Over 100 years ago, noted Swedish economist Knut Wicksell wrote,

There is a certain rate of interest which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.

Thus, the concept of a natural rate of interest came into being. The natural rate can also be referred to as the “neutral” or “equilibrium” rate, and economists refer to it as R*. The use of equilibrium as the descriptive term is helpful, we believe, for the natural rate is the interest rate that should be achieved when all or most aspects of the economy are in equilibrium. When the economy is in balance and performing as it should, absent either demand or supply shocks, interest rates should be naturally set at a certain level.

Early in this century the San Francisco Federal Reserve revived the concept of a natural rate and began estimating it, led by the work of John Williams, now the President of the New York Federal Reserve. The Laubach Williams model is currently the most widely accepted standard for estimating the natural rate. In the wake of the Great Recession, Larry Summers, chief proponent of the secular stagnation theory, did considerable work on the natural rate and brought the consideration of it to more prominence. To precisely define the natural rate we quote John Williams: “…the natural rate is defined to be the real federal funds rate consistent with real GDP equaling its potential level (potential GDP) in the absence of transitory shocks to demand. Potential GDP, in turn, is defined to be the level of output consistent with stable price inflation, absent transitory shocks to supply. Thus, the natural rate of interest is the real federal funds rate consistent with stable inflation absent shocks to demand and supply.”

The natural rate is theoretical, that is, unobservable, but it is nonetheless of extreme importance to both policymakers and investors. Since it is a theoretical rate, estimating it correctly is never easy, but it is certainly worth the effort. For policymakers and investors there is always the question of where future interest rates are going. Knowing where the natural rate is can be very helpful in this undertaking. If an investor knows where the natural rate of interest will be, assumptions can be made about bond yields of various maturities. Perhaps more important is the role the natural rate plays for policymakers. They need to have an idea where the natural rate is, for if federal funds policy is under the natural rate, they are in a stimulative mode, whereas if their policy is above the natural rate, they are in a contractionary mode.

When considering what the natural rate might be, economist tend to think in terms of “real” interest rates since they believe that movements in the real rate influences both business and consumer decisions moreso than nominal interest rates. And, it is important to think about the natural rate, not as what the optimal rate is now, but more in the range of the next few years when hopefully any excesses or imbalances in the economy will be brought more toward equilibrium.

A simple exercise may be helpful in putting the natural rate in current context. The Federal Reserve (Fed) is estimating that some time over the next several years they will settle in with a federal funds rate of about 2.5%. This so called terminal rate is really a proxy for the real natural rate, plus an adjustment for inflation. This means that they believe the real natural rate is around .50%, adjusted upward by their current targeted growth rate of inflation of about 2.0%. If the real natural rate is .50%, since the Fed is in an easy money posture, they want real federal funds to be below .50%, which it is at its current level.

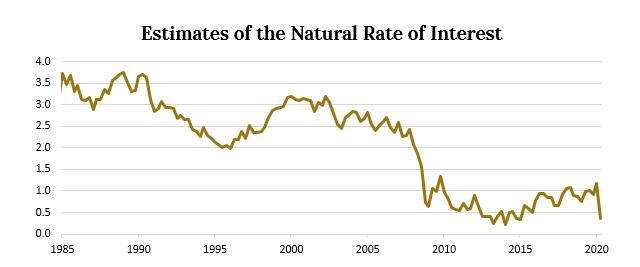

The Laubach Williams model has portrayed a steadily declining natural rate since 1980, in line with steadily declining nominal rates.

Updated estimates of the baseline model described in "Measuring the Natural rate of Interest," by Thomas Laubach and John C. Williams (Data Through: 2Q2020)

There are a number of reasons for the steady decline in the natural rate. Summer and Rachel in a 2019 paper discuss a number of factors that naturally tend to raise the natural rate, as well as factors that naturally tend to lower the natural rate. Essentially, changes in government policies such as spending for Medicare and Social Security as well as increases in government debt are factors that would exert upward pressure on the natural rate. However, these factors have been outweighed by negative forces such as the decline in productivity, slowing population growth, technology, and inequality. Overall, the negative forces have been more dominant, steadily reducing the natural rate over time. Importantly, these conditions are likely to remain in place far into the future, thus suggesting a lower interest rate regime for a long time.

The natural rate is always subject to change, depending on economic factors. There is open debate currently as to whether the Fed is mistakenly estimating the natural rate too low based on developments in the wake of the Covid pandemic. Above we note the upward pressure on the natural rate from government debt, which of course exploded to the upside in 2020 and 2021. Pandemic relief totaled some six trillion dollars over the two year period, thus creating huge deficits that needed to be financed with government debt. This could be a game changer. It is possible that the surge in government debt was sufficient to change the direction of the natural rate to a higher level. If so, the policy implication is clear. The Fed would find itself in a much too easy mode, thereby risking an overheating in the economy and resulting inflation. The Fed is under pressure currently with inflation running at 30-year highs, yet they are still in a very aggressive stance with regard to monetary policy. It is worth noting that their stance has been slightly altered as they are beginning the tapering process of quantitative easing.

The importance of the natural rate is challenged by the fact that it is a theoretical rate and cannot be observed. Nevertheless, as we have pointed out, the assumptions about it have huge implications for policy, both monetary and fiscal. With inflation currently running very high and the question of its sustainability being debated, the natural rate of interest is a very important topic.

*For this paper we have drawn heavily from the Federal Reserve Bank of San Francisco Economic letter of Oct. 31, 2003.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security or sector. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security or sector.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-384

Generative AI: Generating Investment Opportunity

In November, the release of OpenAI’s ChatGPT marked the beginning of the commercial phase of the global race in artificial intelligence.

Innovation & Transformation: Investing in AI

Given the pace of innovation and the rapid adoption of generative AI technologies, now is an exciting time to be an investor in companies with AI exposure. At Crawford, we can take advantage of these opportunities by identifying individual companies that both meet our quality requirements AND participate in these secular growth markets.

GDP: The Economy Surprises Again

For now, we celebrate the outstanding performance of GDP. The future is not risk free, but for now, the present is pretty good.