At Crawford Investment Counsel, we seek to invest in higher-quality, consistent companies that produce more predictable earnings and dividends. Investing is about the future, which is uncertain, so we seek to improve our chances of success by focusing on companies that display fairly constant demand for their products and services. This tends to eliminate many highly cyclical or overly economically sensitive companies whose businesses may be more volatile in nature.

We have found that some of the companies within the Industrials sector offer us moderate economic sensitivity and exposure to attractive end markets with barriers to entry and sound profitability, not to mention high market shares, all of which lead to high visibility and above-average quality. As you might expect, the fundamental characteristics of this sector align well with our orientation toward the dividend as an initial indicator of quality.

The Industrials sector, also known as Capital Goods, represents one of the broadest economic sectors. Within this area of the economy are industries such as aerospace and defense, construction, engineering and building products, and electrical equipment and machinery, among others. And many companies within this sector have multiple business lines that are in some way related to business equipment or infrastructure, including services or logistics-related segments that often cross industry classifications.

From an investment standpoint, we seek to emphasize the following investment characteristics in our industrial stock selections:

- Market leaders in rational oligopoly industries.

- Attractive revenue growth and stability (above-GDP demand typically driven by recurring services or replacement parts), high profitability, and “through the cycle” cash flow generation.

- Good management teams comprised of strong operators who return significant capital to shareholders and pursue prudent M&A, all while maintaining a strong balance sheet.

- Reasonable valuations. For this sector, we favor cash-flow-based metrics (as opposed to P/E ratio).

- Quality bias reflected in strong capital allocation policies, including dividends.

From this set of fundamental characteristics, we individually research and analyze companies across the sector to arrive at our highest conviction investment ideas overall while maintaining judicious diversification to mitigate risk. From this process, our holdings currently coalesce around several leading investment themes that we find attractive. These are each expected to play out over a multi-year period, and are outlined below:

- Theme: Electrification/Utility Grid. Drivers: Energy efficiency, industrial automation, grid resiliency, renewables adoption.

Source: Slide from Eaton (ETN) Investor Day Conference, 3/1/21

- Theme: Non-Residential Buildings. Drivers: Revolutionary retrofit activity aimed at decarbonization and occupant safety (air quality, security & monitoring), EV charging.

Source: Slide from Johnson Controls (JCI) Earnings Conference, 4/30/21

- Theme: Aerospace & Defense. Drivers: Economic reopening, Asia middle class, space exploration, defense modernization.

Source: Eaton (ETN) Investor Day Conference, 3/1/21

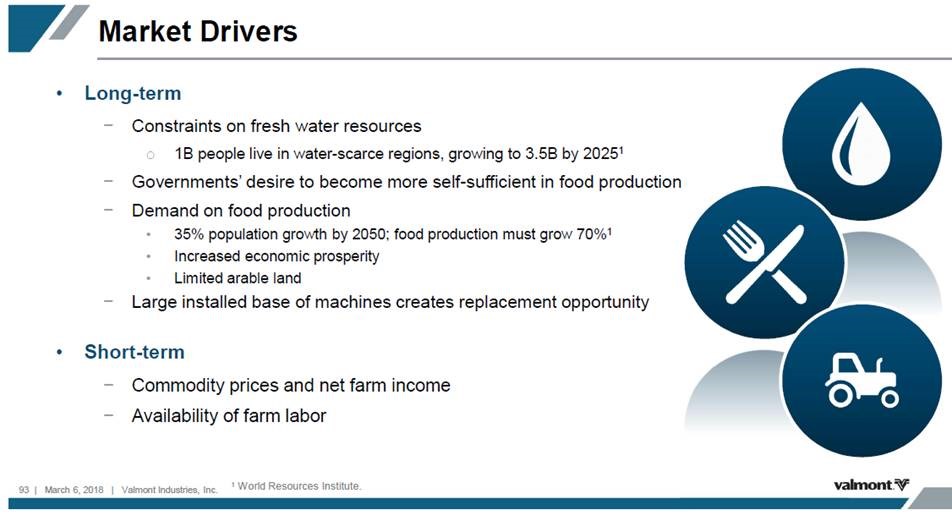

- Theme: Water Scarcity and Treatment. Drivers: Climate change, aging infrastructure, connected farms, food security, pollution.

Source: Muller Water (MWA) Presentation at Gabelli Pump, Valve, & Water Systems Symposium, 2/25/21

Source: Valmont Industries (VMI) Investor Day Conference, 3/6.18

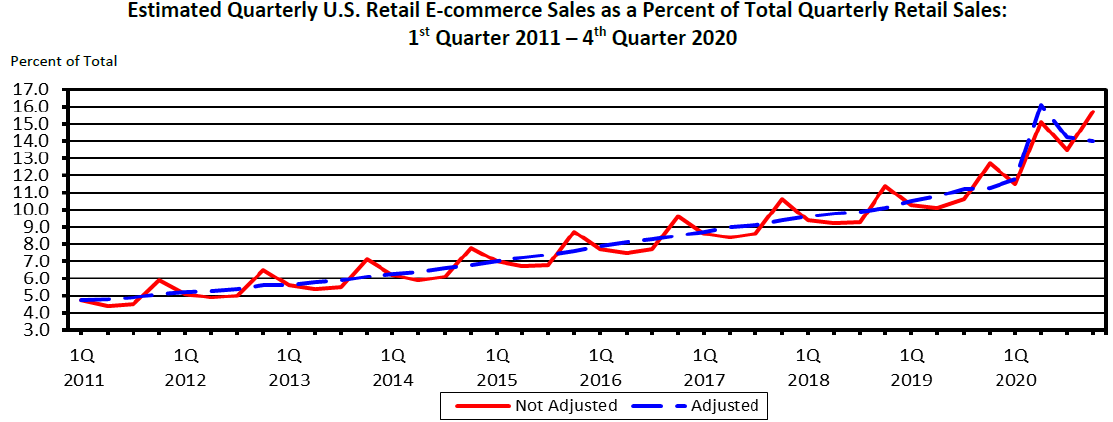

- Theme: Drivers: Retail share shift online, rise of next day delivery expectations, significant package carrier pricing power, improved delivery network efficiency.

Source: Census Bureau, Chart of the week 9/18/2020

In addition to these specific drivers of demand, we are encouraged by a combination of positive, bigger-picture tailwinds for both Industrials and the overall economy, leading to a favorable growth outlook with attractive investment characteristics. Some of them are:

- What is expected to be a multi-year economic reacceleration process is underway, reinforced by more focus on infrastructure stimulus and likely elongated by ongoing supply chain constraints.

- Good leverage to improved business conditions and the ability to pass along potential cost increases to maintain profit margins.

- Counter cyclical cash flow generation that has left many companies in this sector with improved balance sheet strength and flexibility, even relative to the pre-pandemic period.

- A robust and improving outlook for sales, profits, and earnings per share.

- Dividend yields that are largely above sector and market.

- A commitment to dividend growth, with many companies exhibiting multi-decade payment histories characterized by consistent advances.

- Valuations at a discount to the overall market based on EV/EBITDA (a preferred valuation metric for this sector that incorporates both balance sheet strength and elements of cash flow).

- Strong likelihood of further dividend increases, share repurchases, and balance sheet fortification.

Of course, investing is not without risks, and today the stock market has fairly high expectations built into share prices. For this reason, we liken our value orientation toward more reasonably priced businesses combined with a lower earnings variability factor, which means that expectations are more reasonable and, in our estimation, more likely to be met or exceeded. Once this economic cycle moderates a bit, we expect many investors will migrate toward the higher-quality industrial companies owned across CIC portfolios.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed.

CRA-21-139

Quintessential Quality

While there are examples of high-quality companies across the market, few sectors are so densely populated with quality as the Consumer Staples sector.

Expect the Unexpected

At Crawford, our strategies are engineered to embrace the reality of uncertainty. We prefer to pursue an active management process that seeks diversification across sectors, industries, and position sizes.

Not Diversification, Dividendification!

We seek diversification by investing across various areas and sectors of the market, and we insist on dividendification in the name of achieving successful outcomes for our clients.