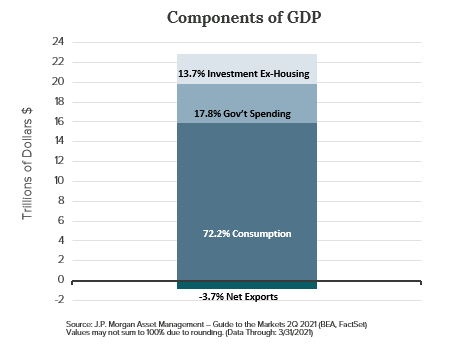

The state of the consumer is strong. In fact, at Crawford Investment Counsel (Crawford), we believe the financial condition of the U.S. consumer has rarely been better. This augurs well for future economic growth, as over 70% of Gross Domestic Product (GDP) is driven by personal consumption (consumer spending). We believe the following charts illustrate our case and underscore this positive outlook.

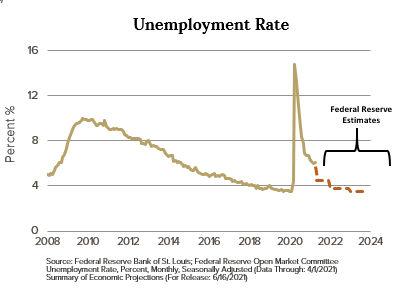

- Unemployment remains at near record low levels.

- We think post-government stimulus expirations, unemployment will continue its gradual downward drift.

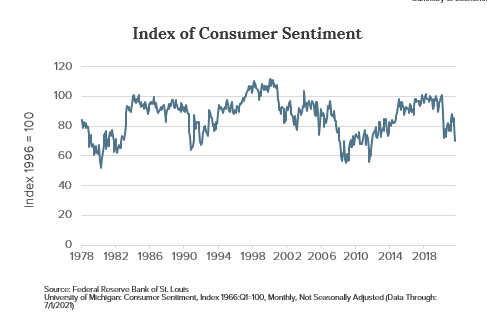

- Consumer confidence is reigniting higher, after a COVID-19 induced downward hiccup.

- Relative to the past 40 years, confidence remains high.

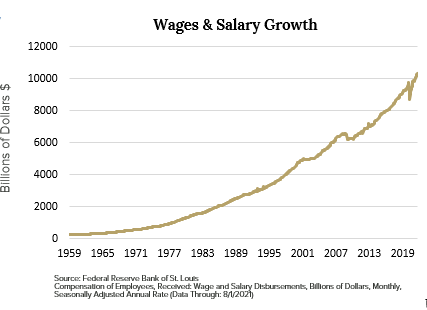

- Wages and salaries growth continue up and to the right.

- We think wage inflation is in the cards for 2022 and beyond, which may accelerate the rate of change for laborers’ wages.

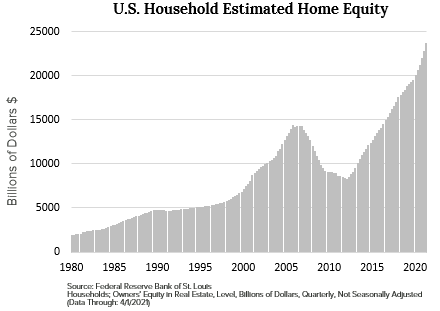

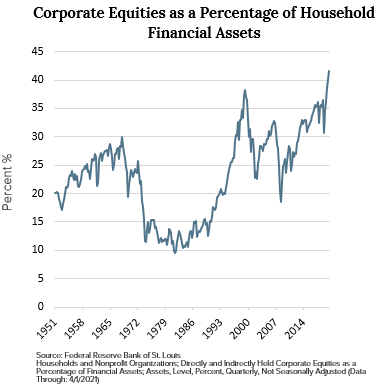

- Consumer balance sheets are at all-time highs.

- This is fueled by growing home equity and stock market participation.

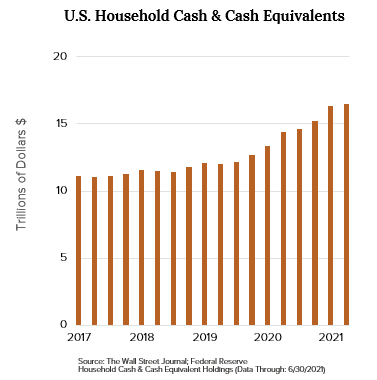

- These balance sheets are flush with cash.

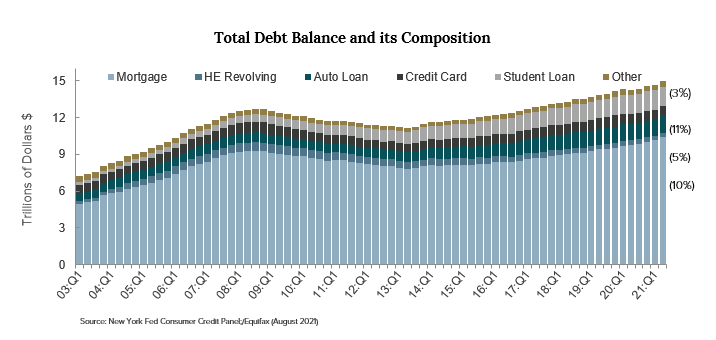

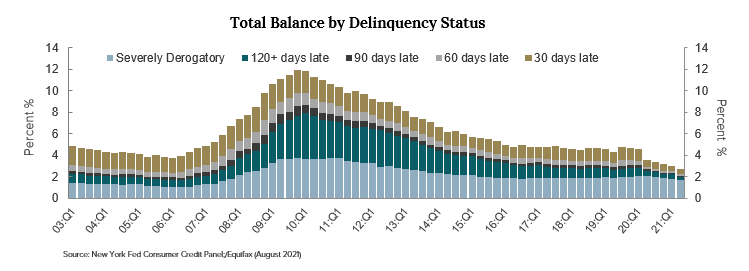

- The composition of debt is not what we find to be concerning.

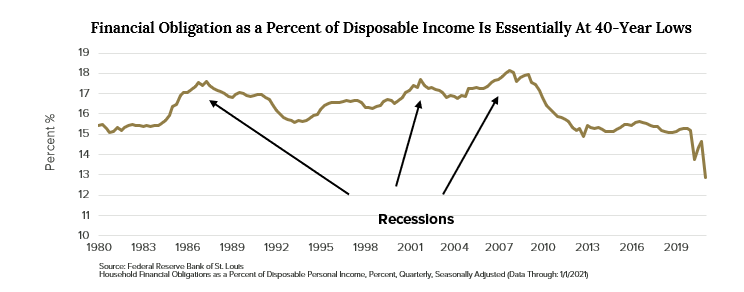

- The consumer’s ability to service debt has rarely been better, over the past 40 years.

- Is there anything to worry about?

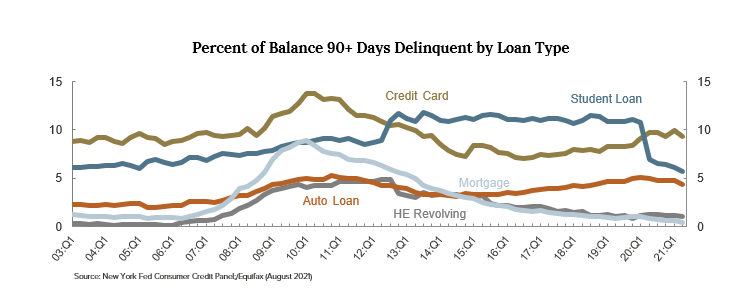

- Credit trends suggest not, although there are perhaps a few concerning developments in 90-day delinquencies for credit cards and auto loans, a pressure point about which we remain vigilant.

We believe consumer financials are as healthy as they have been in decades. At Crawford, we expect these consumer tailwinds to continue to drive healthy nominal GDP growth for several years to come. Crawford Investment Counsel’s portfolios are positioned to benefit from what we think can be a sustainable, continued, healthy increase in consumer spending. As the consumer continues to represent over 70% of U.S. GDP, we see improving nominal GDP growth driving competitive equity returns for our investors.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security or sector. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security or sector.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-370

Interview with the Core Equity Portfolio Manager

At Crawford, all of our strategies help investors achieve a specific set of goals and solve for certain needs. Clients are attracted to the Core Equity strategy because it has a higher focus on growth than other Crawford strategies.

Living with the COVID Endemic

At Crawford Investment Counsel we are constantly working to stay informed and fully abreast of developments that can have an economic impact.

Introduction to Behavioral Investing

Crawford's investment philosophy is intentionally designed to work with, rather than against, human nature.