The inflation debate is front and center right now in the financial markets. After 40 years of declining and stable inflation, participants are now taking varied points of view on the future. The conventional argument is the Federal Reserve’s “transitory” position, that is, that the sudden uptick in inflation we are now experiencing is due to base comparisons and will smooth out as the economy regains balance after reopening. The more extreme view is that somehow the supply/demand relationship has been substantially altered and that we are embarking on a period of high and sustained inflation. The truth may lie somewhere in between, but for now we concur with the conventional position as the one more likely to prevail. For a more comprehensive view of the overall inflation discussion we refer you to our piece on the website “Inflation Worries: Real or Imagined?”

There is one piece of the inflation puzzle that is getting less attention than it deserves: the velocity of money. Many observers are focusing on the rapid growth in the overall money supply as a result of the Federal Reserve’s expansionary policies. Not only have they reduced short-term interest rates to zero, they are also engaging in quantitative easing through the purchase of longer-term debt securities. The result has been a rapid increase in the nation’s money supply. This is alarming to many, recalling Milton Friedman’s famous quote, “Inflation is always and everywhere a monetary phenomenon.” We will not take issue with an economist of Friedman’s stature, but there are mitigating circumstance that should be considered.

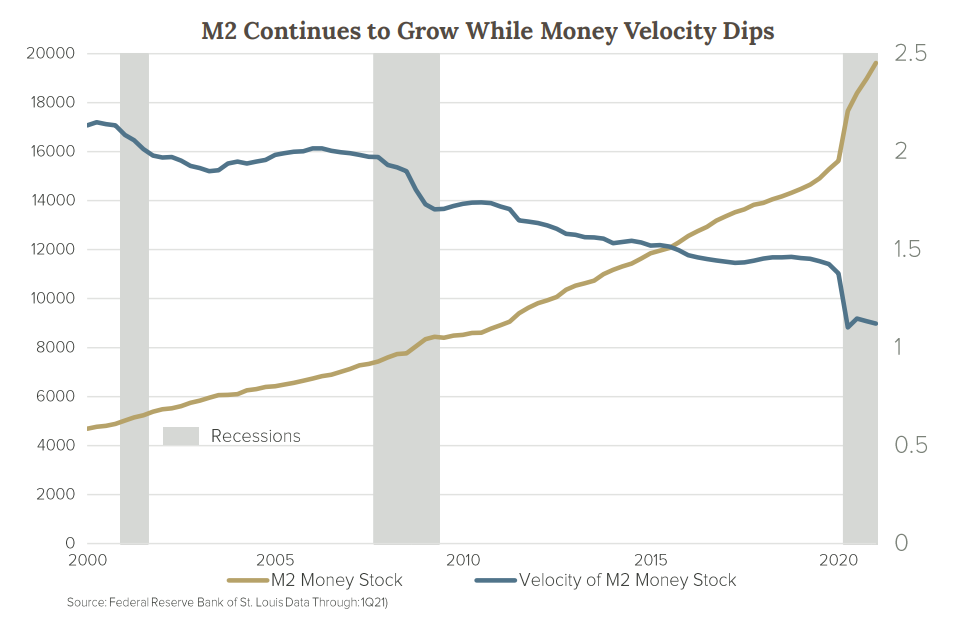

We would frame the question thusly: what difference does it make if vast amounts of money are floating around in the economy if it is not being used to create economic activity? In economic terms, some money sitting idle is no different than vast amounts of money sitting idle. Velocity of money is the means of measuring how active the money supply is. As such, it is a gauge of economic health, and higher velocity is usually an indicator of more robust economic activity. The term “money supply” typically refers to M2 that includes pure cash, cash equivalents such as money market funds, and short-term deposits. The problem is, the velocity of all this money has been in steady decline for the last 20 years. The downward trend accelerated sharply in 2020 as the pandemic locked consumers and businesses in place. Money in the economy piled up because of Federal Reserve action and expansionary fiscal policy. People simply could not spend, or chose not to out of fear of the future. See below the diverse trends in money supply and velocity.

The precipitous decline in velocity in 2020 can be attributed to unusual circumstances and is likely to be at least partially reversed as the economy fully reopens this year. That is because volatility is computed by multiplying nominal Gross Domestic Product (GDP) by the money supply, and both factors are expanding. However, the longer, downward trend which started in 2000 may be more difficult to reverse. A closer look at the chart indicates velocity had its most severe declines during and after the last three recessions: 2001, 2008, and 2020. It will be recalled that interest rates were declining throughout this period, but most severely after the 2008 recession when rates went to zero and have remained there for most of the time since. This suggests that the level of interest rates play a role in velocity.

Prior to 2007 federal funds were 5% and other interest rates were even higher. If a company or individual held money at that time, there was an expense attached to it since there were other alternatives that would provide an attractive rate of return. But when rates went to zero and there were no higher-yielding alternatives, there was no penalty for holding money. It has become easy just to hold money, and it sits idle. Thinking further, the suggestion would be that a return to higher interest rates would likely spur an increase in velocity. Perhaps, but one has to assume a much higher level of interest rates, something we do not expect. In our view, there is a linear connection here: low interest rates cause idle money, thus lower velocity of money, and limited impact on inflation.

The last point is the important one. There may be a connection between velocity and economic activity, but the connection of money supply and inflation is tenuous. It takes more than a lot of money supply to create an inflation—that money has to be active. No matter the size, money, sitting idle or moving slowly, is not likely to generate enough economic activity to create severe inflation pressures. This is why it is important to keep an eye on velocity. If it remains low by historical standards, it is not likely to presage an inflation cycle, but should it reverse its long decline in a meaningful way it would be cause for concern, given the swollen money supply. On this score, we will be watching velocity for clues to the future of inflation.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-148

Green and Growing Income

The consistency found within utilities is a function of the fact that it is a regulated industry that enjoys fairly constant and growing demand.

Example of Investment Thesis: AstraZeneca

In the first installment of the Company Fundamental Investment Series, Senior Research Analyst and Director of Core Equity Strategy, Frank Pinkerton, walks us through an investments thesis.

Is Your Portfolio Ready for Winter?

Currently, there is a dramatic shift occurring in the global financial markets. Unlike a fantasy novel, it is not as definitive as the first snowfall.