Crawford Investment Counsel’s Equity Research Team is as much a team of business analysts as we are portfolio managers and stock pickers. We seek to find good businesses, which can be defined as consistent, quality companies with a high return on invested capital (ROIC). We seek to invest in these types of companies when they are trading at attractive or fair prices. Since different strategies at Crawford have unique parameters for investment, some opportunities will align with one strategy or another at any given time.

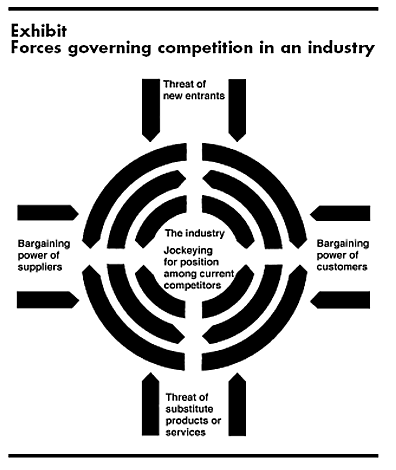

A tool we use to help assess a business’s sustainable competitive advantage is Porter’s Five Forces, a mental model penned by Harvard Business School Professor and Strategist Michael Porter.

Source: Harvard Business Review

Source: Harvard Business Review

Perhaps an illustrative example of a stock candidate will be most useful to highlight how we employ this mental model in our quest to find suitable, timely candidates for Crawford portfolios. In the case of Hanes Brands (HBI), despite the fact that this is a well-known brand of underwear that many are familiar with, the company is smaller in terms of its overall market capitalization. In addition, we feel the generous dividend yield is attractive to income-seeking investors. So, this company is a good candidate for our portfolios that focus on smaller market capitalization companies or where high income generation is a primary portfolio objective.

Hanes Brands is the leader in the $22 billion North American underwear market, with market share approaching 30%. Most likely borne of their dominant market share, HBI’s ROIC has remained fairly steady over the last several years. We believe this can be largely attributed to the Hanes brand equity within the North American innerwear and underwear markets as well as a lack of innovation and perhaps underinvestment by their largest competitors.

Regarding the center force, industry rivalry, the innerwear industry is largely a quadropoly, with Hanes commanding leading share followed by Fruit of the Loom, Gildan, Jockey, and a handful of other smaller brands. Generally, with oligopolistic industry structures, the leading players are loathe to make large disruptive changes (with respect to price, innovation), and market share stasis is not uncommon. That has been the case in the underwear industry for the past few years, and we expect that stasis to continue, which should bode well for dominant market-share-player Hanes.

Regarding the bottom force, threat of substitute products or services, we think HBI is well-positioned. We struggle to see obvious substitutes for underwear.

Regarding the top force, threat of new entrants, Hanes has experienced some competition from more forward-thinking, innovative athleisure brands like Lululemon and Underarmor in sports bras and ThirdLove in form-fitting bras. Given the oligopolistic nature of the underwear industry and the fact that a reasonable amount of invested capital is required to produce units at scale to be profitable, we think the threat of new entrants is fairly low.

Regarding the left force, bargaining power of suppliers, HBI is somewhat vertically integrated, thus alleviating potential pressure from a handful of overly important suppliers. HBI does have some contract manufacturers in greater Asia who have some bargaining power with respect to price and delivery times, for example. HBI is sufficiently diversified among suppliers of key materials like cotton and other textiles. Consequently, we think HBI stands up well against bargaining power of suppliers, and we think a Cost of Goods sold crimp to Gross Margins is unlikely.

The right force, bargaining power of customers, may arguably be HBI’s weakest Porter force. Walmart (WMT) and Target (TGT) are roughly 25% of sales, and both of those customers can (and do) exert undue power over HBI. We don’t expect this to subside, and we note HBI’s market share at WMT is approaching 40%, better than its overall industry average. We view this as a potential weakness in that WMT may be able to command better pricing (and thus lower margins for HBI) if they play some of the smaller market share players off of HBI’s dominant position. We remain vigilant to this potential risk to our HBI investment.

In sum, our analysis of Porter’s Five Forces as it relates to a potential investment in HBI concludes that:

- HBI has a reasonable competitive advantage borne of strong brand equity coupled with effective marketing and pricing, which has resulted in dominant market share (especially in the supercenter channel) and ROICs in the low teens.

- We continue to watch changes in market share in innerwear, keeping a close eye on key competitors, including Fruit of the Loom, Gildan, and Jockey.

- As the leading trusted branded player, HBI enjoys a price premium to its peers, which we believe allows it to exercise better marketing spend per unit, and the profits from this leading market share flywheel can be reinvested into better innovation across many innerwear SKUs (Stock Keeping Units).

- We continue to watch changes in market share in innerwear, keeping a close eye on key competitors, including Fruit of the Loom, Gildan, and Jockey.

- HBI’s potential Achilles heel, which bears continued vigilance, relates to its lower bargaining power relative to these supercenter players, particularly WMT at 14% and TGT at 11%. Could either of these two critical customers exercise undue economic power over HBI whether by demanding superior pricing (resulting in lower HBI margins at these key, larger accounts) or replacing HBI SKUs with competitors’ products? Either of these presents a potential risk and perhaps future negative catalysts to HBI’s stock price performance.

This type of analysis helps us to anticipate changes in market share, capital allocation, and competitor behavior, among other potential changes over the life of an investment. We continue to apply Porter’s Five Forces of critical thinking to each potential investment for Crawford equity strategies. This analytical vetting of each idea helps us identify future risks as well as potential positive catalysts for businesses we consider for inclusion in Crawford equity strategies.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-158

Interview with Frank Pinkerton: Core Equity Portfolio Manager

Interview with Frank Pinkerton: Core Equity Portfolio Manager

Interview with Aaron Foresman, CFA: Managed Income Portfolio Manager

Interview with Aaron Foresman, CFA: Managed Income Portfolio Manager

The Role of Stocks & Bonds in a Balanced Portfolio

Owning a portfolio of companies that regularly increase their earnings and dividends is a powerful force.