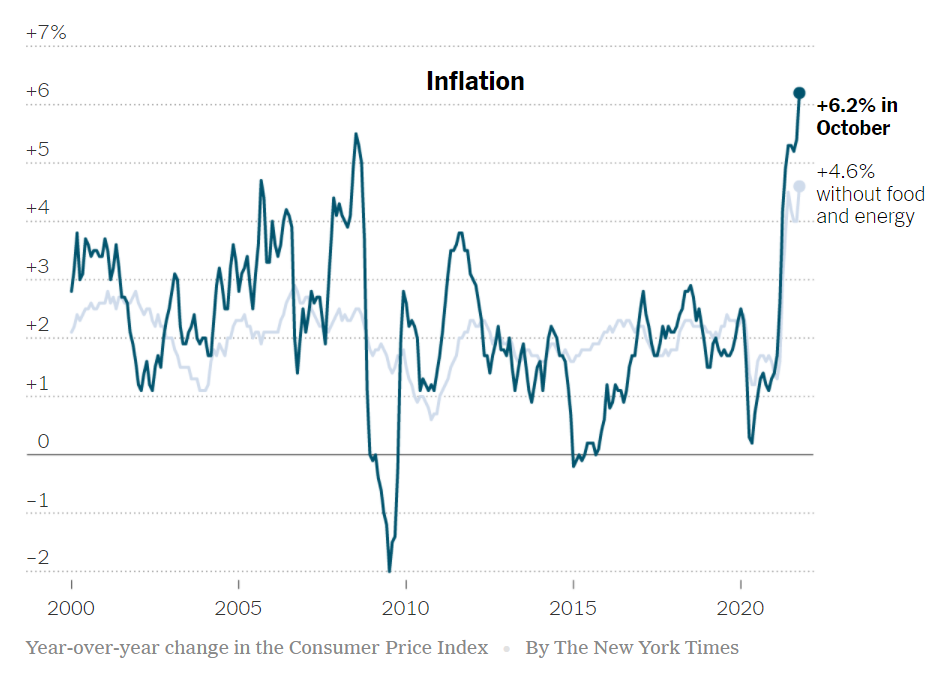

Inflation has long been the most widely used economic term. This is substantiated by searching key words across various news outlets. Today, inflation is especially front of mind as the Consumer Price Index (CPI) rose 6.2% in October, its highest increase in 31 years. Milton Friedman famously said, “Inflation is always and everywhere a monetary phenomenon,” but individual expectations also play a big role in how both consumers and workers react to inflation. There is a psychological aspect to inflation that influences consumer behavior and expectations. We’ve been conditioned to expect docile inflation, and now things are changing. This mental accounting on the overall price of things we consume is at least partially why recent increases in the costs of goods and services has evoked such a visceral response from consumers and business owners, not to mention the media.

First, it is important to note that inflation has been in a secular decline for most of the past 40 years. There have been areas of the economy where prices have actually declined and short periods of deflation in the overall economy. The past few decades have been disinflationary, which means the overall price level has been increasing at lower and lower levels. Factors leading to this were globalization and the increased supply of labor that came along with this, as well as technological advances that increased efficiency and productivity. In addition, immediate price discovery via handheld internet devices has helped consumers seek out the best deals. This all makes it harder for retailers to increase prices. It began with Walmart’s everyday-low-price strategy, and now Amazon is a big part of it.

Published November 10, 2021

Professor Robert Shiller of Yale University wrote a paper in 1997 entitled “Why Do People Dislike Inflation?” The conclusion is that people unanimously abhor inflation because they believe it reduces their standard of living. This runs counter to reality (and economic theory), wherein the cost of inflation is relatively small and is often accompanied by increased wages which tend to more than offset the higher nominal prices paid. This myopic attitude on behalf of individuals is a behavioral bias, which causes people to dislike both inflation and taxes, but at the same time gives very little credit for fiscal spending that provides tangible, offsetting benefits such as more jobs, better economic growth, and government services.

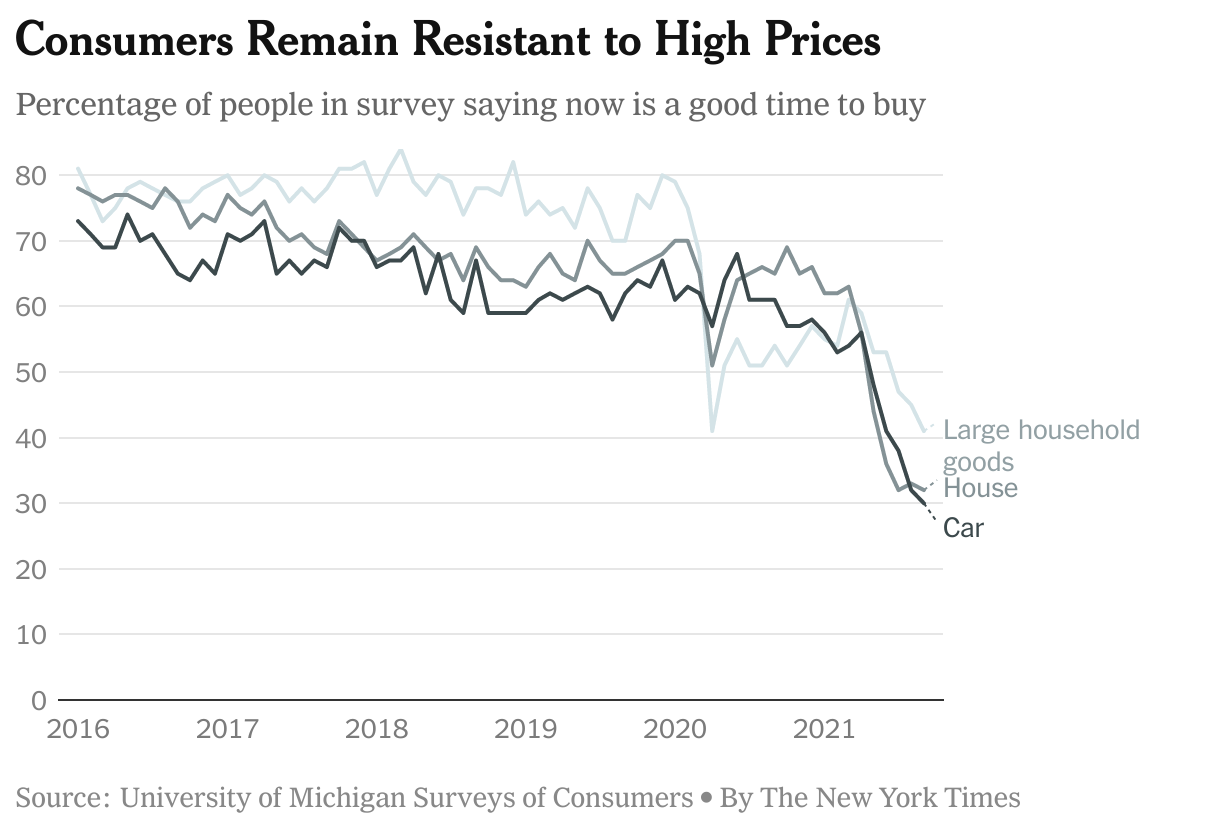

Today, prices have increased, yet the most recent University of Michigan survey indicates that most consumers imply that now is not a good time to make purchases. This is a reaction to higher prices, but if consumers felt inflationary pressures were here to stay, they would be buying now in advance of further expected price increases. This indicates that consumers must not believe that the higher prices being experienced today are likely to continue rising. It would be more worrisome if people were increasing consumption in the face of higher prices, indicating that inflationary conditions were more embedded in consumer expectations.

Published November 12, 2021

In other words, expectations that prices will continue rising should rationally lead to more consumption sooner rather than later, boosting both economic growth and short-term inflationary pressures in the process. Since we are not seeing rapid increases in consumption and because inflation expectations remain anchored at relatively low levels, it is not likely that sentiment toward price levels over the longer term will prove to be a self-reinforcing cycle of higher and higher inflation.

Wage growth is a key component of inflation and expectations. Corporations have benefitted from slow wage growth for many years. Profit margins and corporate earnings have been boosted by low real wage growth over the past few decades. Standards of living for the lowest wage earners has not risen in inflation-adjusted terms for many years. In part, this is responsible for the corporate share of GDP increasing significantly over the past 20 years. Aside from those in the lowest wage categories, many have benefitted from the trend of cheap labor. However, labor is now finally gaining some real wage increases in the aftermath of the pandemic. This is in part due to dislocations caused by the economic shutdown but may be a longer-term phenomenon. Just last month, millions of workers, many in the areas of hospitality, quit their jobs. This has exacerbated the decline in the percentage of people in the potential labor force who are seeking employment. It remains to be seen if this is a temporary condition or if attitudes toward employment have changed amongst some. It may be that the psychology of wages is a longer-term outcome of the COVID-19 pandemic and an unintended consequence of the fiscal and monetary response.

We believe that the psychology of both inflation amongst consumers and wages amongst workers will be key determinants of future inflation.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security or sector. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security or sector.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-380

Inflation Update: More Work to Be Done

Realistically, a lot of work lies ahead to get inflation under control. However, from an economic point of view, it is essential that the inflation problem be solved.

Are Bond Yields Compensating Investors for Inflation

Bourgeoning inflation anxiety has many bond investors concerned about being adequately compensated.

Inflation Update: Keep an Eye on Velocity

The inflation debate is front and center right now in the financial markets.