The recent surge in cryptocurrencies has many wondering if they should join the rise. Cryptocurrencies, most notably Bitcoin, have been famed for their high returns, high volatility, and what many believe to be low correlations with traditional assets. If you’re at all familiar with our time-tested investment philosophy at Crawford, you know that we caution investors against getting caught up in fads and what the market appears to be appreciating over the short term. Part of our philosophy acknowledges that the future is uncertain. This is why we prefer to stick with time-tested investments that we feel not only demonstrate unusual consistency but also produce income and attractive total returns.

Although we cannot predict the future, we do note that the market is currently appreciating cryptocurrencies and has recently done so at a remarkably rapid clip. Before embarking on this review, we want to be clear that crypto assets are not something we anticipate to actively manage for our clients. To put it bluntly, crypto assets in their current state violate virtually every tenet of our investment philosophy at Crawford. In short, we are focused on reducing volatility through investing in high-quality stocks and bonds, and we’ve consistently sought to apply this investment discipline for over 40 years now. So what are crypto assets anyway?

Bitcoin was the first cryptocurrency, and today it is the largest and most successful among a growing number of crypto assets and related enterprises. Many have cited Bitcoin as the “North Star” for the digital asset space. In other words, its trajectory serves as a compass for the evolution of the broader ecosystem. For this reason and simplicity’s sake, we will use Bitcoin to explain both the merits of crypto assets and the technical architecture of blockchain.

The best place to begin is at the beginning. It all started in 2008 when a whitepaper by an anonymous author writing under the name Satoshi Nakamoto put Bitcoin on the map. This paper, “Bitcoin: A Peer-to-Peer Electronic Cash System,” marked the birth of Bitcoin, as Nakamoto proposed a new way to transfer value over the internet. It is important to note that this was not the first peer-to-peer payment solution ever to be proposed, but Nakamoto succeeded where others had failed because of his novel solution to the problem of digital scarcity. Today, Bitcoin has two primary uses: it serves as a means of payment and store of value. Bitcoin’s place on what Nakamoto refers to as “blockchain” is what makes this possible.

Crypto assets, including Bitcoin, are built on a blockchain, which at its core is a distributed ledger that is permission-less and managed on a decentralized basis. It relies on decentralized trust and is censorship-resistant in nature, as there is no single person, corporation, government, or entity controlling it. It’s a single distributed database available to everyone, where anyone in the world can view balances and submit transactions at any time. The problem Nakamoto solved was how to ensure both the security and the synchronous updating of a database that is used across millions of users worldwide, and again – he solved this problem through creating digital scarcity. To truly understand Bitcoin, and cryptocurrencies more broadly, one must understand the technical structure of blockchain.

Blockchain enables what is referred to as a consensus algorithm. Through a combination of clear incentives, cryptography, and other technological advancements, blockchain creates timely, bad-actor-proof consensus across all copies of a decentralized and distributed database. The actors on the blockchain are both the individuals looking to make transactions and the “miners” which are aggregating, proposing, and settling those transactions. Essentially, miners are powerful computers that are scattered around the world, forming a critical part of the Bitcoin network and competing with one another for the right to settle the next “block.” A block is simply an aggregated group of valid, new transactions, and the competition involves solving a challenging mathematical puzzle. The miner who solves this complicated problem earns the right to propose the block, and finding the solution and proposing the block comes with a reward: newly minted bitcoin and transaction fees.

Once the puzzle has been solved, the winning miner posts the solution and proposes the block of transactions to the network. It is important to note that this is a highly technical system in which solving the problem is difficult, but checking the result is easy. The competition to settle the next block of transactions is contingent on the solution of the previous block, so there is great incentive for all of the other, non-winning miners to update their copies of the database. This updating of the various copies of the database in order to solve the next problem is what “chains” together the blocks. The difficulty of the mining is programmatically adjusted on a biweekly basis depending of the level of effort miners have applied.

Related to this, one of the key features of Bitcoin is its finite supply. There will only ever be 21 million Bitcoin, and the supply undergoes a halving every time 210,000 blocks are added to the chain. This halving has historically happened roughly every four years, and there are currently approximately 18 million Bitcoin in circulation. Once the prescribed 21 million Bitcoin have been minted, miners will still be incentivized in the form of transaction fees. With a greater understanding of its technical structure, we move forward with its two primary purposes in mind: its role as a means of payment and store of value.

To begin, we’ll discuss Bitcoin’s role as a means of payment. We must note that Bitcoin is the first truly global payment system. The truth is, much of our modern lives are fully online, including banking, yet our monetary systems are stuck in the past. Bitcoin presents a new vision for how individuals might hold, send, and receive items of value. It allows money to move without a central intermediary, which we have to admit is a revolutionary feat. Verifying and subsequently transferring items of value has historically proven to be difficult, and Bitcoin has presented a novel way of short-circuiting the process of coming to consensus about the status of accounts and transferring money. On the other hand, Bitcoin has also been praised as a store of value and protection against inflation. Over this past year, investors searching for yield and alternative assets have been drawn to Bitcoin’s inflation-hedging properties. Bitcoin is often recognized as “digital gold” due to its finite supply. While equity returns are driven by corporate profits, economic growth, interest rates, and tax policy, Bitcoin’s value is instead contingent upon market adoption, network security, liquidity, supply changes, regulator developments, technological developments, and various other factors. This has led many to believe that Bitcoin is uncorrelated and more similar to commodities or currencies than it is to other cash-flow-producing instruments like stocks or bonds.

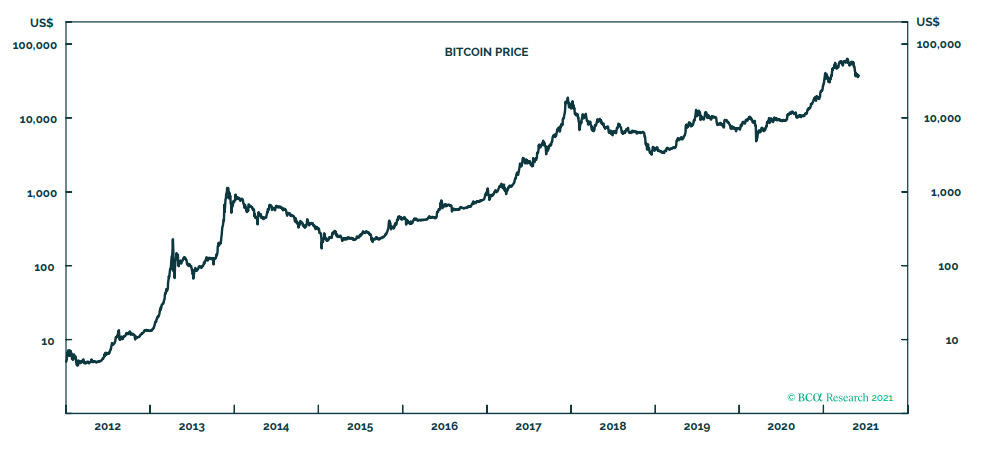

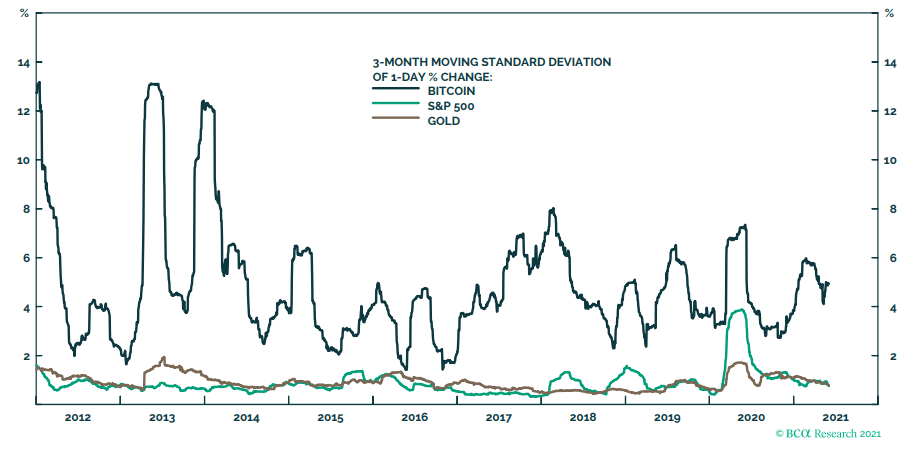

To give a brief overview of Bitcoin’s trading history since its inception 13 years ago, there have been two significant bull markets that subsequently led to two periods of significant pullback. We are currently in the midst of the third bull market today, and within the past few weeks we have witnessed what some believe to be the beginnings of a new bear market in Bitcoin and other crypto-assets. However, with Bitcoin’s 13-year lifetime in mind, we note that its rapid growth has led so many investors to become interested and attempt to join its rise. As of 3/31/21, Bitcoin’s total market capitalization was roughly $1.1 trillion. While its value has skyrocketed over a relatively short period of time, we must keep in mind that this hasn’t come without its fair share of volatility. Since its inception, Bitcoin has experienced unusually large drawdowns, sometimes in the timespan of a single day.

Source: BCA Research, 06/04/2021

Source: BCA Research, 06/04/2021

With all of this in mind, we note that Bitcoin clearly represents a new way to transfer valuable assets and money, but it is hard to predict exactly what its future might hold. For illustrative purposes, we’ve spent the majority of this paper discussing Bitcoin. However, we do want to step back and note both that it is not the only crypto asset available and also that we believe it is unlikely that one single crypto asset will come to serve every market need. To step back even further, we’d also like to add that we do recognize blockchain’s potential as an attractive technical structure and concept that could disrupt many industries. The fast evolution and adoption of cryptocurrencies has been impressive, but we feel this progress doesn’t come without its fair share of concerns. Like all things, we note that high returns don’t usually occur as a result of sound investment decisions and often are a result of speculation. For some, cryptocurrencies may prove to be fruitful, but for our clients we find the risk too great. There are great regulatory, technology, security, and scalability concerns regarding this asset class, in addition to concerns related to developing the infrastructure for investing, including custody, taxation, insurance, and capital efficiency. On another note, there are rising Environmental, Social, and Governance (ESG) concerns around the mining process that utilizes significant energy.

In conclusion, cryptocurrencies are not an asset class we recommend to our clients. This relates primarily to the fact that by owning crypto assets, in our opinion, investors must accept the risk of complete loss of capital. To us, and for our clients, this is an unacceptable outcome no matter how great the payoff may be. In fact, permanent loss of capital is exactly what our strategies are designed to protect against. Through our investment approach, we emphasize the importance of downside protection and more predictable, consistent patterns of return. In sum, the volatility currently exhibited in cryptocurrencies is directly in conflict with our investment principles at Crawford.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-156

Small Cap Research Process

(CIC) Small Cap strategy aims to deliver attractive investment returns over the long run while reducing the volatility..

Loan Growth: A Canary in a Coal Mine?

While we certainly hope for stronger economic growth and improved loan demand this year, the current environment underscores the importance of fundamental, bottom up research and active risk management.

Quality Comes Into Favor as the Fed Pivots

With some emerging concerns about a softening economy, quality is being emphasized to a greater extent, and since this is the predominant characteristic of our portfolios, this has been reflected in the returns.