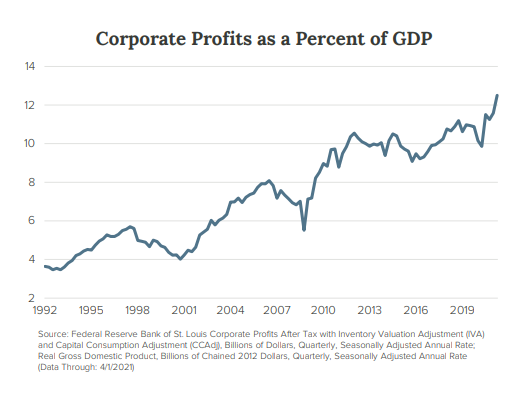

Many observers of the stock market seem to be amazed at how well common stocks have done over recent years. For instance, over the last five calendar years ending at the end of 2021, the S&P 500 has returned at a compound rate of around 18%, some 80% above its longer-term return. We could cite similar return patterns over longer time periods, but this outperformance by stocks leads to the question of why stocks have been doing so well. We think the answer is obvious. See the chart below.

We are very impressed with the message from this chart and at the same time are surprised that more observers are not. The message is a simple one: corporate America has been garnering a greater and greater share of overall economic wealth for a long time. Corporate profits as a share of real Gross Domestic Product (GDP) have risen inexorably since the early 1990’s, going from less than 4% of GDP to over 13% at the end of 2020. The message is clear: corporate America has either been doing some things right, or they have benefited from secular trends in the overall economic environment. Either way, and the answer is most likely both, the result has been of great benefit to holders of common stocks. A juggernaut is defined as an overwhelming force, which seems an apt description of corporate America in this context.

Lying behind the rise in corporate profits is the story of margin expansion (they reside at all-time high levels now), above-GDP revenue growth, increased leverage, increased monopoly and monopsony power, lower corporate taxes, the benefits of globalization, and diminished regulation, among others. All of these elements have contributed to the remarkable corporate performance relative to the overall economic environment.

The use of numbers can put this extraordinary picture into perspective. While the chart shows corporate profits as a percentage of real GDP, we like to compare all corporate performance against nominal GDP, since nominal represents the real world in which they compete. In other words, if inflation is enlarging GDP, it means that corporate America is having to deal with that inflation as they compete in the real world. Over the 1992 to 2020 period, nominal GDP grew at a compound rate of 4.56%. Corporate profits, however, compounded at 7.37%. That is the difference.

It has been a great run for corporate America; can it continue? The answer to that big question depends on a lot of things, but we would suggest that while the corporate sector has been very innovative and creative, they have also benefitted greatly from the longer-term trend of declining worker power. Declining worker power is a way of describing a major shift from labor to capital that has been going on for decades.

Beginning in the 1980’s, declining worker power can be observed in the sluggishness of real wage growth, a declining share of national income by labor, and declining unionization. These trends, all signs of diminished worker power, point, on the other hand, to rising profitability by corporations and the ability to increase markups between the cost to produce a good or service and its selling price. This is a potential explanation of margin improvement by corporations.

Economic power can be assumed to reside in monopoly, monopsony, and workers. Workers are in constant competition with the other two. Monopoly power is a factor in our economy that has been on the rise. It is easy to identify sectors or industries where one or a few corporations have constructed moats around their business, giving them unusual power over workers who may be working in those companies. Monopsony, where a company dominates a city or region as the principal employer to the exclusion of others, exercises great power over that labor market. The fact that workers in that area have only one option limits their power. Worker power derives mainly from unionization or the threat of it and from firms that choose to run their businesses in the interest of all stakeholders, including workers. A condition of full employment also empowers workers, to a certain extent.

We point to an additional factor that tends to limit worker power: the growing presence of technology in business. The use of technology implies greater productivity per worker, which in essence, reduces the need for additional workers and can lead to a weaker overall labor market. This trend seems to be well in place for the foreseeable future.

Within this framework of competing economic power, monopoly and monopsony have been the winners, and workers, the losers. The result has favored corporate America and has been one of the chief contributors to higher corporate growth.

This article, in attempting to partially explain why corporate America has been so successful in recent decades, makes no judgment as to the virtues of economic power in any of its forms. We of course are very pleased that corporate profits have been growing at a higher rate than the economy, and this has been to the direct benefit of shareholders. This we applaud. At the same time, we believe it would accrue to the benefit of overall economic health were there to be more balance between corporate and worker power. As corporations garner a larger and larger share of total wealth, it accentuates income and wealth inequality and has a tendency to reduce overall demand.

Back to the original question: can the corporate juggernaut be stopped? In our estimation, probably not. We believe the outlook for corporate profit growth remains strong, and this represents a dynamic support factor for common stocks. As profits continue to rise, we expect stocks to do so also, especially over the longer term. The forces working in favor of corporations seem likely to continue, although workers could see improvement if government policy were to change to make unionization easier, if the minimum wage were to be raised, and if more companies were to adopt an attitude of less shareholder activism. These changes, the beginnings of which are now small, have a long way to go.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-22-064

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

Why Dividends Matter: Downside Protection

One of the more favorable aspects of investing in dividend-paying stocks is their ability to help protect capital in declining stock markets.

What is a Preferred Stock?

Preferred stocks are equity securities that are required to pay interest or dividends before common dividends are paid to common stockholders.