Source: FactSet

Many market observers have noted that during the initial phase of the market recovery from the pandemic-induced lows, Growth stocks significantly outperformed Value stocks. From our analysis, this was attributed to the perceived resilience and continued adoption of new technologies like digital communications and alternative energy generation, even in the face of the near-total economic shut down. Given that most of these technologies were still in the early innings prior to the pandemic, companies seeking to commercialize them largely exhibited Aggressive (Speculative) Growth attributes discussed above. Additionally, large government outlays on COVID-19 vaccine and treatment research almost indiscriminately benefited a wide swath of biopharma companies, which typically represent some of the riskiest choices within the Aggressive Growth niche of the small cap market. As a result, while Growth stocks certainly performed well overall, Low Quality Growth stocks were the ones driving outsized returns last year as evidenced by the 169% gain in the S&P 600 Pure Growth Index from 3/18/20 to 2/11/21.

Spurred by the unprecedented amounts of fiscal and monetary support as well as rapid vaccine progress, the stock rally began to broaden out around the middle of last year. However, it was mostly the Deep Value segment of the small cap market that started to outperform in tandem with Growth stocks. In particular, shares of brick-and-mortar retailers surged as these struggling businesses were seen benefiting from a rebound in consumer spending fueled by government stimulus. Once again, the strongest returns were concentrated in low quality stocks, this time at the Value end of the spectrum, with the S&P 600 Pure Value index gaining 148%, nearly matching the 149% increase in the Russell 2000 Growth index for the 3/18/20 – 2/11/21 period.

Starting in mid-February of this year, we have seen a shift in market leadership from Growth to Value, coincident with the increase in interest rates and general economic optimism. We feel this was beneficial to Crawford Small Cap performance given our overweight of relatively high quality value stocks such as Financials and Industrials. That said, low quality value stocks in the highly cyclical sectors like Energy and Materials also produced substantial gains, limiting the portfolio’s outperformance. Furthermore, the emergence of the “meme stock” phenomenon posed another challenge for our investment style as investor attention has been disproportionately fixated on Deep Value stocks with endangered business models (e.g. GME, AMC, BBBY). The irrational gains in these stocks (thousands of percentage points in the span of several months) have provided meaningful contribution to index performance and propelled the S&P 600 Pure Value index to a 201% gain from the market bottom through 5/31/21. Needless to say, the vast majority of these stocks represent highly speculative investments and lie beyond the boundary of acceptable quality for our investment process.

In summary, since the early days of the COVID-19 pandemic, the small cap market has been defined by the outperformance of low quality stocks at both ends of the Value-Growth continuum. At the same time, higher quality stocks in the middle of the style range have seen little investor interest. We believe that this return disparity has been driven by record amounts of financial liquidity, ultra-low interest rates, unprecedented government intervention and the effects of a rapid economic recovery. As powerful as these factors are, we view them as unsustainable in the long run. Ultimately, we expect that a more typical historical pattern of outperformance by high quality small cap companies will reassert itself, and our patient, fundamentals-based investment approach will once again be rewarded.

Disclosures:

Crawford Investment Counsel is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Crawford's advisory services can be found in its Form ADV Part 2 which is available, without charge, upon request. Additional information can be found at www.crawfordinvestment.com.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

The opinions expressed are those of Crawford Investment Counsel. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. Past performance does not guarantee future results.

CRA-21-118

High and Rising Income: Crawford Dividend Yield Strategy

In this strategy, growth of income is achieved by owning companies that increase dividends regularly, and it is buttressed by our active management process.

An Extreme Environment... Revisited

As we approach the fourth anniversary of the COVID-19 pandemic, we wanted to revisit an article we published in mid-2021

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.