One of the pendulum shifts that we believe is occurring is that we are likely moving from a period of above-average investment returns from stocks and bonds to a more normalized or lower return environment. Over time, we see that investment returns tend to be somewhat cyclical, and more pedestrian results typically follow periods of robust stock market gains. When one compares returns over the past ten years to those over the long-term, it is not at all a heroic prediction that overall returns will be a bit lower for the foreseeable future.

S&P 500 Compound Annual Returns:

10 years ended 2021: +16.52%

Since 1927 through 2021: + 9.74%

Source: Crawford, FactSet (Data through 12/31/21)

This is not to say that we do not expect to make money and produce positive portfolio results from stocks, but we do anticipate a more subdued outlook. Indeed, this has been the case thus far in 2022, and some of the factors leading to recent stock market weakness may remain headwinds for some time. To be clear, we see that this does not imply a negative return forecast and is certainly not a recommendation that investors sell stocks.

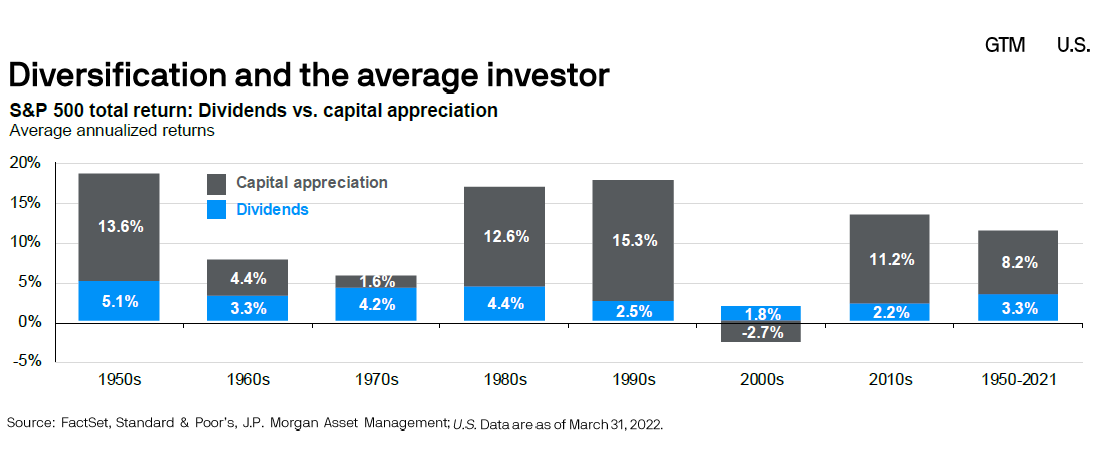

Because the market decline has caused the dividend yield to increase and to the extent that investor returns are lower, we believe the importance of income or dividend yield will be more meaningful in terms of its contribution to overall investment results. This means that higher-yielding strategies may become more favored by investors, and we have recently seen investor preferences shift towards companies that pay dividends. We believe this could be another pendulum shift within a period of lower returns overall, in part caused by the relatively modest level of income provided by the popular stock indices, in addition to potential profit headwinds and margin pressures on business.

The Crawford Dividend Yield strategy offers a well-above-average dividend yield of approximately 4% today. The portfolio's objective is to generate a yield within the eighth or ninth decile of all dividend-paying companies, meaning that the strategy will aim to produce a very high income relative to what is available in the stock market. Much fundamental scrutiny is applied throughout the securities underwriting process to ensure that the dividend is safe and secure. Also, the portfolio diversification pattern is such that the portfolio's risk level is low compared to the broader market and higher-income strategies.

Below are some displays that illustrate the empirical evidence for this strategy, along with the yield history of the portfolio.

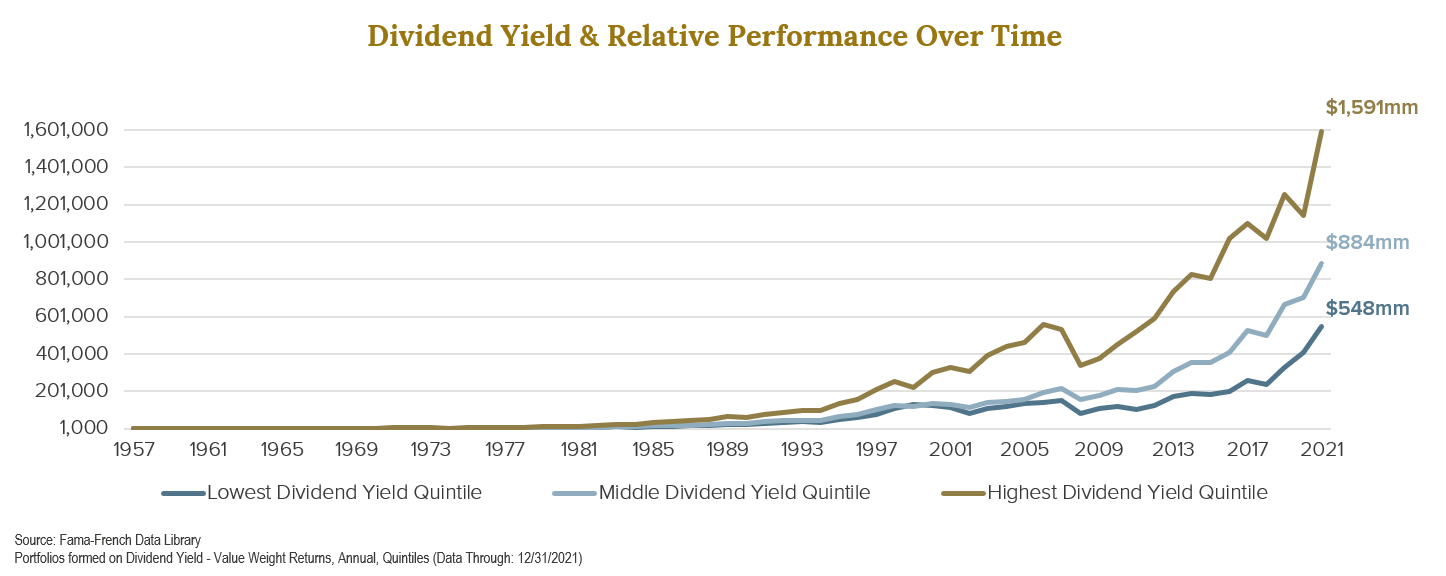

The first chart utilizes data from the Fama-French data library, which happens to be among the more robust historical data sets available for the stock market. As a result, we think the data contradicts a common misperception about higher-yielding stocks. Instead, it shows that over time, the highest dividend-yielding stocks have significantly outperformed those with lower dividend yields.

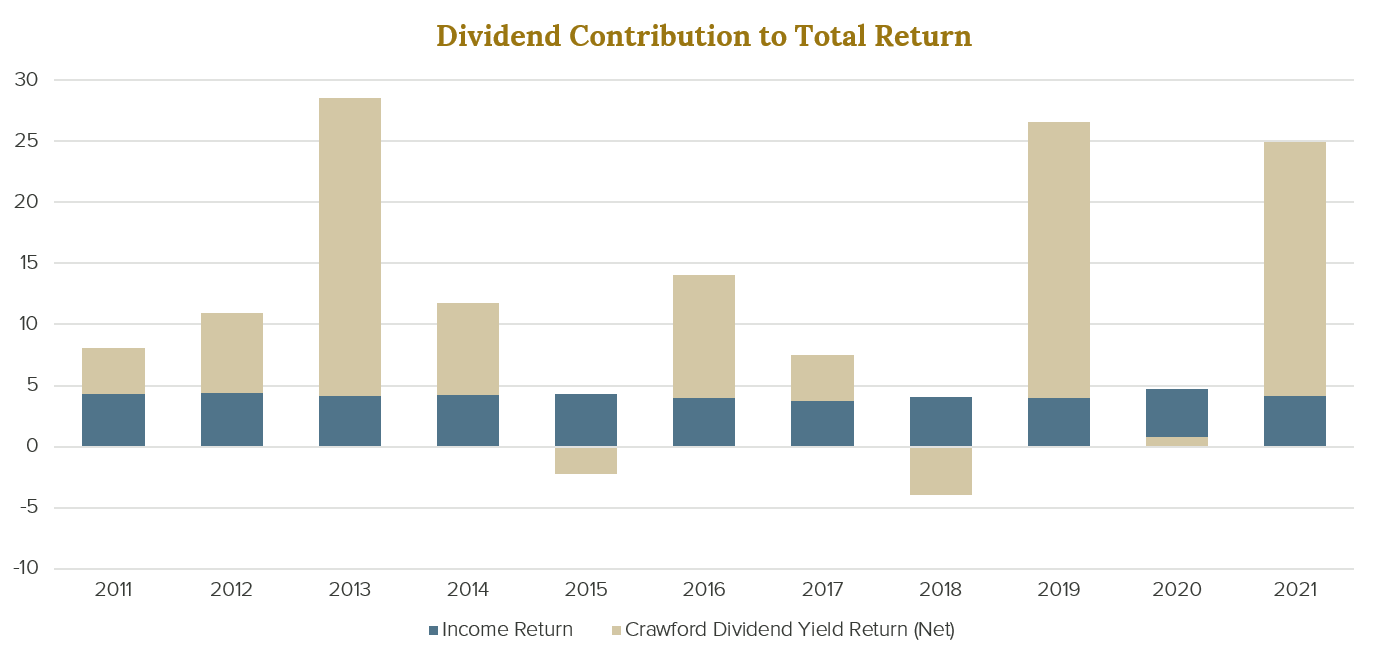

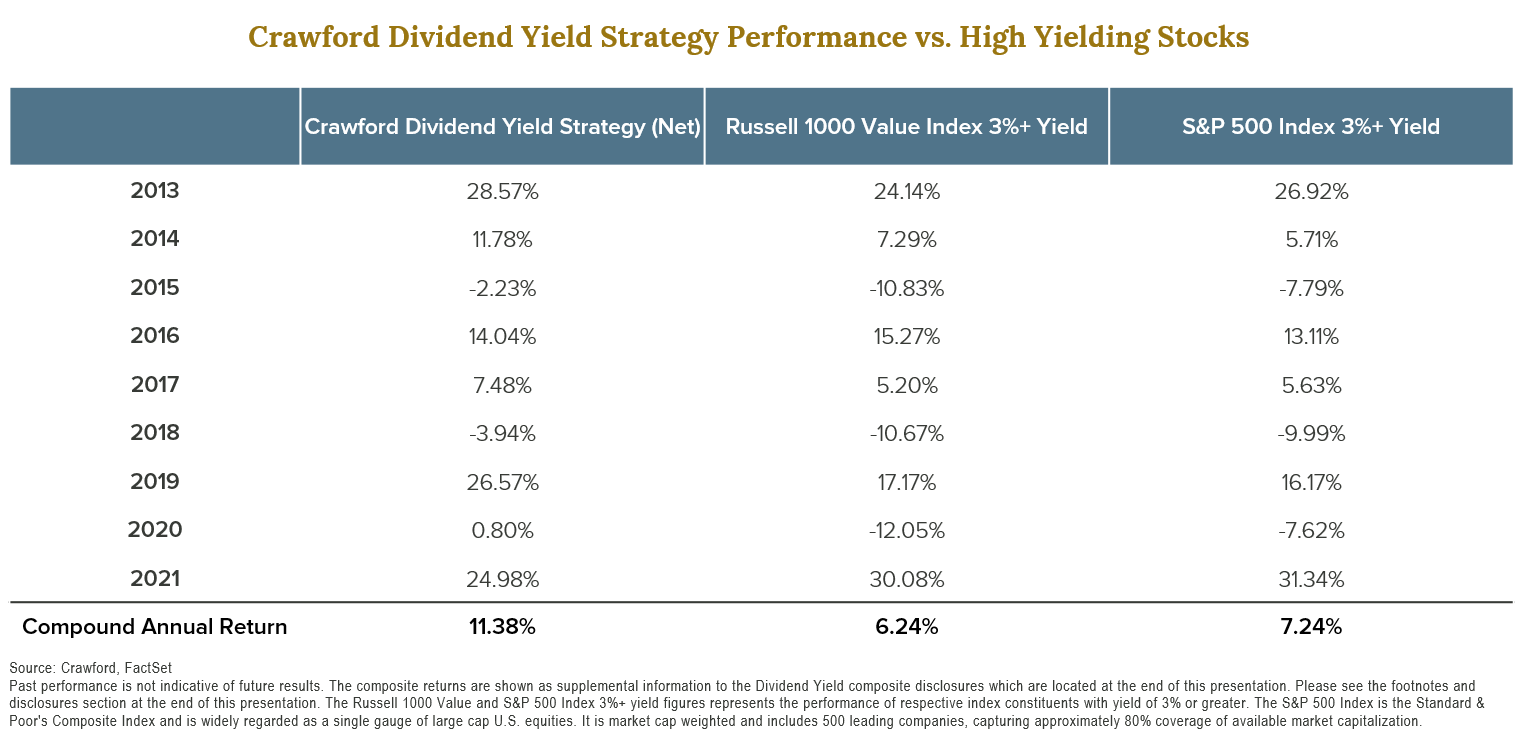

Since its inception, the Dividend Yield Strategy has achieved its primary objective of above-average income, with a dividend yield of approximately 4%. At the same time, it has provided a competitive return. And in years of market decline, the yield helped to cushion and protect on the downside.

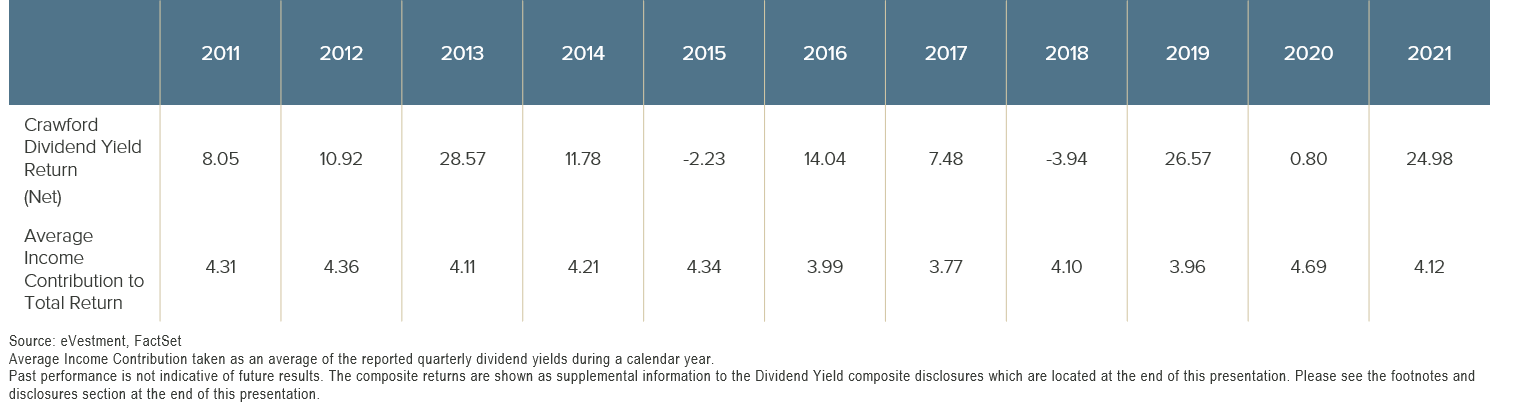

Our confidence in the Crawford Dividend Yield Strategy is further bolstered by its ability to provide what we see as competitive returns relative to higher-yielding subsets of the popular indices. The table below illustrates that the strategy has produced a strong return pattern versus the opportunity set. Additionally, the strategy has participated in up-markets and protected when higher-yielding stocks have been under pressure.

We believe the investment environment is favorable for higher-yielding stocks. As a result, the Crawford Dividend Yield strategy is well positioned to build on positive results as we move forward and look to the future.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-171

Interview with the SMID Cap Portfolio Manager

We believe clients invested in the strategy should benefit from attractive, long-term returns and a relatively low degree of risk.

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

Patterns of Returns Matter

The pattern of returns earned can be more important than absolute returns.