At Crawford Investment Counsel, we invest in businesses for the long term, with an emphasis on quality. For us this begins with identifying companies that pay a consistent and growing dividend over time. We marry this orientation toward predictable and consistent, dividend-paying companies with a price sensitive approach. We believe in owning quality businesses and know that the price paid for any investment is a significant factor on the potential total return. We find that the best conditions for purchasing high-quality stocks are when short-term disruptions in a specific company’s growth trajectory drives the share price down to a point where the stock can be purchased at a discount. The combination of a declining share price and consistent or rising dividend leads to an elevated dividend yield which contributes to total return and can provide an element of downside protection. A thoughtfully constructed portfolio of undervalued, high-quality securities increases the probability of success, provides an attractive and growing stream of income, and most typically enables participation in rising markets while protecting capital in down markets. In short, we prefer to purchase high-quality stocks at attractive valuations.

Valuation is an important and final component of our expected Total Shareholder Return (TSR) framework which we use to help quantify growth and total investment return expectations for a particular stock. We seek fundamentally strong and growing companies and formally define the return algorithm as the internal growth of the business plus the dividend yield. Once we satisfy ourselves of sufficient visibility into the fundamental progress of the business, we then address the valuation component by either adding to the equation for undervalued companies or subtracting where we anticipate valuation compression. In addition, we believe the intrinsic value of any stock or investment is the present value of its cash flows. As such, we regularly run a Discounted Cash Flow (DCF) model to provide additional insight into the value of owned companies and those under consideration. The combination of our TSR and DCF models helps us identify opportunities where the stock market may be out of step with the intrinsic value of a particular business. This insistence on quality and attractive valuation provides a margin of safety as we approach the investment equation.

A corroborative approach when considering valuation is to use a variety of sector-specific multiples (e.g., P/E or EV/EBITDA) to observe a stock’s valuation as well as its relationship to the market and its peers over time. By examining current multiples today compared to historical relationships, we can attain additional insight into what the stock market is saying about a company’s future. And, a stock’s multiple is a cumulative reflection of the market’s perception and sentiment regarding a company’s durability of cash flows, in addition to an embedded expectation of a company’s growth rate, its margins, and its returns. Perceived changes or risks regarding these factors can cause a stock multiple to rise or fall.

Since we start with more consistent and predictable companies, we believe our likelihood of success is enhanced, while the potential for fundamental deterioration is more limited. These aspects of our approach tend to narrow the range of investment outcomes and provide more visibility into the success factors we expect to come to fruition. Undue investor optimism or pessimism regarding a company’s future prospects is often a result of extrapolating current, shorter-term circumstances well into the future. This myopic behavior can result in near-term dislocation and cause a stock to be temporarily over or under-valued relative to its intrinsic value. Similarly, it is possible that a stock valuation appears too high or too low because the market has a consensus view of near-term earnings expectations. Therein lies some of the artistry in fundamental analysis. Our job is to assess the company’s long-term prospects and determine where we believe the market is being overly optimistic or pessimistic. The aforementioned tools and conventions referenced are some of what we utilize to help make investment decisions.

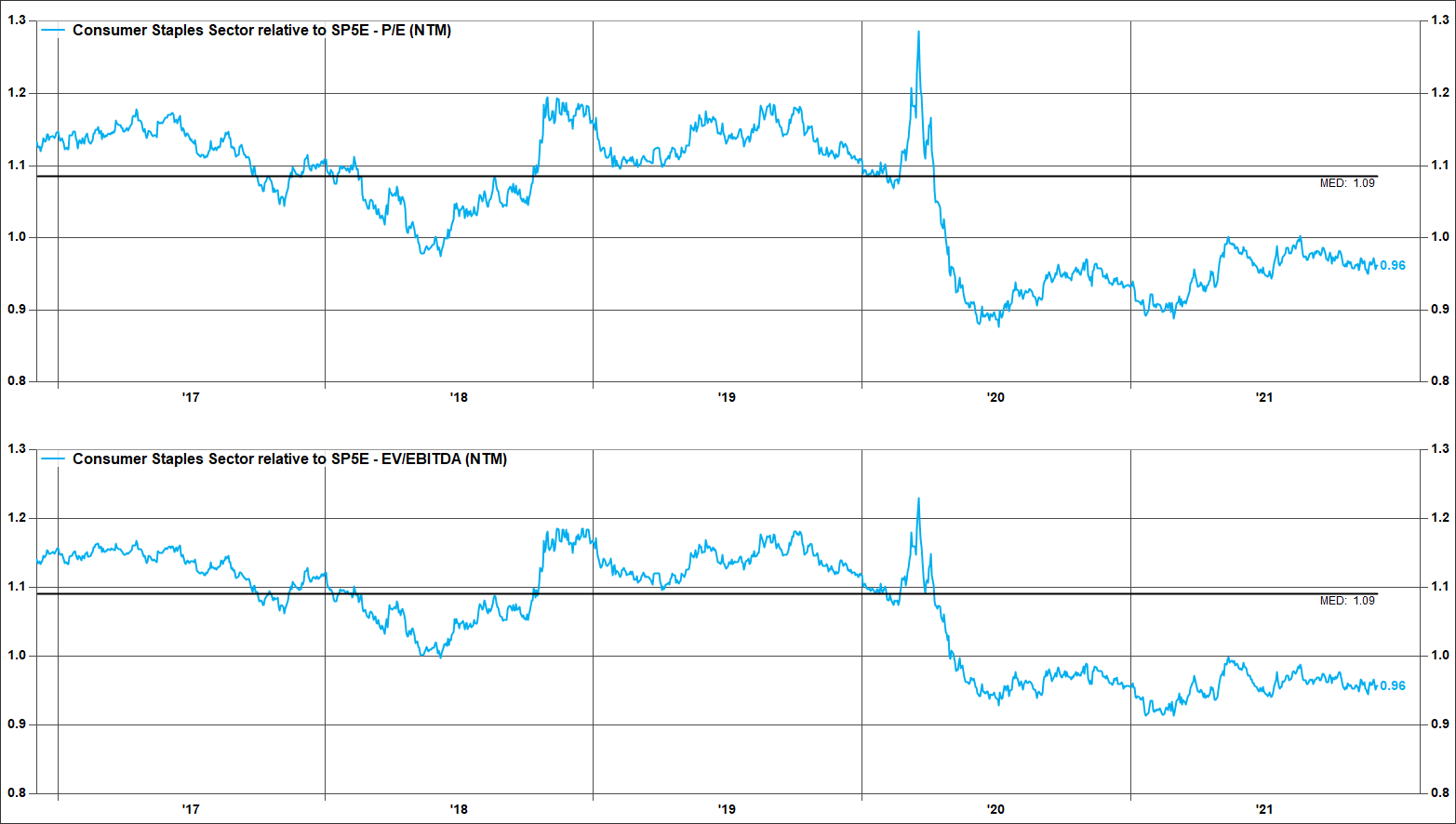

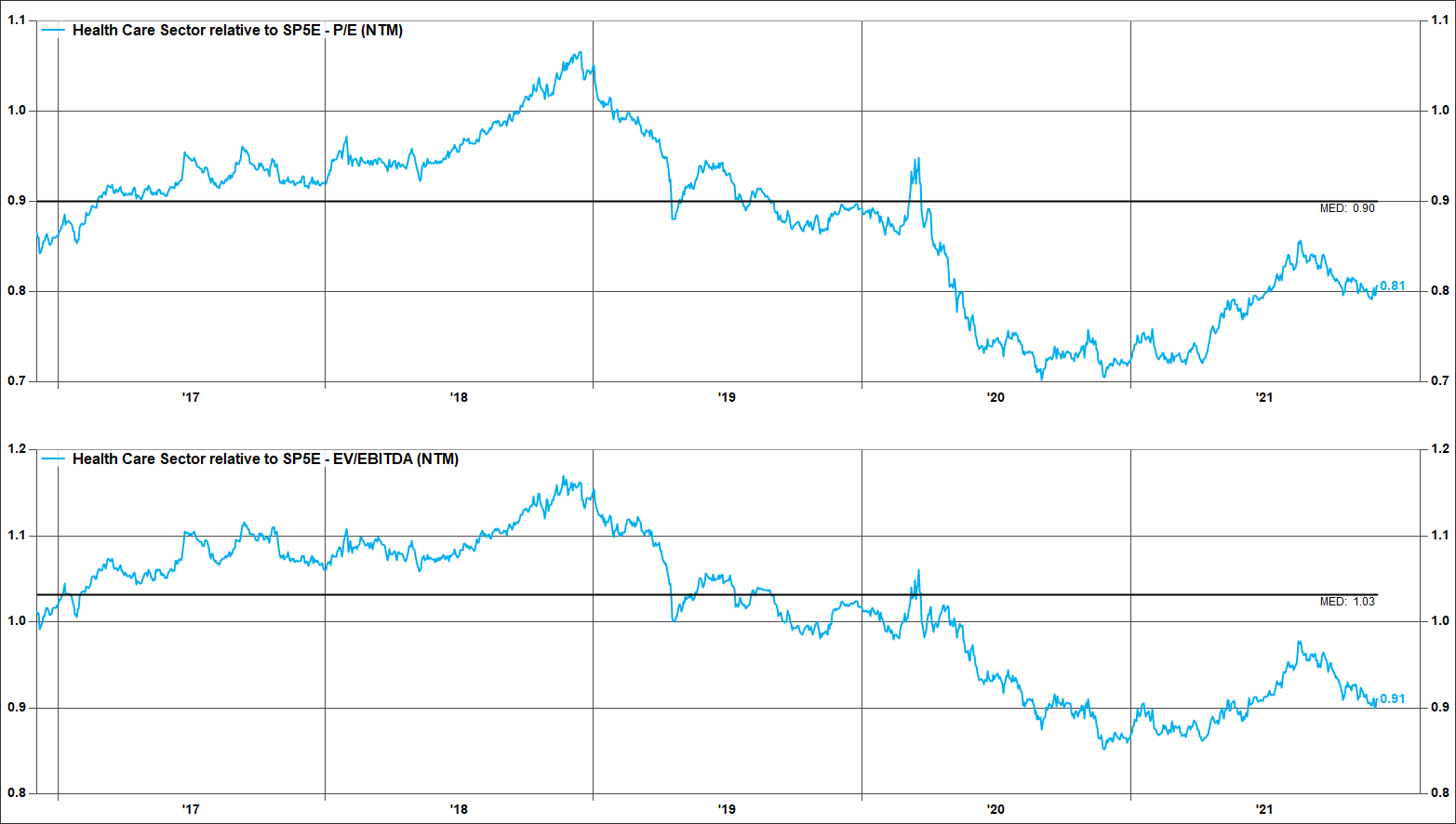

Another tool we utilize is the relative valuation chart. The charts help us compare investment opportunities within the market. We find this context/comparison works particularly well with more consistent companies, especially many of those within the Consumer Staples and Health Care sectors. The constant demand for many of the products these companies sell provides a higher level of earnings consistency. Potential or perceived changes in a company’s (absolute and relative) growth rates, margin, and returns can result in changes in its discount rate and valuation multiple. Similar factors which may impact those variables are likely to influence and impact the sector overall. If and when concerns leading to price declines dissipate, a stock’s valuation can improve, resulting in a profitable phenomenon that value investors refer to as ‘reversion to the mean.’ This additional aspect to the TSR can reveal strong total return opportunities.

In the current market environment, cyclical stocks are being favored as investors anticipate a full re-opening of the economy – both domestically and globally. These more economically sensitive businesses have higher leverage to an improving economy. Conversely, the market is attaching relatively low expectations for the more stable sectors such as Consumer Staples and Health Care. Historically, these more consistent sectors most often trade at a market multiple or at a premium to the market. This is in contrast to today where they are at a discount to the overall market. While we believe this economic optimism is appropriate at this time, we also believe the more stable sectors have attractive fundamentals which are being overlooked, and which should contribute to strong total shareholder returns over time. While it is often the case that cyclical stocks are favored early in an economic recovery, we believe economic cycle growth eventually will peak/slow, and in advance of this, the more stable sector valuations will be rewarded appropriately.

The charts below illustrate the relative valuations of the Consumer Staples and Health Care sectors compared to the S&P 500. These are both higher-quality sectors that demonstrate lower earnings variability and high ROE, and the companies in these sectors generally have strong balance sheets. Relative to the past five years, these stocks are cheap compared to the overall market opportunity set, and so we find the combination of value and quality appealing at this time.

Source: FactSet

To be clear, we do not make investments based on sector valuations, but this type of analysis can help inform where more opportunities may reside within the market at any given time. At a more granular level, we can (and do) perform this comparison for individual stocks. Returning to our TSR framework, we can apply those comparisons to inform the expected valuation contribution. Stocks can appear cheap for a reason, however, so we employ our fundamental research to perform the detailed, bottom-up analysis on individual companies to ensure there can be forward fundamental progress, a necessary ingredient for shareholder value to be realized.

Over the very short term, changes in valuation represent most of the variability of stock prices. Longer-term, both the fundamental progress of the business and dividends received have a much bigger influence on any investor’s experience. This reinforces the importance of the quality-first and valuation-sensitive approach we bring to the investment process. Suffice it to say that it is critical to get right both the fundamental business improvement and the valuation parts of the investment equation.

Given that we are long-term investors, we fully appreciate the virtue of taking a value-oriented approach to the investment equation. Marrying this with our requirement of companies that demonstrate fundamental progress gives us the confidence to exercise patience and conviction, enabling time to work to our benefit. While those with shorter time horizons cannot afford to risk being early, we can remain focused on the longer-term outlook and take advantage of ‘time arbitrage.’ We seek to strike a balance between being patient and identification of a thesis which is coming to fruition, knowing it can be well worth the wait for the fundamentals to improve. In the meantime, we are being paid a dividend while we wait.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

The opinions expressed are those of Crawford Investment Counsel Inc. Investment Team and are subject to change without notice. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Crawford Investment Counsel Inc. reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no guarantee that Crawford Investment Counsel Inc.’s assessment of investments will be correct. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not take into account specific client investment objectives.

CRA-21-391

Bursting the Bubble: Speculative Fervor Then & Now

Long-term success comes from staying disciplined, avoiding speculative frenzies, and focusing on remaining invested in high-quality investments that can weather the test of time.

Example of Investment Thesis: AstraZeneca

In the first installment of the Company Fundamental Investment Series, Senior Research Analyst and Director of Core Equity Strategy, Frank Pinkerton, walks us through an investments thesis.

The U.S. Remains a City on a Hill

U.S. exceptionalism, whether thought of in its broader original context, or the more restrictive financial and economic context, is essential to the future well being of our country.