As we recognize the 10th anniversary of our Dividend Yield strategy becoming a formal investment portfolio at Crawford Investment Counsel, we wanted to take both a look back and a look ahead. Throughout the 40-year history of the firm, we have accommodated clients seeking a higher level of income or enhanced dividend yield. Initially, this was accomplished on a portfolio-by-portfolio basis by modifying allocations or changing position sizes in an effort to meet client income needs without sacrificing return or increasing risk. In 2010, this practice of offering investors a distinct strategy with a higher level of income was formalized into a separate strategy under the name Crawford Dividend Yield.

Ten years ago was a notable period for both equity and fixed income investors in that it was the first time since the 1960s when the stock market dividend yield was higher than yields on government bonds. The long rise in interest rates in the 1970s was followed by a subsequent 40-year decline, which has been punctuated by the central banks’ low/zero interest rate policies in the aftermath of both the global financial crisis and now the pandemic. The period following The Great Recession was one where numerous companies, especially financial institutions, had to cut their dividends due to economic conditions, many unable to restore them for years. It is no coincidence that the Dividend Yield strategy emerged out of this environment. Our firm’s capability of delivering a high level of sustainable and growing dividend income, in contrast to the lowest interest rates seen in a generation, made the strategy a compelling and timely offering. In the current period (2020 and 2021), we again are witnessing both low interest rates and record dividend cuts and suspensions resulting from the economic shutdown in response to the Covid-19 pandemic. Therefore, we believe the rationale for the strategy remains highly relevant today.

Source: Crawford, Factset

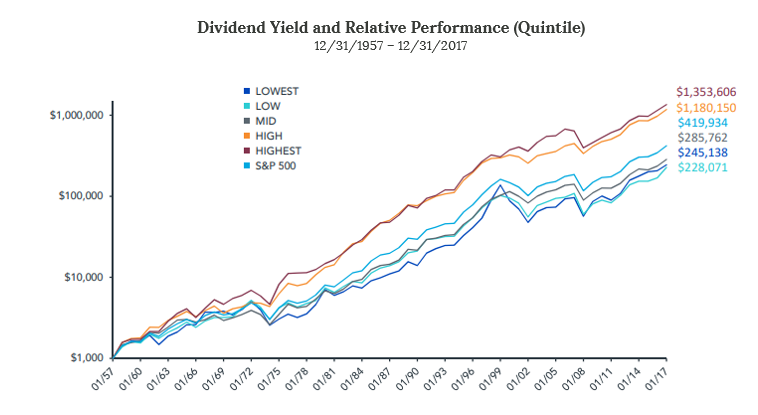

While the strategy does satisfy an investor need in a low-interest-rate world, there is strong empirical evidence and historical precedent documented by numerous academic studies that undergird the merits of investing in higher yielding stocks. Most notably, these studies include research by famed value investor, David Dreman, as well as the now infamous Lehman Brothers. One of the more prominent and expansive studies is by University of Pennsylvania Professor of Finance, Jeremy Siegel. Dr. Siegel’s original research was published in his 2005 book, Future for Investors, with data subsequently updated through 2017. Looking back at 60 years of stock market performance, his findings revealed that stocks in the top two highest dividend yield quintiles provided greater total investment return as compared to the overall market (S&P 500 Index) and did so with less risk (as measured by stock beta).

Source: Wisdom Tree: Siegel, Future for Investors. 2005, with updates to 2017. Period 12/31/1957-12/31/2017.

We embrace these studies and have witnessed firsthand the compelling risk/return tradeoff that higher-yielding stocks can provide. This area of the market can be a fertile universe for both current income and total return. As such, we target a yield that falls in the 8th and 9th (highest) decile yields in the market for the Crawford Dividend Yield strategy. Our rationale for this is to position the strategy within a universe of stocks that best enable it to provide high income and strong performance as suggested by the academic research. At the same time, targeting a decile range that varies over time relative to the overall market helps ensure we are not held captive to a static nominal yield threshold which may result in over-reaching/stretching for yield in a low-interest-rate environment. Further, it should be noted that with the exception of select investments which may reside in the 10th yield decile due to their unique business model and naturally high payout ratio, we generally deemphasize this highest decile as many of those stocks are of lower quality, suggest potential financial stress, and carry a higher probability of a dividend cut.

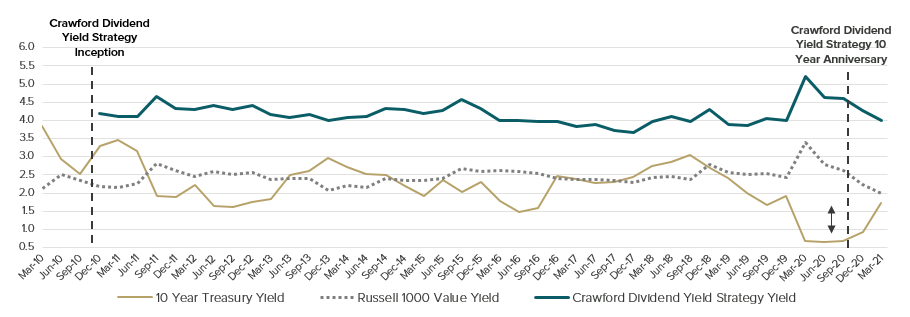

The yield on our strategy has consistently oscillated around 4%, and as of the end of the first quarter of 2021, its yield was approximately 4.01%. This yield was over twice as high as our primary benchmark, the Russell 1000 Value Index, and significantly above the S&P 500 Index. We believe it is among the higher-yielding, actively managed equity portfolios available today.

While the strategy’s primary emphasis is on current yield, Crawford’s bias for high-quality stocks is clearly reflected in our portfolio selections. We seek companies that offer both current income as well as growth in income over time. Many companies that are core to the higher-yield deciles and our strategy tend to be more mature and, as a result, have higher payouts due to fewer growth opportunities. At the same time, many of these companies are high-return businesses with low capital requirements, enabling sustained, higher payouts. Since our strategy’s inception, we have looked to bolster those core portfolio positions with higher-quality stocks that offer better growth and diversification of income across sectors. Often, stocks in non-traditional ‘yield’ sectors that reside in the higher deciles have higher yields and lower valuation due to underperformance. These situations can provide strong total return opportunities from ‘reversion to the mean’ or revaluation if, and as, the concerns leading to price decline dissipate.

Earning the 4% dividend is a good start to providing a solid total investment return over time. But for us it is just a start. When considering the familiar Gordon growth equation [Price = D1 /(r-g)] one can see that the value of a stock over time is driven by three factors: next year’s dividend amount, a required rate of return, and the perpetual growth rate of the dividend. Of those factors, the growth of the dividend has by far the largest impact on the value of the investment. We think adding both quality/growth and diversification of income can help mitigate the interest rate risk and stigma of bond surrogate status, limiting this potential influence in the process.

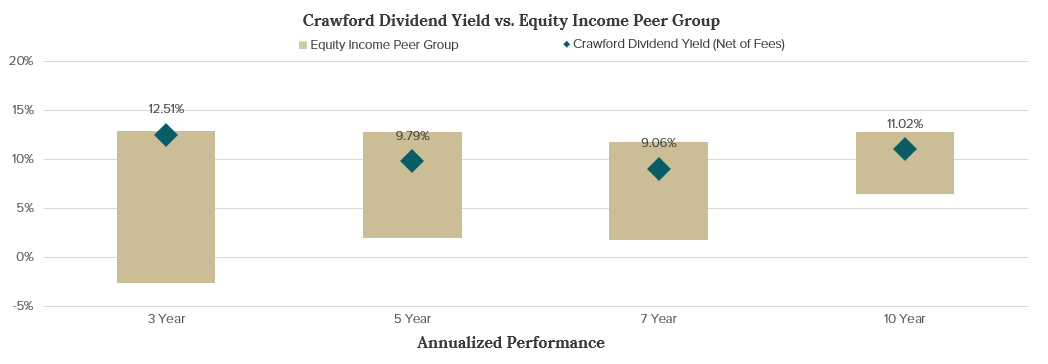

In general, we have been pleased with the performance of the Dividend Yield strategy over the past one, three, five, and ten years (since inception). As noted previously, the yield on the strategy has oscillated around 4% over the past decade. While there are periods when higher-yielding stocks are in or out of favor with market participants, over the long term the strategy has been competitive with its primary benchmark and has consistently met its primary objective of current income. This performance has occurred in an environment which lacked a tailwind for a higher-yielding strategy. Over the past 10 years, growth has outperformed value, non-dividend payers have been favored over dividend payers, quality has not distinguished itself, and higher yield buckets have underperformed lower yield/no yield buckets.

Data as of 3/31/2021 Source: Crawford, FactSet, eVestment. Equity Income Peer Group: Comprised of mutual funds in the Lipper Equity Income Peer Group with a % Dividend Yield >3.5%; duplicate share classes were removed. The floating bar illustrates the range between the minimum and maximum performance within the peer group. Past performance is not indicative of future results. The composite returns are shown as supplemental information to the Dividend Yield composite disclosures.

Looking ahead, we believe the opportunity for the Crawford Dividend Yield strategy is as good as we have seen since its inception. First, the yield on U.S. 10-Year Treasuries remains low by historical standards, highlighting the attractiveness of higher yielding stocks. Over the past year, the Dividend Yield strategy itself provided income that at one point was nearly five times greater than those longer-dated treasuries. While not our base case, if the economy proves more fragile, we believe the higher yield can provide some defensiveness in a market with elevated valuations. Conversely, if the economy continues to improve, there is the opportunity for a further re-rating/higher valuation of the stocks which until recently have been generally overlooked in favor of growth. Finally, as the economy normalizes, we believe secular growth will remain muted. All of these conditions, both short- and long-term, make higher-yielding stocks attractive at this time, in our view.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

The composite returns are shown as supplemental information to the Dividend Yield composite disclosures regularly distributed by the firm. If you have not received a copy of Crawford’s GIPS composite reports, please contact Casey Krimmel Dhande at Crawford Investment Counsel, 600 Galleria Parkway, Suite 1650, Atlanta, GA 30339.

CRA-21-143

Looking Back and Looking Ahead

Since we find ourselves at the beginning of a new year, let’s take a broad look back at what we have seen transpire over the past 12 months.

Gauging an Outlook for the Stock Market

Attempting to estimate stock market returns is difficult, but looking at things through a longer-term lens improves our chances of success.

Book Review: The Number

Looking to better understand the ramifications of living off of an investment portfolio in retirement? Let us recommend a good book!