We are observing a number of pendulum shifts within the economy and stock market today. Many of the underlying shifts represent negative headwinds for corporate profits, including higher labor costs, higher interest expense, and the need to hold more inventory and re-examine production sources amidst a less secure supply chain. We believe these shifts, among others, are weighing on investor sentiment and causing stock prices to decline.

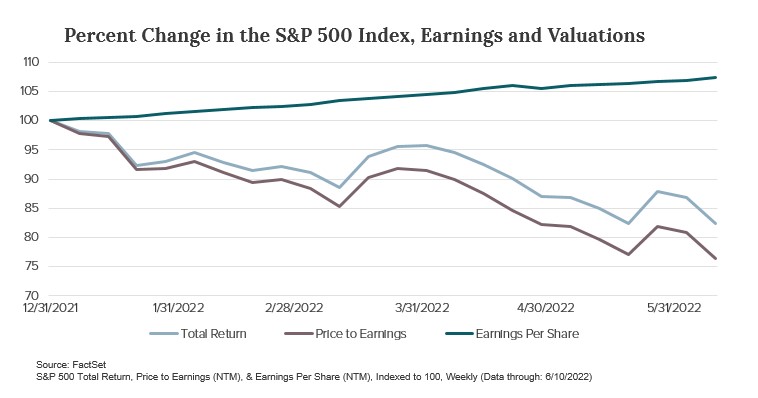

It is unclear how long these issues will persist (see our piece on secular versus cyclical change here), but we have seen earnings estimates have surprisingly continued on an upward trajectory thus far. The decline in share prices combined with stable earnings projections means Price to Earnings (P/E) ratios have declined significantly over the past six months. This comes after a long period of multiple expansion and may represent a silver lining for investors. In other words, to the extent that earnings estimates are close to being accurate, we feel today’s market environment represents an opportunity to buy stocks at reasonable P/E ratios.

We readily acknowledge that the P/E ratio is not always our preferred valuation metric, particularly for dividend-paying stocks. However, we believe it does serve as a convenient yardstick to gauge the overall valuation for the stock market. So far in 2022, earnings revisions are better than historical averages, reflecting some degree of analyst skepticism.

The big question is: What will happen to earnings? If earnings decline, then stock multiples turn out to be higher than advertised. In other words, this would suggest that earnings figures are vulnerable to the downside, meaning the valuation is actually higher than it appears. Of course, we believe this would not be a good outcome. We will know more in a few weeks once quarterly earnings are fully reported.

At Crawford Investment Counsel (Crawford), we have long believed that bottom-up investing in high-quality, dividend-paying companies gives stockholders the best likelihood of success. We have a much greater degree of confidence in our ability to gauge the fundamental and earnings outlook for consistent and predictable businesses in our portfolios than we do for the broader market, the S&P 500 Index. Our focus on higher-quality companies provides a margin of safety and narrows the range of potential outcomes. We believe this increases our likelihood of success in the process. Despite our focus on investing in individual companies, we certainly recognize the importance of overall economic and market conditions. These conditions impact corporate profits, and no stocks are exempt from some changes in the overall market.

We are observing rapidly contracting P/E ratios, but we do not yet know if the earnings estimates are too high. If the economy goes into recession, it would be typical for corporate earnings to decline significantly. We expect this relationship will hold in the future, and we know from experience that some companies weather economic downturns better than others. The good news is that the valuation has already contracted significantly in a short period of time, reflecting caution and doubt on behalf of investors. This contrasts the high degree of optimism we witnessed at the beginning of 2022, as reflected in the high valuation afforded the market and certain higher growth companies.

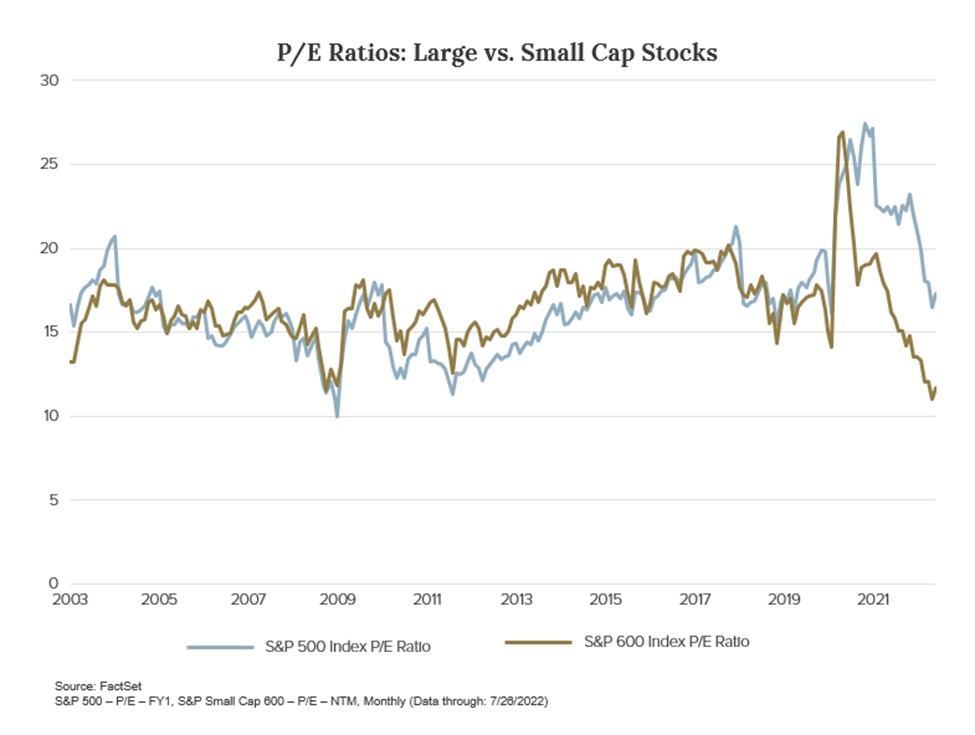

It should be noted that certain areas of the stock market can trade at different multiples of earnings. Today, smaller company stocks trade at valuations below larger capitalization companies. These smaller businesses typically have earnings that are less able to withstand slower economic growth and some of the other headwinds cited at the beginning of this piece.

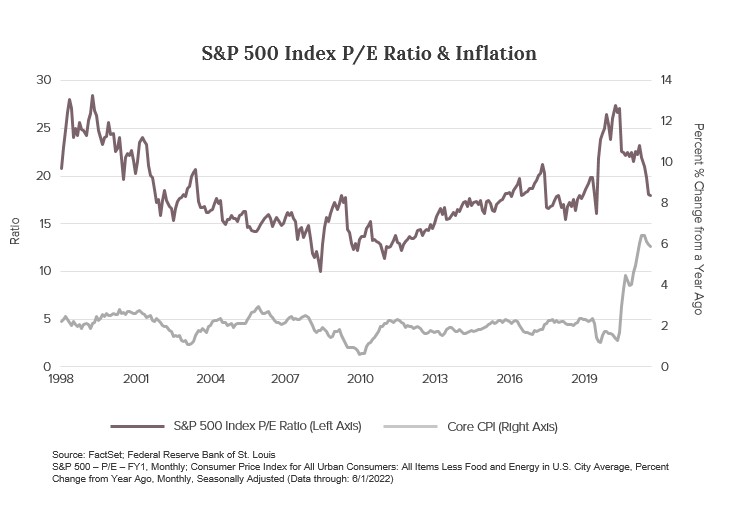

How long the P/E ratios stay compressed, or whether they contract further, will likely depend on the path of economic growth, corporate profits, and inflation. Earnings multiples typically are inversely correlated with inflation, meaning higher periods of inflation are typically accompanied by lower multiples, and vice versa.

Back to the silver lining for investors, multiples have contracted, meaning at least on the surface stocks are cheaper than they have been in some time. Our approach is to attempt to take advantage of this by investing in very high-quality companies that have durable businesses and resilient earnings and cash flow, in addition to paying dividends with an upward bias.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-205

The Role of Stocks & Bonds in a Balanced Portfolio

Owning a portfolio of companies that regularly increase their earnings and dividends is a powerful force.

.jpg?width=500&height=334&name=shutterstock_550915870%20(1).jpg)

The World is Uncertain, Just Look at Earnings Expectations

It’s no secret that more stable earnings and dividends are what we strive to seek over the longer term for our investors.

Quality: The Differentiated Investment Factor

We believe quality is a differentiated investment factor with various benefits including attractive long-term returns, protection in market declines, smoother patterns of return, and income production.