The recent stock market volatility has sharpened investor focus on several interconnected economic challenges such as supply chain disruptions, inflation, and higher interest rates. While the exact root causes of these phenomena can be debated, their impact on the economy continues to reverberate. Importantly, some of these pendulum shifts such as elevated inflation and the attending rise in interest rates have started to negatively impact profitability of companies across a variety of industries. We have observed profit margins of industrial and consumer companies being pressured by raw materials costs, retailers foregoing profits due to out-of-stock conditions, and even technology companies unable to source the necessary components for their end products. In this article we contend that in the face of these headwinds, banks and, by extension, bank stocks are poised to do relatively well. For the purpose of this article we will use the term “bank” to denote what we characterize as a traditional, “Main Street” regional bank that is not heavily involved in securities trading and other capital markets activities.

Before we dive deeper into the reasons for our constructive outlook regarding banks, we believe it would be helpful to provide a quick overview of how these businesses make money. For a typical “Main Street” bank, Net Interest Income (NII) represents the largest source of revenue. NII is simply the difference between a bank’s interest income, which is generated from lending activities, and interest expense, which is paid to depositors and other capital providers. Net Interest Margin (NIM) is a related concept that expresses NII as a % of bank assets (loans). In a sense, a bank’s interest expense can be viewed as a “cost of goods sold” and its net interest margin as a measure of profitability akin to the gross margin for a non-financial business.

While banks often compete with each other on interest rates they charge for loans (i.e. price of credit), the highly competitive nature of the industry keeps these pricing deviations at a relatively minor level. On the other hand, industry-wide loan pricing is very closely linked to the prevailing level of interest rates in the economy, which, in turn, is determined by the level of inflation. When the Fed raises its key interest rate to combat inflation, it effectively allows banks to raise their “prices” via increases to their own lending rates, which naturally leads to higher revenues. Of course, under those circumstances, banks also increase rates they pay for deposits (liabilities); however, these increases are typically smaller than increases in lending rates and are implemented with a time lag. Additionally, a significant portion of bank deposits such as checking accounts remain either completely interest-free or very low cost regardless of the interest rate environment. The combination of these factors leads to bank NIM expansion and NII growth during periods of rising interest rates. This dynamic is what makes banks an excellent hedge against inflation and higher interest rates. In essence, during times when most manufacturing companies are dealing with contracting gross margins due to rapidly rising material costs, banks have an embedded advantage of expanding gross margins due to rising interest rates. Needless to say, banks also do not have to contend with any supply chain shortages.

Given the uniquely large amount of liquidity injected into the financial system by the federal government during the pandemic, we expect that deposit costs will be increasing at an even slower pace than has been the case historically.

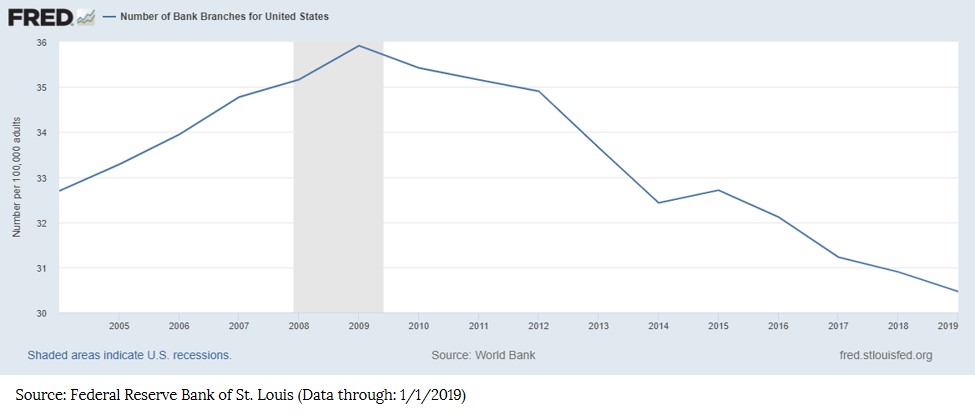

Not surprisingly, just like many other service-oriented businesses, banks themselves are not immune to inflationary pressures, particularly as it relates to higher labor costs. However, in recent years, the industry made significant investments in new service delivery channels that rely heavily on technology and substantially reduce the labor component. In many cases, customers can now conduct their banking activities without ever having to visit a branch. Account and loan applications can be submitted on-line, checks deposited with a mobile device, and funds transferred with a few clicks. Thus, the industry’s cost structure has been undergoing a meaningful shift away from personnel costs and towards automation. This is clearly evident in a steady decline of bank branch counts across the country. Because of these developments we believe banks will be relatively less impacted by rising wages and talent shortages.

In addition, we acknowledge that banks do not exist in a vacuum and are very much dependent on the health of the overall economy. Simply put, we predict that banks are not going to do well if their customers are not doing well. A recession could potentially lead to financial stress for consumer and businesses that will translate into lower demand for credit and loan write-offs for banks. Many investors still bear scars from the housing and financial crisis of 2008 – 2009. While we are mindful of this risk, we would note that regulatory capital requirement and the industry’s underwriting standards have improved drastically in the aftermath of the Great Recession. For example, we have seen that banks have largely disengaged themselves from lending to customers with weak credit histories (a.k.a. “subprime lending”), have established lower loan limits relative to collateral values, and are better capitalized.

This leads us to believe that credit-related stress will be manageable for most banks during the next downturn. Furthermore, here at Crawford Investment Counsel, we focus on investing in banks with the strongest underwriting histories, which offers additional downside protection.

In summary, we strongly believe that selectively chosen bank stocks can play an important role in protecting investor portfolios against inflation and rising interest rates. That said, not all banks are created equal. At Crawford Investment Counsel, we employ a rigorous fundamental research and due diligence process that allows us to identify banks with a high proportion of non-interest bearing deposits, well-managed expenses, and credit underwriting standards that have been tested over various economic cycles. We believe these are all key ingredients for investor success.

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-157

Neutralizing Interest Rate Sensitivity

Given the potential for rising interest rates in the year ahead, the Crawford Managed Income Strategy is a compelling option for 401k participants.

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.