The stock market is a complex system. Millions of different individuals with different points of view come together to set pricing on publicly traded businesses. It can be a frustrating endeavor to try and figure things on a near term basis, as often the flow of information is overwhelming and uneven. Thus, when we view investing for our clients, we often think of Benjamin Graham’s quote:

In the short run, the market is a voting machine but in the long run it is a weighing machine.

Only a couple of other times in my investing career has this statement applied so directly to a specific group of companies – the Pharmaceutical Industry. Why? Because currently the market is voting fairly heavily against the pharmaceutical industry:

- Growth for the pharmaceutical industry comes from new patients which are often diagnosed by a physician in an office. The COVID pandemic has lowered in-office visits, and many of these diagnoses are coming later, if at all.

- The Democrats control the White House and both chambers of Congress. This has raised concerns, mostly related to government pricing controls and further regulation. On the whole, the news front has been negative.

- Patent expirations are a company-specific risk to investing, and there are a handful of companies with very large patents expiring over the next four years. When a patent expires for a large proprietary medication at a pharmaceutical company, it typically results in lower revenue and cash flows for several years until the product’s contribution can be replaced.

- Given the recent recession and burgeoning recovery, investors are following an old playbook to buy companies with economic sensitivity and the ability to raise price, leading them to de-emphasize their investments in healthcare (and specifically pharmaceutical companies) in order to benefit from the recovery.

There are many other situational negatives we could cite, but the takeaway is that investors currently dislike pharmaceutical companies. Sectors and industries often fall in and out of favor with investors, but over the long term, corporate earnings and dividends will influence share prices. On this we are confident that healthcare and pharmaceuticals will demonstrate attractive “through the cycle” growth and stability. This is why we seek to invest our clients’ portfolios with a healthy allocation to pharmaceuticals.

We believe it is evident that pharmaceutical companies add value to society and the economy, which can most recently be seen through the response to the COVID-19 pandemic with vaccines and therapies. We don’t think this trend will stop. Our preferred companies invest billions of dollars each year in finding new drugs and biologics that improve patients’ lives. For example, Merck’s last five years, and next eight years, will largely be about dominance in oncology, as Keytruda, a prescription medicine for cancer treatment, was the first to market a new type of oncology biologic that has saved hundreds of thousands of lives. Keytruda basically allows the patient’s immune system to attack cancers more effectively.

Source: Congressional Budget Office

Source: Congressional Budget Office

Additionally, advances in science and technology continue to accelerate and provide opportunities for pharmaceutical companies to bring better products to market. Approved only two years ago, cell therapies are an example of a remarkable advance in science, despite sounding like science fiction. For example, Kymriah, a Novartis therapy discovered at the University of Pennsylvania, is a process where a patient’s immune cells are harvested, engineered to fight cancer, multiplied by billions, and then re-injected into the patient. In addition to cell therapy, the areas of gene therapy, RNA interference, and mRNA vaccines also hold tremendous promise.

Lastly, we believe pharmaceutical stocks show many consistent financial tendencies that fit our customized portfolios and help our clients achieve their investing targets. While pharmaceutical companies show very consistent earnings growth, return metrics, and earnings stability, their dividend track record is close to pristine. At Crawford, we view dividends as an indicator of both quality and value, and pharmaceutical companies are among the most consistent payers and growers of dividends. For example, Johnson & Johnson has increased its dividend for 59 consecutive years. The surety of collecting dividend income and the likelihood of dividend growth to offset inflation allows our portfolio managers to meet client income goals without invading corpus.

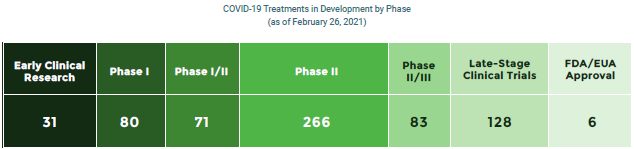

It should be noted that over the last 18 months, many pharmaceutical companies invested billions of dollars of capital to create, research, trial, and manufacture a vaccine against a virus that was previously not known. The COVID pandemic shut down our lives, causing an estimated $16 trillion in economic damage and far greater loss to life and happiness. We believe that successfully creating a vaccine that protects an individual for minimal cost illustrates the pharmaceutical industry is part of the solution for our healthcare needs as opposed to part of the problem. Meanwhile, the U.S. government supports giving away the intellectual property. Giving away intellectual property is a tremendous burden to be placed on the pharmaceutical industry, because if investors believe that intellectual property rights are not sacrosanct, future development could be hindered.

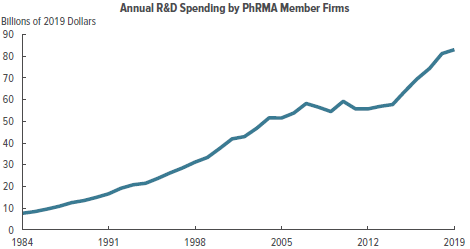

Source: PhRMA

Source: PhRMA

We continue to investigate, own and add to our favorite companies in the pharmaceutical industry despite them being out of favor. We will happily invest in companies that we believe are making tremendous headway in improving the lives of patients, with yields higher than the market, and that have long held dividend increases. We are confident that by working together, the pharmaceutical industry, governments, and other commercial organizations will realize the value this industry brings and reward pharmaceutical companies for that in the long run.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not a recommendation to buy or sell a particular security or sector.

CRA-21-135

Benefit of Working with CIC - Income and Growth of Income

Owning income-producing securities is an important and differentiating element of working with Crawford Investment Counsel.

Update: The Corporate Juggernaut Powers On

Here we introduce a different reason behind the continuing ability of corporate America to increase its share of the overall economic pie.

Dividend Integrity

It is interesting that the period of time in which this strategy was created was not entirely different from the economic and market circumstances today.