In the early 1980’s the popular Wall Street economist Ed Yardini coined the phrase “bond vigilantes” as a way of describing the power of the bond market to be a check on poor government action, particularly with regard to deficits and debt. To be vigilant is to watch and observe; to be a vigilante is to take matters into one’s own hands, sometimes with violence. There have been more than several instances when the bond market has rioted over government extremes, striking fear into policymakers’ hearts. These riots take the form of rapidly rising bond yields, thereby raising the cost of financing the deficits. None less than President Bill Clinton was fearful of the bond vigilantes and was influenced to take a conservative fiscal course that led to the first balanced budgets in many years. The bond vigilantes were a force to be contended with in their day.

Fast forward to today when fiscal policy is extremely easy to the tune of some six trillion dollars of Covid-related relief, another trillion of infrastructure spending on the way, and the potential for two trillion or so in the proposed Build Back America bill. The U.S. government is facing its largest budget deficits on record, and government debt as a percentage of Gross Domestic Product (GDP) is over 100% and still rising. In the face of these extremes, the bond market remains surprisingly calm. The benchmark 10-year U.S. Treasury note now trades at a yield of roughly 1.50%. Given these circumstances, one might appropriately ask, “Where did the bond vigilantes go?” Have they disappeared?

Some observers have offered the opinion that through quantitative easing, the Federal Reserve (Fed) has more or less neutered the government bond market by buying U.S. Treasury securities so aggressively that they can control the market. We doubt this. Even though the Fed has bought roughly four trillion dollars of U.S. Treasuries since March of 2020 and now holds almost 25% of the outstanding Treasury issues, that still leaves 75% of the market in private hands, which is free to join the vigilantes at any time.

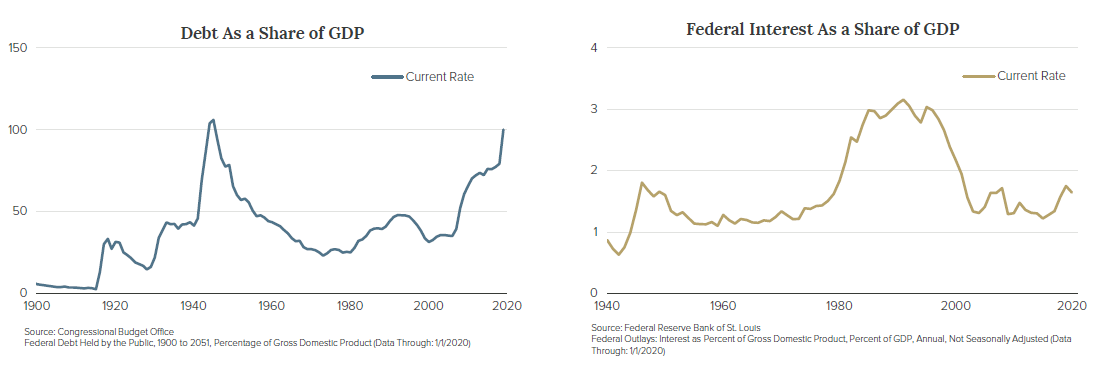

We offer another explanation. We suggest that no, the vigilantes have not gone away. They are still watching, but what they are seeing is not that disturbing to them. In a sense, they have been converted to a different line of thought. The vigilantes still have the potential to riot, but they don’t see the need just yet. We suggest that the bond vigilantes have been converted by one fact and one assumption. FACT: much larger deficits can be sustained due to the very low interest rates that dramatically lower the cost of financing the deficits. ASSUMPTION: this condition will remain favorable because interest rates are going to stay low for a long time, thus enabling the fiscal deficits to be sustained. One might assume that the vigilantes have observed and considered the implications of the information contained in the following charts.

The vigilantes probably have not decided that deficits do not matter, but they may appreciate how much the situation has changed. The charts illustrate just how much federal debt has grown over the last 20 years, but even more startling is the decline in the cost of financing that debt. This opens up the possibility of vastly more federal borrowing at a much lower total cost. Consider for example an additional trillion dollars of government debt that was financed 20 years ago at 4%. It would cost the government 40 billion dollars a year to pay the interest on that debt. Now, considering an average of yields across the maturity spectrum, that trillion dollars of new debt could be financed at roughly 1%, or some 10 billion dollars per year. Looked at another way, the government could issue four trillion dollars of debt for the same cost as its one trillion. This does not even assume the real cost in terms of the real yield, which is actually below zero. The conclusion: a great amount of debt can be financed at very low rates, which opens up the possibility of much larger amounts of government debt without the burden of high costs to service the debt.

The costs of federal debt are facts. The assumption is that interest rates will remain low, and therefore, carrying the extra debt can be sustained. This is a critical assumption, for much higher interest rates in the future combined with larger debt would be economically damaging. In our opinion it would be aggressive to assume that interest rates in the future stay as low as they are currently, but we believe it is fairly sound to conclude that the era of generally low interest rates is not over, and will not be anytime soon.

Of all the economic events of recent decades, none is more striking than the large and sustained decline in interest rates, both domestic and global. It may be assumed that because the sustained downward trend has been global in nature, and because the declines have been consistent across all maturities, both long and short, the decline is a real phenomenon, not just a monetary one. In other words, interest rates are not low because the Fed decided to take them there; they are low because of structural changes in the economy. And these structural changes are most evident in the propensities to save and invest.

It is important to keep in mind the saving/investment dynamic as a fundamental driver of the economy. As private savings are transferred into private investments such as new plants or factories, computers, software, and other information technology, growth is created. When that transfer is not accomplished there is stagnation. Savings just pile up in a glut, weighing down on interest rates. There have been forces that are working to increase savings at the same time that other forces are working to discourage investment. Those factors working to encourage savings are longer retirement periods, increased inequality, and rising uncertainty. Those factors working to discourage investment are slowing labor force growth, greater efficiency in the use of capital, and the influence of information technology in reducing the need for large capital investments. The corporate sector also may be a contributor as they succumb to shareholder demands for more dividends and buybacks. Our observation is that these trends seem well entrenched and are likely to be continuing factors in the inability of the private sector to absorb private savings into investment.

There is certainly room for interest rates to rise from current levels, assuming the economy remains on course for recovery and expansion. Will the bond vigilantes come alive and drive interest rates to significantly higher levels? We doubt it, for we believe the bond vigilantes, and by inference the bond market, is viewing the world differently. Until the secular forces we have discussed begin to change, that is, until the economy changes structurally, we believe the vigilantes will remain quiet.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

The opinions expressed are those of Crawford Investment Counsel Inc. Investment Team and are subject to change without notice. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Crawford Investment Counsel Inc. reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no guarantee that Crawford Investment Counsel Inc.’s assessment of investments will be correct. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not take into account specific client investment objectives.

CRA-21-387

The High-Grade Bond Market Today: Compressed Yields & Longer Duration

Since the Global Financial Crisis, changes in the U.S. high-grade bond market are exposing passive fixed income investors to a heightened level of risk.

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.