With the uncertain investment backdrop and poor returns from both stocks and bonds thus far in 2022, we would like to reiterate one of our long-held philosophical priorities: downside protection. Mitigating losses in a weak market environment, like the one we are experiencing today, is a key aspect of the way we invest at Crawford Investment Counsel (Crawford). For over forty years, our strategies have proven to add value in a manner that is highly favorable for our investors, particularly when markets are in decline. We have intentionally prioritized quality, low volatility, and risk management, all of which influence our ability to participate in rising markets and protect capital when markets fall. These factors have been deeply embedded in our philosophy and investment processes since our firm’s inception. In sum, the concept of “winning by not losing” helps lead to successful outcomes for our investors.

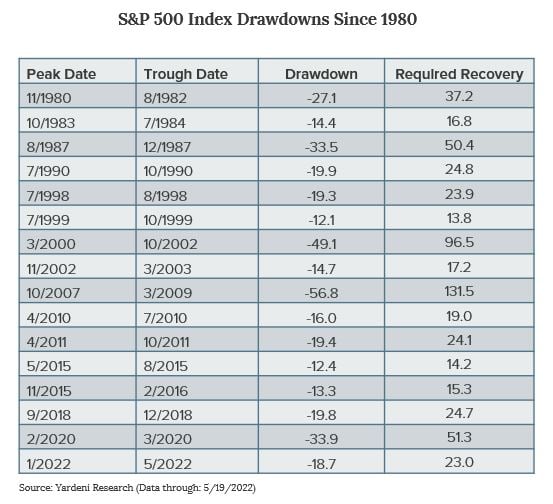

As a way to demonstrate the significance of downside protection, let’s examine recent market returns since the firm’s inception in 1980. We will look at the relationship between drawdowns/declines above 12% and the required recovery percentages to get investors back to “even,” or where they were prior to the drawdown:

In terms of percentages, the path to recovery for market averages is much more significant than the decline. This is known as sequence-of-return risk, and it is a function of the asymmetry of percentages and numbers. Many people know that a loss of 10% requires a gain of 11% to recover. What many don’t fully appreciate is that as a loss grows, so does the size of the return needed to recover. In an extreme case, if the market went down by more than 49%, you would need a double or 100% return to fully recover. This has happened twice in the past 40 years, and Crawford strategies are designed to protect against this very fact of nature.

By mitigating losses on the downside, recovery becomes more readily achievable, and impairment of capital becomes far less likely. Factors that can contribute to turning a temporary, market-driven decline into a permanent loss of capital include taking withdrawals from a portfolio to meet spending needs, abandonment caused by disillusionment and loss, and investments in lower-quality companies that simply cannot sustain their business models through difficult periods. All of the aforementioned instances exacerbate sequence-of-return risk, sometimes fully inhibiting recovery at all.

The average decline listed above is -23.8% when the S&P 500 is down over 12%. But the average recovery required to get back to prior peak levels is 36.5%. The more downside protection offered, the less this math works to the client’s disadvantage. By systematically improving on downside capture and preserving value, Crawford helps clients experience less loss, and they recover much faster than the popular averages.

Each of Crawford’s strategies has provided strong downside protection in this recent period of weak market returns. The recovery required for Crawford’s strategies relative to primary benchmarks is, on average, a small fraction of the figures above. This follows a long historical precedent made possible by the quality bias inherent in each of our strategies. We will use our Dividend Growth strategy, which is our longest tenured strategy and the firm’s flagship strategy, to illustrate this very fact.

The strategy utilizes the Russell 1000 Value Index as its primary benchmark, and for the 41.25-year period since its inception, it has outperformed in 78.05% of negative return quarters for the benchmark. The strategy’s max drawdown is 12.78% less than that of its benchmark, and the strategy’s average relative return, or outperformance, in negative return quarters is 1.91%. Over time, this has led to positive alpha, strong risk adjusted returns, and a smoother pattern of returns for our investors, all leading to successful outcomes.

We see that the reason high-quality companies exhibit strong performance over time is that they tend to be structurally advantaged in several key ways. Companies of this nature are more profitable as dictated by metrics such as return on equity, return on assets, and return on invested capital. Their higher profitability is often a function of “asset-lite” business models, which enable them to generate free cash flow to both pay dividends to their shareholders and capitalize their businesses using less debt. Additionally, their earnings variability is lower due to the less sensitive and more predicable nature of their income statements and earnings streams. Higher-quality companies simply rely less on environmental circumstances to determine their success and can persevere to a greater degree in both good times and bad. We believe these companies win “through the cycle,” not just when markets are strong.

Not only do higher-quality companies have businesses that perform relatively well in both good times and bad, but their shareholders experience a similar phenomenon. More predictable and consistent businesses tend to lead to more predictable and consistent share prices and dividend streams. These are the types of companies we prefer to own. We believe companies of this nature offer a far greater risk/reward tradeoff when compared to lower-quality, economically sensitive, and highly levered companies that are profitable in boom times, only to give much of their performance back in a recession or downturn.

These facets of higher-quality companies tend to be exacerbated and more highly valued by investors during periods of uncertainty. We intend to stick to our philosophy, continue winning by not losing, and ultimately, create more successful outcomes for our investors.

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-156

The Parable of Tom the Turkey

Our past experience makes us wary of investments that are too good to be true. We know investments that go up like an escalator typically come down like an elevator.

Demise of the Mall

With the secular trend of e-commerce continuing to grow at the expense of traditional retail, we find what we believe is a long-term investable theme.

Loan Growth: A Canary in a Coal Mine?

While we certainly hope for stronger economic growth and improved loan demand this year, the current environment underscores the importance of fundamental, bottom up research and active risk management.