Have you ever worried about too much government debt? Will the government ever have a balanced budget again, much less pay down its debt? Will the U.S. Government ever run out of money? Are deficits always and everywhere inflationary? If these are concerns of yours or if you seek perspective on these and other issues related to budget deficits, we recommend reading The Deficit Myth by Stephanie Kelton. You may not always agree with her on monetary and fiscal policy, but if you read this book, you may have a better understanding of how our system of money functions. Exploring these issues is especially timely since very large deficits have been produced in the last year through pandemic relief and aid. Furthermore, the Biden administration is proposing additional large spending programs that will have deficit effects. The deficit discussion is certainly pertinent at this time.

Right now, Kelton is the face of a school of economic thought called Modern Monetary Theory (“MMT”). MMT is by no means standard or mainstream economic theory and is derided by some academics as totally unrealistic and dangerous. In the book, she advocates for MMT on the grounds that it can dispel myths about how our money system works and thus can free up policymakers to move us toward a more productive and people-focused economy. That is about all we wish to say about MMT itself, for our purpose is not to make a judgment on the merits of MMT but to review some of the myths that exist around budget deficits and public spending. On those grounds we endorse her book as helpful and interesting.

This is not a typical economics book. It made the New York Times’ best seller list. It contains only a few charts and no equations, and it is written in plain English. Kelton has a unique ability to reduce abstract and complicated issues to simple and understandable terms. It will not require an economics degree to understand the book.

There are several themes that Kelton returns to as she exposes popular myths. One is the comparison of household budgets to government budgets. The myth is that since a household must balance its budget, governments must do so also. Not true. Unlike a household, the federal government just issues the currency it spends; the head of household must earn the money to balance his/her budget. Suppose the government buys a tank from a defense company. When the tank is delivered the company bills the government, and on a keyboard at the Federal Reserve the account of the company is paid up. It is that simple, and it can be done for any amount of money that is authorized by the Congress because the U.S. has its own currency which allows it to produce an unlimited amount of dollars. As the Federal Reserve of St. Louis put it, “the U.S. Government is the sole manufacturer of dollars.” And in the same vein, Allen Greenspan, Chair of the Federal Reserve at the time, in testimony to Congress, said, “There’s nothing to prevent the federal government from creating as much money as it wants and paying it to someone.” This differs completely from the household budgeting process where expenditures have to be met with a limited amount of resources. Yes, a household has to balance its budget, but the U.S. Government does not.

Similar to the idea of our government having unlimited ability to create dollars is the myth that the government has to have money in hand before spending. Here Kelton differentiates between spending before taxing and borrowing (S(TAB)) versus taxing and borrowing before spending TAB(S)). Have you ever heard a congressman say we can’t afford to do something because we would have to raise taxes to pay for it? Again, untrue. The government routinely spends first (S(TAB)) and may later raise taxes or borrow to pay for it, although not necessarily so. But again, the government is free to go ahead and spend whenever it is authorized by Congress. How the money is raised is irrelevant and may never happen.

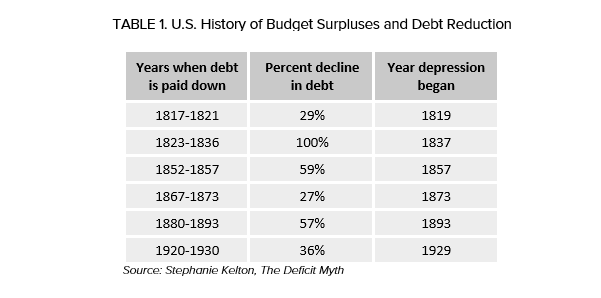

Deficits have a bad name, and the implication is that they are always bad. Kelton dispels this myth by suggesting that deficits should be thought of as a means by which the government injects money into the economy and that by running a deficit the government is taking less money out in taxes. When necessary, the government takes money out of the economy by raising taxes in order to narrow deficits. While budget-makers often long for the days of balanced budgets, they are dealing in fantasy, for the U.S. Government almost always runs a deficit. In truth, deficits are the norm, as illustrated by the fact that the U.S. Government has not balanced its budget in 20 years. On this point Kelton has an interesting table that we reproduce below. It makes the case that going from deficits to balanced budgets on a sustained basis can be very detrimental and may result in recessions or depressions.

Kelton definitely does not make the case that deficits are always good. Instead, she makes the point that deficits can serve economic purposes, and as the table above suggests, when deficits are dramatically reduced, the consequences can be severe. The authorities would be well served to not be too aggressive in deficit reduction.

By this time Kelton may be creating the impression that unrestrained spending carries no penalty and that governments can spend unlimited amounts with no consequences. Kelton is quick to take the other side by noting that there are times when spending is overstimulating, and the way to know when this is occurring is inflation. Inflation is the ultimate brake on how much the government can inject into the economy. If resources are strained to keep up with activity and inflation begins to rise, this is when taxes should be raised to narrow the deficit and slow the economy down. One can argue that this sounds too easy since tax increases require congressional action, something politicians are loath to do. Nevertheless, it is helpful to think of deficits as injections into the economy and taxes as withdrawals from the economy.

In this review, we have highlighted a few of the myths Kelton exposes for what they are. Her conclusion is that these myths are detrimental because believers that act on them are acting on false premises, and therefore, these myths hinder proper policymaking. We believe her goal is obvious: to create clear understanding of how our system works and eliminate fear of action based on the myths. You may not agree with her goals, but if a reading of this book dispels some myths in your understanding, we believe you will be a more informed observer of the economy and government action within it.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed.

CRA-21-136

Deficits and Government Debt

For the last 20 years, the U.S. Government has been continuously running budget deficits, resulting in huge amounts of government debt being issued.

The Year of Triple Tightening

We define triple tightening as the Fed raising interest rates, the Fed’s balance sheet shrinking, and reduction in fiscal programs to recipients.

Is Your Portfolio Ready for Winter?

Currently, there is a dramatic shift occurring in the global financial markets. Unlike a fantasy novel, it is not as definitive as the first snowfall.