In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- We remain on recession watch, but we acknowledge the potential for a “soft-landing.”

- We continue to believe monetary policy rates are higher than they should be based on our expectation of a more balanced economic environment.

- Our Core and Municipal strategies are positioned to:

- Preserve capital with a strong bias to high quality (sector and issuer credit strength).

- Benefit from total return as rates adjust to a more balanced economic environment (yield curve positioning and maturity extension).

- Produce a high level of current portfolio income (bias to higher-yielding spread sectors and above-average coupons).

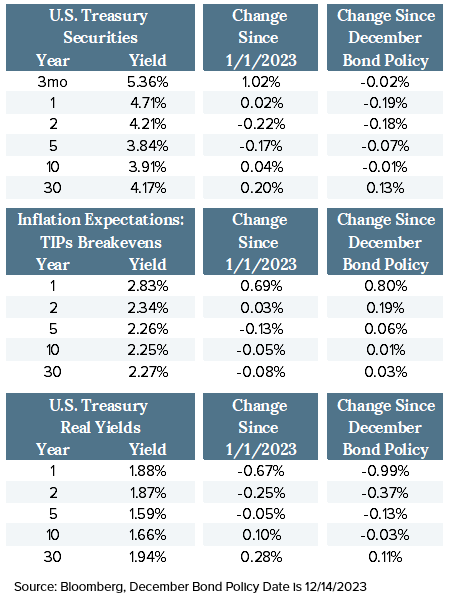

Treasury Yields as of 1/31/2024 (Post-Fed Meeting)

- Nominal Treasury yields fell across the curve since our December Bond Policy meeting, except for the 30-year bond, which moved modestly higher.

- Curve Inversion: Historically, when the secular trend in interest rates is higher, inversions last longer.

- The 3mo/10yr Treasury yield curve inversion (beginning November 2022) was unchanged. In the previous nine inversions, on average, recession began 23 months after inversion (October 2024).

- The 2yr/10 inversion (beginning July 2022) flattened by roughly 15 basis points (bps). In the previous six inversions, on average, recession began 20 months after inversion (March 2024).

- Market inflation expectations, as reflected in TIPs (Treasury Inflation Protected securities) “Breakevens,” increased modestly across the curve, except for the 1-year, which moved up 80 bps.

- Real Yields generally fell, particularly in 1-year, with the exception of the 30-year, which increased 11 bps, all in reaction to anticipated cuts in the Fed Funds rate.

- U.S. Treasury performance over the past six weeks has been driven by a combination of aggressive market discounting of future Fed rate cuts, surprisingly strong economic results, and continued evidence of declining inflation.

- The Fed Funds Futures market has consistently priced in five to six cuts of 25 bps by the end of 2024, whereas the Fed, in its December DOT Plot, estimated three cuts.

- The U.S. consumer has carried the day for economic results with unexpected strength and increased optimism.

- The speed of the decline in inflation has also contributed to bond market performance with healing supply chains, lower oil prices, increased productivity, and labor market strength all having a positive influence.

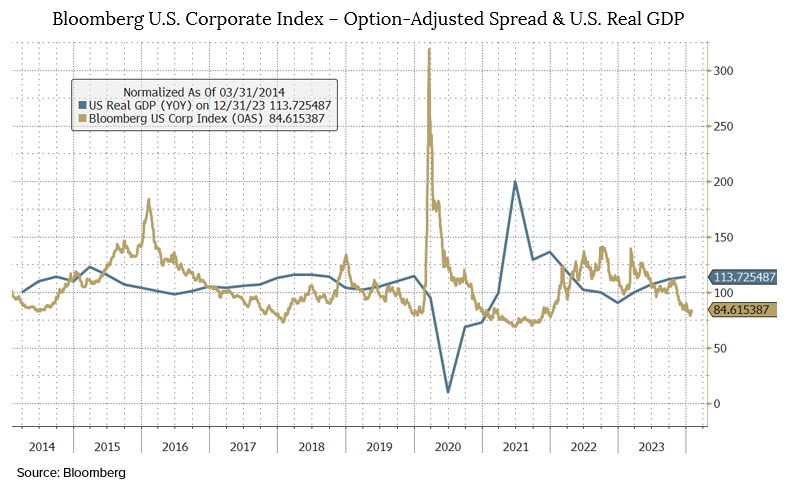

Corporate Bond Market

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- The graph below illustrates the relationship between the Bloomberg U.S. Corporate OAS Index and U.S. Real GDP. The purpose of examining their historical behavior is to attempt to observe (generically) whether yield spreads are currently at a level significantly outside of the normal range (using normalized U.S. Real GDP as a basis for comparison).

- The relationship normally exhibits falling yield spreads (compensation for risk) as GDP rises, and vice-versa. As displayed below, the Corporate index spread is currently relatively low, but not too tight based on rising GDP and historical observation.

- Investment Grade Corporate OAS tightened modestly between the December and January Fed meetings, but it is holding at a relatively tight level given the continued uncertainty regarding Fed policy timing.

- Tight yield spreads are supported by improved high-grade fundamentals which continued to improve in the third quarter of 2023 as corporate management teams pursued more conservative policies, including reduced share buybacks, increased cash balances, and lower capital expenditures growth.

- Strong technical support is also providing strength to spread levels with the month of January printing a record in high-grade issuance.

- Demand for new supply has been very strong with very little yield concession.

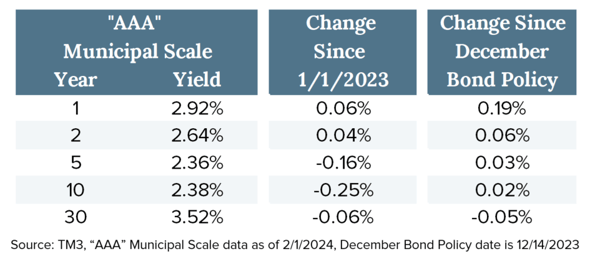

Municipal Bond Market

- Municipal Bond “AAA” scale yields were essentially unchanged since the December Fed Meeting.

- Yields fell dramatically moving into year-end, remained stable for the first two weeks of January, and then began to move back up in sympathy with the Treasury market and higher municipal supply.

- Lower quality outperformed higher-rated bonds in 2023. Year-to-date performance is even across the ratings spectrum.

- 5- and 10-year generic yields are currently below their 1/1/2023 levels.

- Relative value metrics across the curve remain very tight, but absolute yields remain attractive versus recent history.

- New issue origination is projected to be roughly 10% higher than it was in 2023 and will likely be weighted to the first half of the year given that it is an election year.

- Looking forward, municipal headwinds include:

- Rich relative valuations

- A heavier supply calendar

- Treasury market volatility as the Fed transitions policy

- Municipal tailwinds include:

- Absolute yield levels

- Credit strength

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-24-039

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.