In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- We remain on recession watch, but we acknowledge the potential for a “soft-landing.”

- Given the defensive role we believe high-grade bonds play in our client portfolios, we continue to:

- Maintain a defensive credit bias with higher weighting to consumer non-cyclical corporate, tax-backed and essential service municipal, and government agency credits.

- Maintain opportunistic yield curve positioning by maintaining a 15-year laddered maturity distribution.

- We believe Fed funds rate cuts are forthcoming. Policy easing will likely initiate based on labor market and inflation data with the pace motivated either by:

- Recession = consecutive substantial cuts

- Normalization = periodic incremental cuts

- We are positioned for a decrease in interest rates. We believe our current yield curve positioning and bias to defensive credits provides our clients the opportunity to experience strong relative performance in recession or policy normalization scenarios.

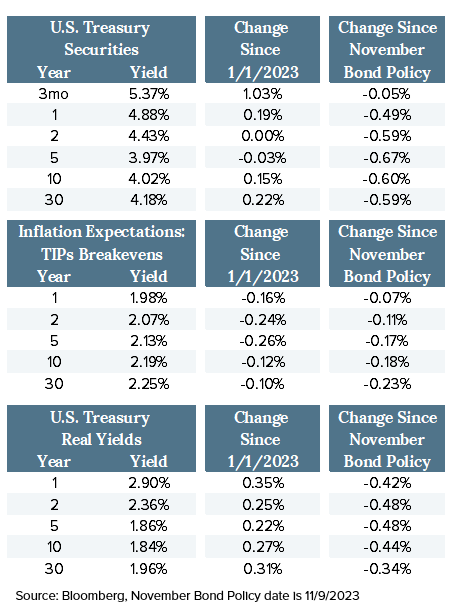

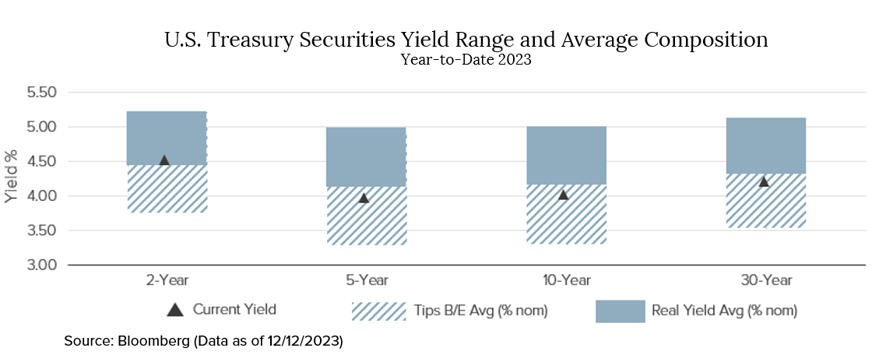

Treasury Yields as of 12/13/2023 (Post-Fed Meeting)

- Nominal Treasury yields have fallen progressively across the curve since our November Bond Policy meeting.

- The 3mo/10yr Treasury yield curve inversion (beginning in November 2022) deepened by ~56 basis points (bps), and the 2yr/10 inversion (beginning in July 2022) finished flat at -41 bps.

- Market inflation expectations, as reflected in TIPs (Treasury Inflation Protected securities) “Breakevens,” fell progressively across the curve.

- Real yields fell comparably to inflation expectations, until the Fed's meeting on December 13th when they dropped significantly across the curve.

- Fundamentally, the rally in bonds (decline in yields) over the past six weeks reflected a softening in fourth quarter U.S. economic data and improved inflation conditions. This was complemented by technical support, including a reallocation in U.S. Treasury security issuance from bonds to short-term bills which helped alleviate pressure on yields from term premium.

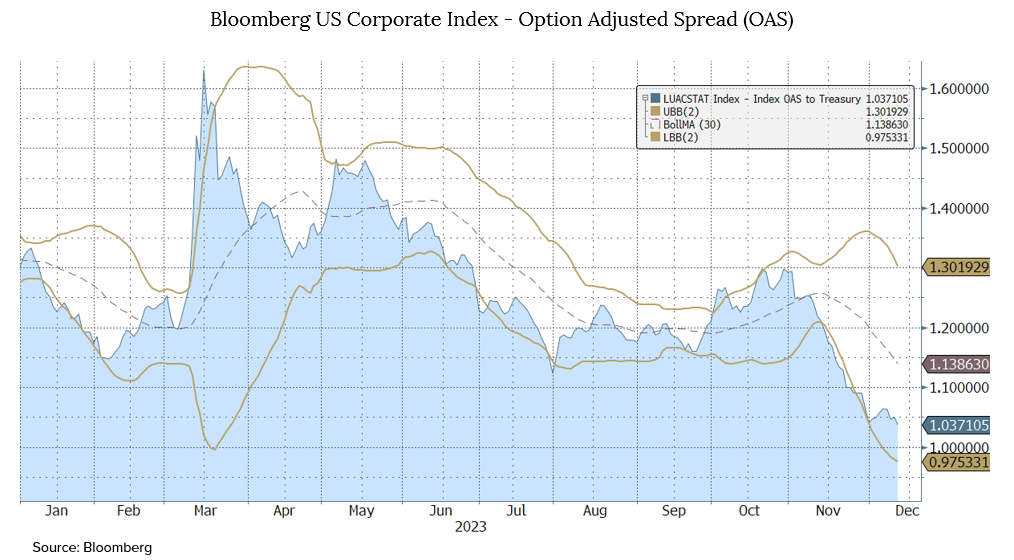

Corporate Bond Market

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- Investment-Grade Corporate OAS tightened meaningfully in the month of November and contributed to the high-grade bond market recording its best month of performance since 1985.

- The graph pictured below illustrates the “tight” nature of the current spread level.

- In 2024, the corporate bond market will face a high level of expected issuance based on a formidable wave of bond maturities stemming from the record issuance in 2020-2021.

- Recently published third quarter data does suggest high grade fundamentals have stabilized with the help of growth in earnings.

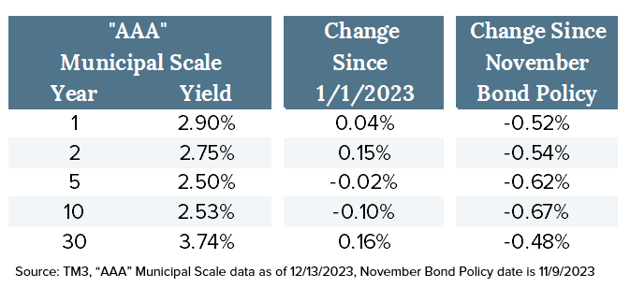

Municipal Bond Market

- Municipal bond yields have fallen dramatically since our November Bond Policy meeting and are down significantly from their October cycle highs.

- 5- and 10-year generic yields are currently below their levels at the beginning of 2023.

- Lack of new issue origination, thin trading, and the January effect will provide technical support to municipal prices through year-end and over the turn.

- Relative value metrics have fallen to extremely tight levels, as evidenced by current Muni/UST ratios versus historical averages.

- Despite the rapid decline, absolute yields remain attractive relative to the recent past.

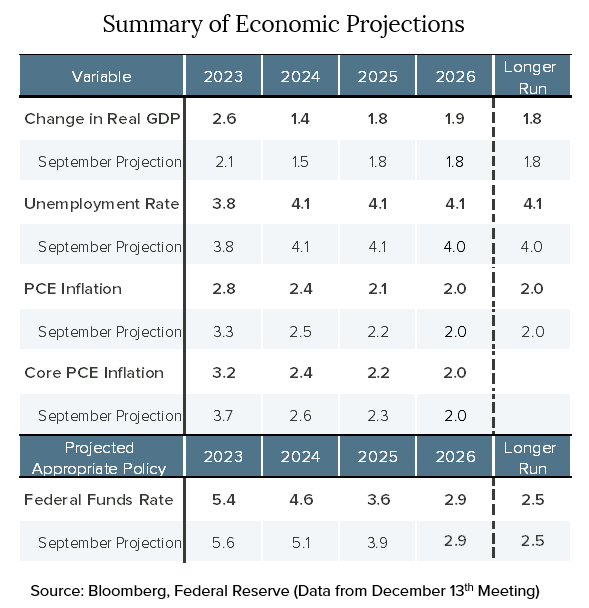

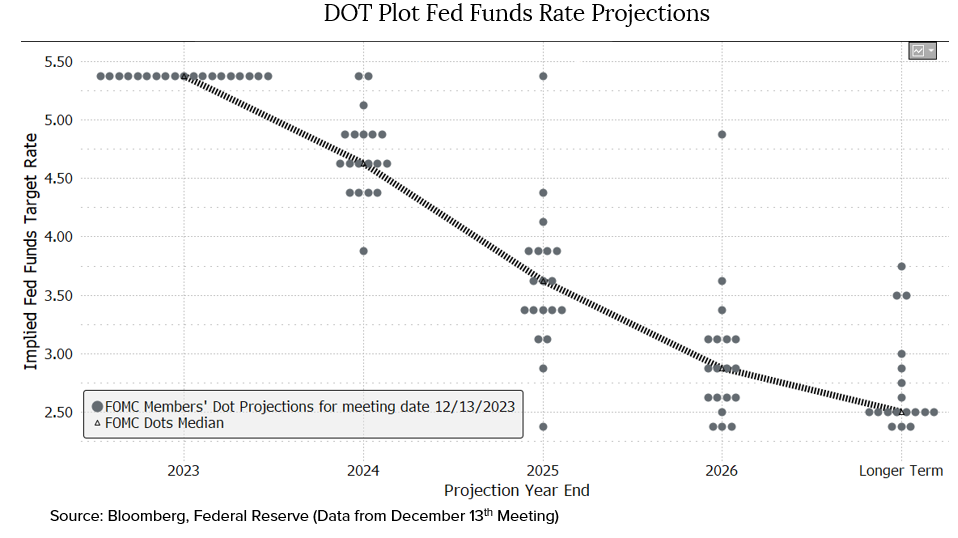

Summary of Economic Projections & Dot Plot

- Revisions to the economic and policy path projections include:

- Increase to expected Real GDP this year (up 0.50%).

- Core PCE inflation was revised down 0.50% for this year, 0.20% for 2024, and 0.10% for 2026. This illustrates how the committee is viewing the unexpected progress in disinflation.

- The projected Fed Funds target rate was cut 25 bps for 2023 (dropping the former 25 bp hike), 75 bps in 2024, 100 bps in 2025, and 75 bps in 2026.

- Projecting a steady level of unemployment at 4.1% suggests belief in the ability to soft land the economy, which is bringing inflation to target without labor market pain.

- The DOT Plot illustrates significant dispersion among policymaker expectations in 2025 and 2026. This is indicative of a policy turning point and lack of visibility.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-24-001

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.