By now we hope you have been able to read some of our colleagues’ perspectives as to how we at Crawford Investment Counsel view the world of investing. Our philosophy is rooted in investing in businesses for the long term, with an emphasis on quality. We believe quality improves consistency and predictability and most often begins with a consistent and growing dividend over time. While there are examples of high-quality companies across the market, we think few sectors are so densely populated with quality as the Consumer Staples sector.

Consumer Staples are among the highest quality sectors of the economy/market due to a number of reasons. Their products tend to enjoy very regular consumption patterns, leading to a narrower range of outcomes. For many of these firms, this quality is reflected in highly consistent free cash flow, driven by daily/regular demand that produces annuity-like sales and profit streams. These companies are often protected by strong brands, limited alternatives, and high barriers to entry. While the dividend and dividend history are indicators of quality, it is, however, just the beginning of our process of identifying a potential investment that provides not only quality, but also an attractive valuation and identifiable investment thesis.

Within the sector, we look for companies which we believe have sustainable competitive advantages and factors which enable their shareholders to enjoy a consistent, growing dividend over time. These include a preference for leading market share (typically #1 or #2) in their categories, which generally have a low private label presence. These characteristics help to both maintain barriers to competitive entry and preserve pricing power. We also look for companies that can grow revenue, preferably driven by volume, coupled with attractive and rising profit margins over time. These factors can manifest in lower variability of earnings, which can enable consistent cash-flow generation and high free-cash-flow conversion. Companies may generate earnings, but it’s the cash-flow generation that pays the dividend and drives long-term value of the firm. Ultimately, these firms tend to generate strong ROE (Return On Equity) or CFROI (Cash Flow Return On Investment) resulting in healthy growth, attractive margins, and relatively low investment requirements.

Other indicators of quality include strong balance sheets to enable flexibility for investment and provide a ballast in challenging economic times such as we experienced last year during the pandemic. Strong management teams – both as operators and as capital allocators – ensure good corporate stewardship and an alignment of interests between shareholders and business leaders. We favor management teams which opportunistically invest for growth where returns are high, but also like a return of cash to shareholders through a consistently rising dividend coupled with share repurchases, reinvestment back into the business, or in some cases a paydown of debt.

While not meant to be all-inclusive, we feel this list of attributes helps these companies drive attractive returns over a full-market cycle, enabling the stocks to participate in rising markets while providing downside protection in declining markets. Further, we believe the dividend income can help support the stock as investors have greater confidence in its sustainability given the business’ lack of cyclicality and management history and commitment to paying the dividend over long periods of time.

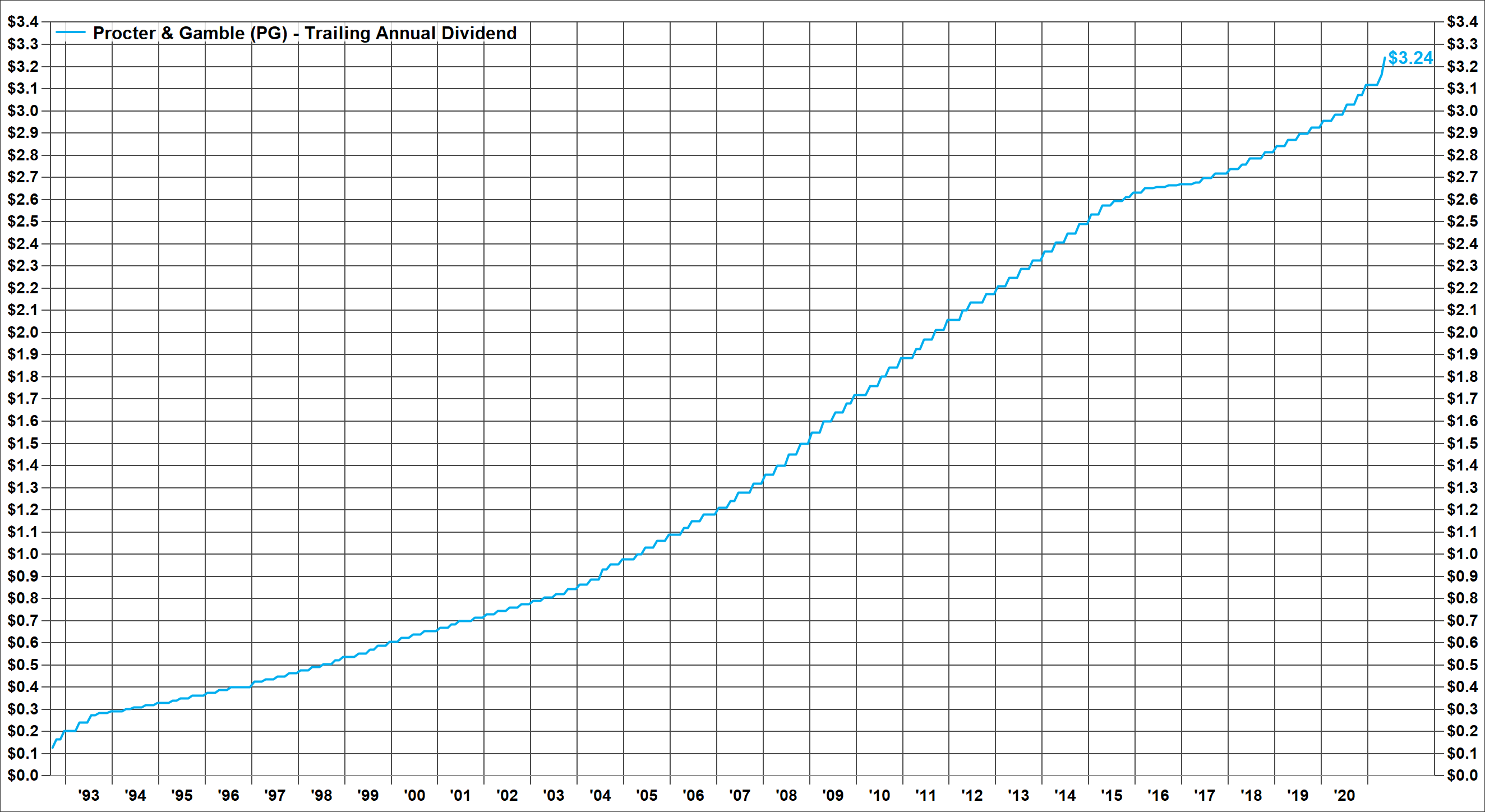

A history of consistent, preferably rising, dividend over time is an important one, in our view. Looking at the Consumer Staples sector one can see many examples of lengthy annual dividend increases over time. This consistently rising dividend pattern means often the dividend yields for the sector are higher than the market overall, potentially due to the long-tenured dividend increases over time. Perhaps one of the classic examples of quintessential quality would be Procter & Gamble (P&G), a stalwart for the sector, which has paid a dividend uninterrupted since 1890 and has increased it for 65 consecutive years. Similar to numerous other high-quality companies, P&G management’s capital allocation aligns with our view that excess cash flow belongs, and should be returned, to shareholders.

Source: FactSet

Given our quality bias and the nature of these companies, the Consumer Staples sector tends to have a prominent presence and meaningful weight in our clients’ portfolios through time. Because of the quintessential quality therein, we seek to have an allocation similar to the broader market-weight, at a minimum. Given our value orientation, our bias toward having a larger exposure would be predicated on the opportunity set and premised on attractive fundamentals and how valuations compare to history. All things equal, we would prefer a diversified exposure across the sector, including exposure to various underlying components such as food, beverages, household products, tobacco, and staples retailing stocks.

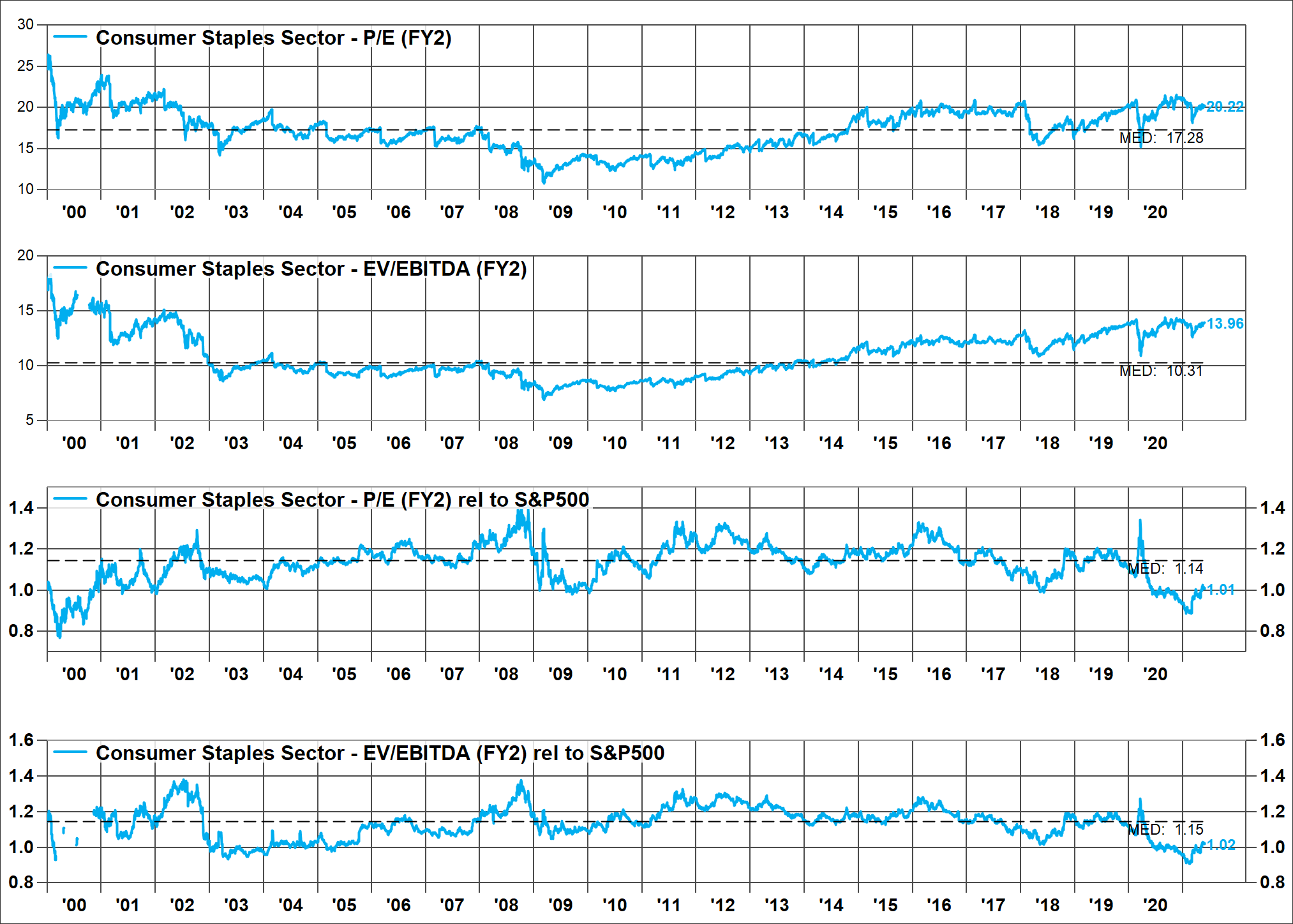

One way to arrive at the value of a stock over time is to calculate the present value of its future cash flows and dividends. As such we run a Discounted Cash Flow (DCF) analysis as a litmus test of stock value for each of our owned companies. However, because the market value/perception can often be detached from economic reality, we also compare valuation multiples, favoring cash-flow-based metrics such as EV/EBITDA (Enterprise Value/Earnings Before Interest, Taxes, Depreciation, and Amortization) or FCF (Free Cash Flow) yield. Although valuations in the Consumer Staples sector are off their recent historic lows, we believe they remain compelling relative to history, suggesting an attractive total shareholder return (TSR) opportunity. This lower valuation, coupled with high quality, leads us to a larger-than-market exposure to Consumer Staples today.

Source: FactSet

Admittedly, 2021 is a transition year amid (hopefully rightful) optimism for a renewed business cycle/ strong economy. However, looking out toward 2022 expectations, valuations for the sector are near levels seldom seen over many decades. Some of this may be attributed to potentially lower expectations for more economically sensitive company earnings, which are more highly levered to an improving economy. But as we look out over the next three to five years, we believe earnings growth from our staples companies could be similar to or better than the market overall. Regardless, we believe the inherent quality of our Consumer Staples holdings will serve our clients well in the coming years and over the long term.

In summary, we feel owning high-quality, consistent dividend-paying companies that enjoy relatively constant demand for their goods does not guarantee investment success. Owning these types of companies when they offer good value improves the likelihood of a favorable outcome, as does a deep understanding of the corporation that can only be achieved via a thorough underwriting of the business which includes rigorous fundamental analysis. The odds of success are in the investor’s favor when company fundamentals are moving forward year-in and year-out, yet expectations are modest and can be met or exceeded. We believe the likelihood of satisfactory returns is only enhanced by the presence of a dividend that can help support the share price in difficult times and add to total investment return every single year. None of this enables us to predict the future with certainty, but it’s a very good place to begin.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-155

Winning with Quality in the Consumer Discretionary Sector

At CIC, we seek high-quality companies for long-term investment.

You Are Here: Intersection of Quality and Value

Crawford seeks to be at the intersection of value and quality. Here is how we get there.

Quality as an Investment Criterion

We believe that quality is a very important factor in portfolio management, but that it is fundamentally different from other investment criteria