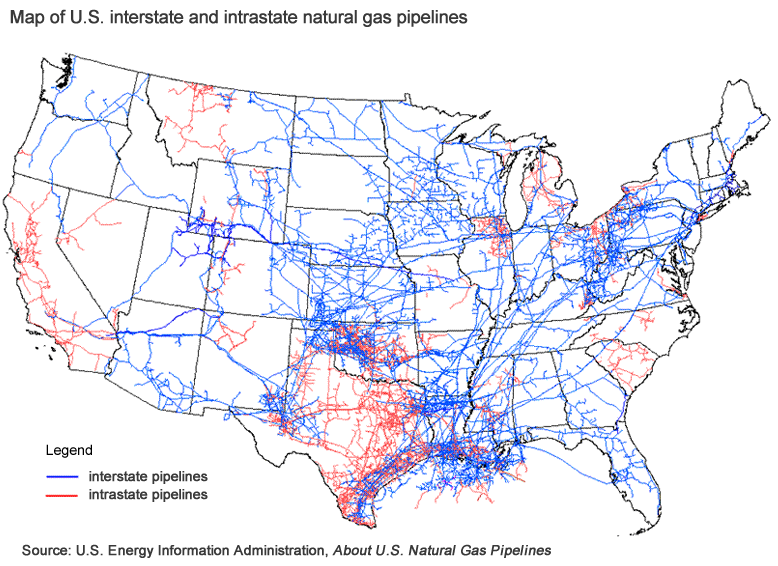

Have you ever thought about how the natural gas we use for cooking or to heat our homes gets there? This seemingly ubiquitous commodity is vital to our daily lives, and quite a lot goes into producing and delivering natural gas into your home. The backbone to the U.S.’s nascent energy independence is due in large part to the energy infrastructure built over the last 70 years. Over 44% of the natural gas produced in the U.S. comes from two states: Texas and Pennsylvania. Louisiana, Oklahoma, and Ohio produce another 26% collectively, and all five states account for 70% of the natural gas produced in the U.S.

What is Energy Infrastructure?

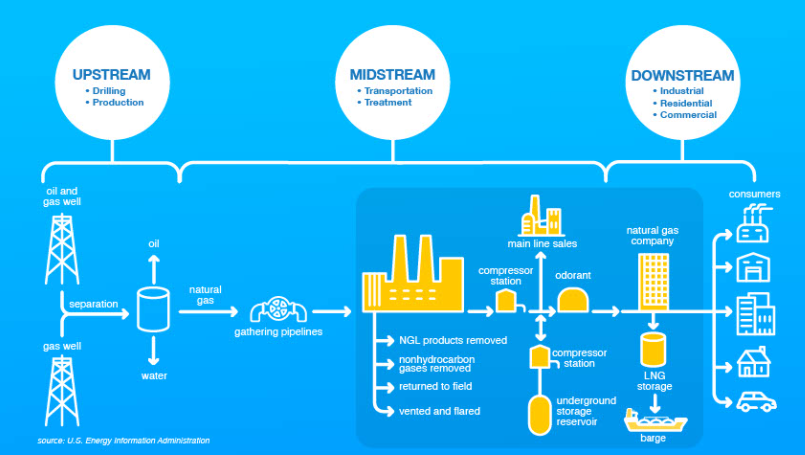

Energy infrastructure, also known as “midstream,” are the pipelines, processing plants, and storage facilities that transport energy across the U.S. If you live in the U.S. South, there is a good chance your natural gas has been transported by assets owned by either Williams Companies or Kinder Morgan. These two companies own and operate the largest portfolios of natural gas pipelines in the U.S. They each gather, process, and transport natural gas for their customers, namely oil and gas companies, refiners, and utilities. Given the mission-critical nature of these assets, energy infrastructure companies enter into long-term contracts with their customers to ensure they earn an acceptable return. This effectively eliminates commodity price risk from their revenue stream and allows for the return of cash to shareholders through generous dividends.

MLPs Versus C-corporations

The midstream investing universe is comprised of both Master Limited Partnerships (MLPs) and traditional corporations (C-corps). At Crawford, we focus exclusively on C-corp energy infrastructure companies for a number of reasons, primarily to avoid complicated tax issues including annual K-1s that are produced by MLPs. The C-corps we own also have stronger governance policies. We feel that many MLPs have had a poor track record of governance, and in some cases, the alignment between management and investors can create conflicts.

Energy Infrastructure and the Environment

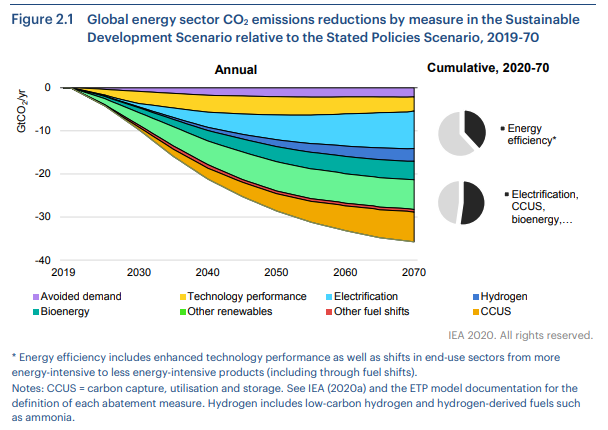

Energy infrastructure companies are already playing a pivotal role in reducing carbon emissions in the effort to reduce global temperatures. Carbon Capture Utilization and Storage (CCUS) is a material component of this effort as shown in the graph below. Additionally, through adding natural gas processing capacity, energy infrastructure companies are reducing the need for gas flaring. Gas flaring releases pollutants such as sulfur dioxide and methane into the atmosphere.

Conclusion

We will continue to invest alongside the highest quality energy infrastructure equities that are also contributing to the global effort to de-carbonize. We feel the corporations we own have mission-critical assets, ample free cash flow, good balance sheets, and generous dividend yields.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security or sector. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security or sector.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-160

You Are Here: Intersection of Quality and Value

Crawford seeks to be at the intersection of value and quality. Here is how we get there.

The Uncertainty of Investment Returns

As a stock market investor, there are few guarantees. However, we believe if one has a well thought out discipline and remains invested, suitable results follow.

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.