Our Dividend Yield strategy offers a high and rising stream of dividend income to investors. This has contributed to attractive total investment return with lower risk than the strategy’s primary benchmark, the Russell 1000 Value Index.

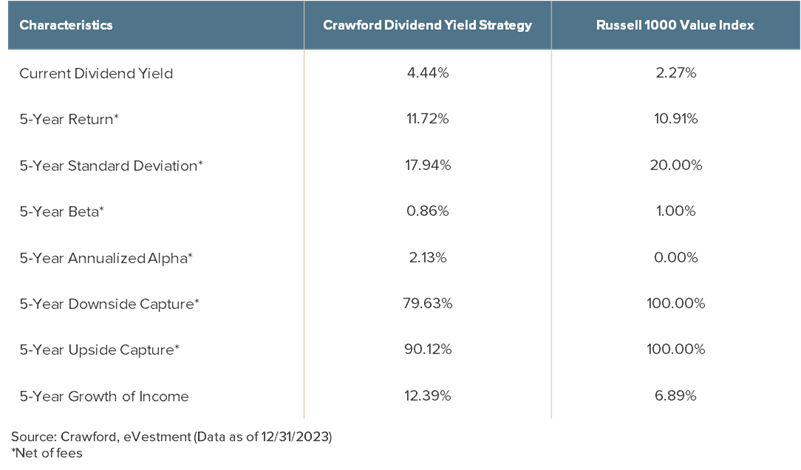

The risk, return, and income experience over the past five years is outlined below:

We believe the data points above are a proof statement that higher-quality, high-yielding stocks can produce both income and total investment return with lower risk and help protect capital in declining markets. This solid combination of return generation and risk reduction is achieved while targeting an overall yield in the 8th or 9th decile of all U.S. dividend-paying stocks. Through a rigorous fundamental research process, we identify those higher-yielding stocks that we believe have high Total Shareholder Return (TSR) prospects and above-average quality as measured by earnings consistency, balance sheet strength, and profitability (among others). Importantly, our high yield and high-quality orientation helps us avoid higher-yielding stocks that cannot sustain their dividends or where total return prospects are diminished.

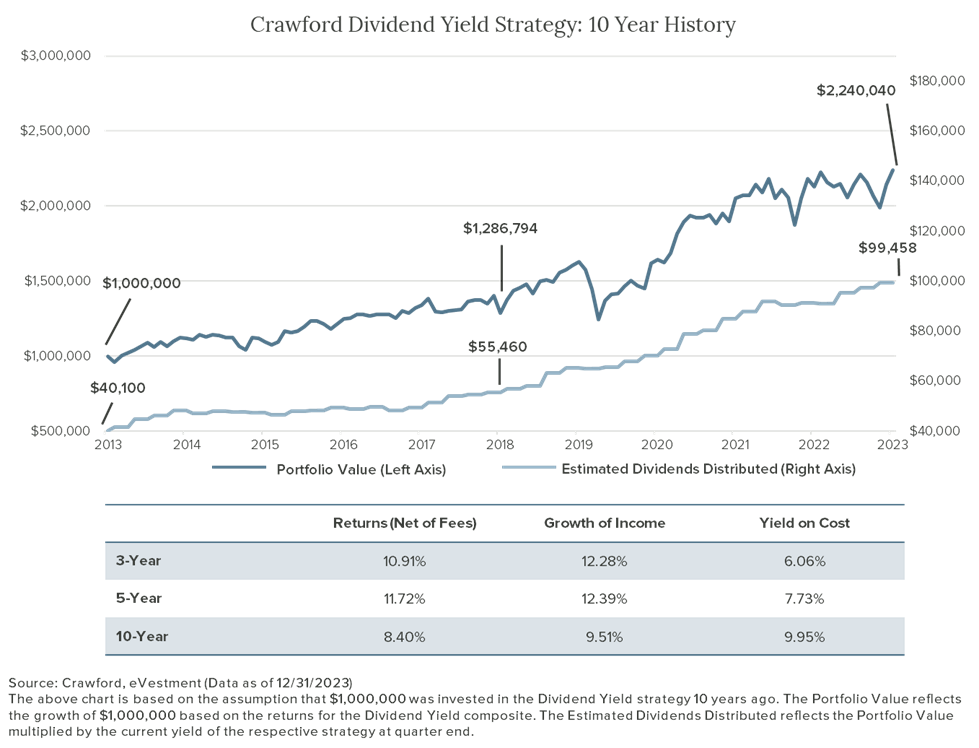

One aspect of our approach that is particularly attractive is the growth of income. In this strategy, growth of income is achieved by owning companies that increase dividends regularly, and it is buttressed by our active management process. In other words, we purchase companies with elevated and rising dividend yields, and often, the dividend yield is high because the stock is experiencing a temporary price dislocation. This can be a result of a short-term business issue or temporary decline in investor sentiment. Our fundamental, bottom-up research process and longer time horizon give us an edge and allow us to invest in these out-of-favor but high-quality stocks with a catalyst for reversion to the mean in valuation. These are investment opportunities that many investors overlook, ignore, or eschew due to shorter-term performance pressures and more myopic investment strategies. And, when the reversion to the mean begins and valuation starts to normalize, the price increases and yield typically decreases, offering us the opportunity to recycle the capital into another higher-yielding investment opportunity.

The level of income growth we have achieved in this strategy is high because we are effectively purchasing companies with elevated dividend yields, waiting for the fundamental improvement that we write into our investment theses, and selling the companies when the yields fall below an acceptable level for the strategy. The good news is that as the yield falls, it is due to the price of the stock increasing, contributing to total investment return in the process. Through employing this approach, we have been able to achieve income growth around or in excess of 10% for the 3-, 5-, and 10-year periods. While our Dividend Yield strategy has a slower dividend growth rate than our other strategies that focus on investing in companies with consistent dividend growth, it actually has a higher income growth rate due to the active management process described above. In turn, this high level of income growth creates a high yield on cost for the strategy, which we believe is a favorable outcome.

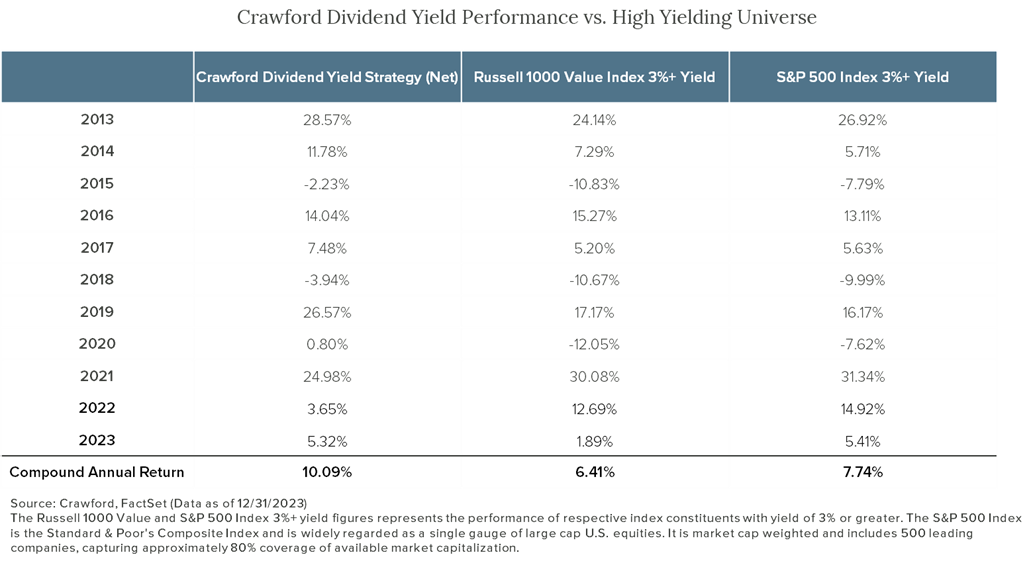

As an income manager seeking total investment return, our primary opportunity set for new investments is essentially stocks with yields of 3% or greater. The strategy has historically produced a yield somewhere around 4%, and it is currently 4.44%.

Our returns compared to 3%+ yielding stocks are illustrated below:

The strategy is particularly appropriate for the following investors, many of whom may be seeking a portfolio of higher-quality, higher-yielding stocks:

- Those seeking an attractive total investment return with lower risk

- Private clients who are in retirement or are soon to be living off their investments

- Endowments and Foundations that have spending needs

- Those concerned about portfolio income keeping up with inflation

- Risk-averse/defensive allocations to a value-oriented strategy

- Bond or C.D. owners who may wish to obtain equity exposure

To conclude, we believe a brief review of total investment return is in order. The formula is below, and as it relates to our Dividend Yield strategy, we expect both income and price appreciation to make substantial contributions to the total investment return over time.

Total Investment Return = Income Received (Yield) + Change in the Prices of the Securities

However, in any given year, stockholders need to be prepared for the fact that the price of the securities can decline, leaving investors with negative total investment return. This is why we appreciate the consistently high and rising income provided by the Dividend Yield strategy. Our investment approach has enabled us to deliver attractive, risk-adjusted returns over full market cycles, and we intend to continue to invest in this manner on behalf of our investors.

Disclosures:

To view a copy of the Dividend Yield composite disclosure, visit the following link: https://info.crawfordinvestment.com/hubfs/Dividend%20Yield%20Composite%20Reports%20-%202023%20-%2012%2031%202023.pdf

Past performance is not indicative of future results. Net of fee performance is calculated based on the actual fees experienced. Not every account will have these exact characteristics and there is no guarantee that another portfolio would have better or equal performance than the representative portfolio presented here. The opinions expressed are those of Crawford Investment Counsel and are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. The strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

The widely recognized benchmark(s) in this presentation are used for comparative purposes only. The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values. The S&P 500® Index is the Standard & Poor's Composite Index and is widely regarded as a single gauge of large cap U.S. equities. It is market cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization. It is not possible to invest directly in these indices. The volatility (beta) of the portfolios may be greater or less than the benchmarks.

Crawford Investment Counsel is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Crawford's advisory services can be found in its Form ADV Part 2 which is available, without charge, upon request. Additional information can be found at www.crawfordinvestment.com.

CRA-24-035

An Extreme Environment

As investors in high quality small cap companies, we have faced a uniquely challenging environment since the beginning of the COVID-19 pandemic.

An Extreme Environment... Revisited

As we approach the fourth anniversary of the COVID-19 pandemic, we wanted to revisit an article we published in mid-2021

The Golden Opportunity: Crawford Small Cap Strategy

We came to realize that the small cap area of the market might actually be the best place to reap the benefits of our long-held philosophy.