As we approach the fourth anniversary of the COVID-19 pandemic, we want to revisit an article we published in mid-2021 titled An Extreme Environment. The article was written amidst a roaring stock market driven by unprecedented fiscal and monetary stimulus. As the title indicates, we were facing an extremely difficult environment for high-quality small cap stocks as investors poured money into struggling businesses that were seemingly given a new lease on life and into loss-making enterprises that depend on access to cheap capital. It was a “back from the dead” market rally, for sure.

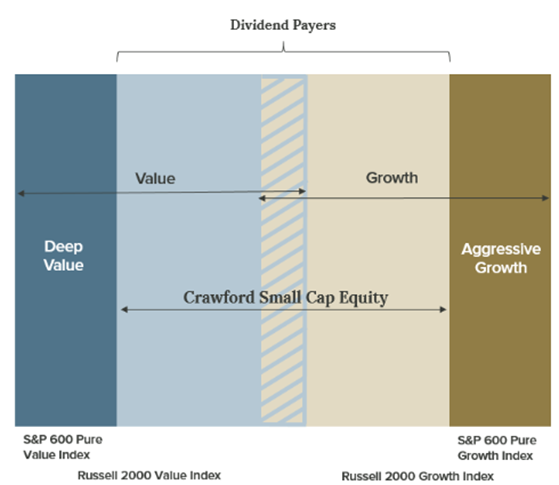

We used the following chart to illustrate this phenomenon. The display below shows all small cap stocks falling somewhere within the range of Deep Value to Aggressive Growth. As one gets further out on either end of the Value-Growth spectrum, quality attributes, including the ability to pay a dividend, begin to diminish. As one might expect, Crawford invests in the central part of the display, where we find Quality at a Reasonable Price (QARP) in small cap stocks. Because the huge rally was almost exclusively limited to low-quality stocks, dividend-paying stocks in the Russell 2000 Index underperformed non-dividend-paying stocks by 41%, which was the largest differential in recent memory.

During this particularly challenging period, we maintained our long-held philosophy and continued to invest in high-quality, dividend-paying companies with strong underlying business models. Our contention was that the outperformance of low-quality stocks was unsustainable, and a reversion to the mean was inevitable. Subsequent events have proven that we were indeed correct.

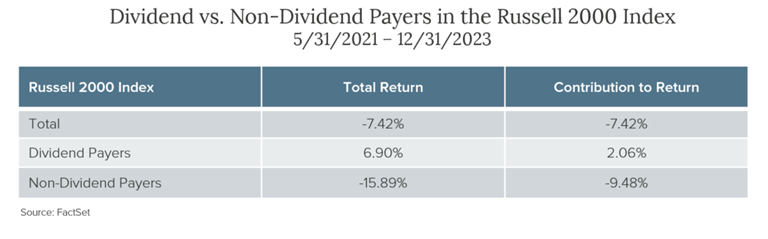

The table below shows performance data for dividend payers and non-dividend payers from 5/31/21 (the end date in our original article) through year-end 2023. The return disparity is once again stark, but it is the dividend payers that have been the big winners on a relative basis since we pointed out the disparity. From May 31, 2021 to year-end 2023, the Russell 2000 Index, which tracks the performance of small cap companies, was down 7.42% with dividend payers up 6.90% and non-dividend payers down 15.89%.

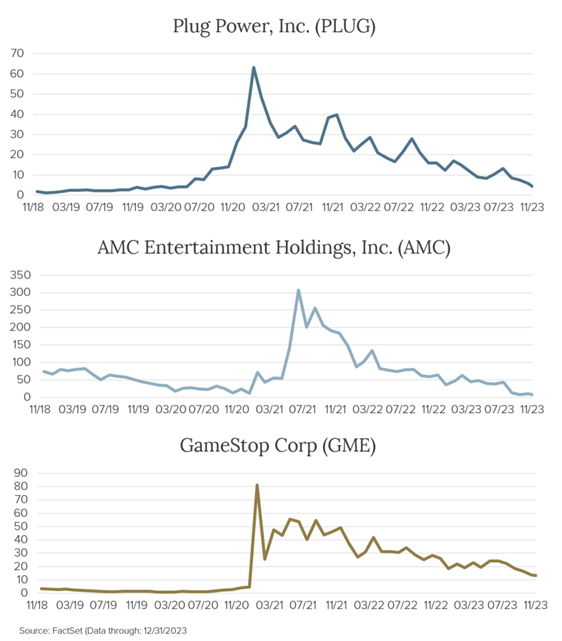

While the performance data speaks for itself and is consistent with long-term trends favoring small cap dividend-paying companies, we would also like to briefly revisit the Meme Stock phenomenon. This mania exemplified the post-pandemic investor disregard for fundamental analysis and traditional valuation metrics. As expected, much of the enthusiasm that surrounded a few small speculative companies that drove market performance has waned. The following displays show what has happened with a few of these meme stocks that captured speculative attention in 2020.

All of these companies offer a cautionary tale of low-quality, unsustainable businesses being bid up by investors for purely speculative reasons. A corollary of this story is that periods of easy money often lead to significant market distortions and ultimately end up hurting unwitting investors. This is an aspect of investing that we seek to avoid through our disciplined approach.

At Crawford, we prefer to purchase high-quality companies that can create shareholder value by consistently compounding earnings over time and returning capital to shareholders. While they certainly do not fall on the Deep Value side of the spectrum, these businesses can still represent good Value even when they trade at or near market valuation multiples. This can be attributed to the higher likelihood of fundamental improvement and lower probability of negative surprises. For the Crawford Small Cap strategy, we intend to continue to invest according to our long-held and rational discipline, regardless of how irrationally the market behaves over the short term. We expect our investors will continue to be rewarded by our approach.

Looking ahead, we view the evolving environment as somewhat of a mirror image of what we experienced in 2020. The cost of capital is much higher and even if the Fed does cut rates this year, we do not foresee a return of the type of liquidity-driven bull market we experienced in 2020 for some time. We also recognize that the economy is now at a more advanced point in the cycle, and while we are not predicting a recession, which would severely impair the earnings of lower-quality small cap companies, we are certainly not ruling it out either. With all of this considered, in all likelihood, we believe the environment will continue to be less conducive for lower-quality small cap companies (Deep Value) and also less fertile for highly-valued small cap companies (Aggressive Growth). This all augurs well for a QARP approach such as ours that focuses on companies that can demonstrate consistent and predictable fundamental progress in a variety of economic scenarios.

Disclosures:

Past performance is not indicative of future results. The opinions expressed are those of Crawford Investment Counsel and are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. Nothing herein should be construed as a solicitation, recommendation, or an offer to buy, sell, or hold any securities, other investments or to adopt any investment strategy. The strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

The widely recognized benchmark(s) in this presentation are used for comparative purposes only. Russell 2000 Value® Index measures the performance of the small cap companies located in the United States that also exhibit a value probability. Russell 2000® Growth Index measures the performance of the large cap growth segment of the US equity universe. The S&P 500® Growth measures growth stocks using three factors: sales growth, the ratio of earnings change to price, and momentum. Constituents are drawn from the S&P 500®. The S&P 500® Value measures value stocks using three factors: the ratios of book value, earnings, and sales to price. Constituents are drawn from the S&P 500®.

Crawford Investment Counsel is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Crawford's advisory services can be found in its Form ADV Part 2 which is available, without charge, upon request. Additional information can be found at www.crawfordinvestment.com.

CRA-24-036

An Extreme Environment

As investors in high quality small cap companies, we have faced a uniquely challenging environment since the beginning of the COVID-19 pandemic.

New Year's Resolutions for Your Portfolio

The good news about these resolutions? We are certain we will keep them. We have a time-tested philosophy and a 40+ year history of sticking to it.

High and Rising Income: Crawford Dividend Yield Strategy

In this strategy, growth of income is achieved by owning companies that increase dividends regularly, and it is buttressed by our active management process.