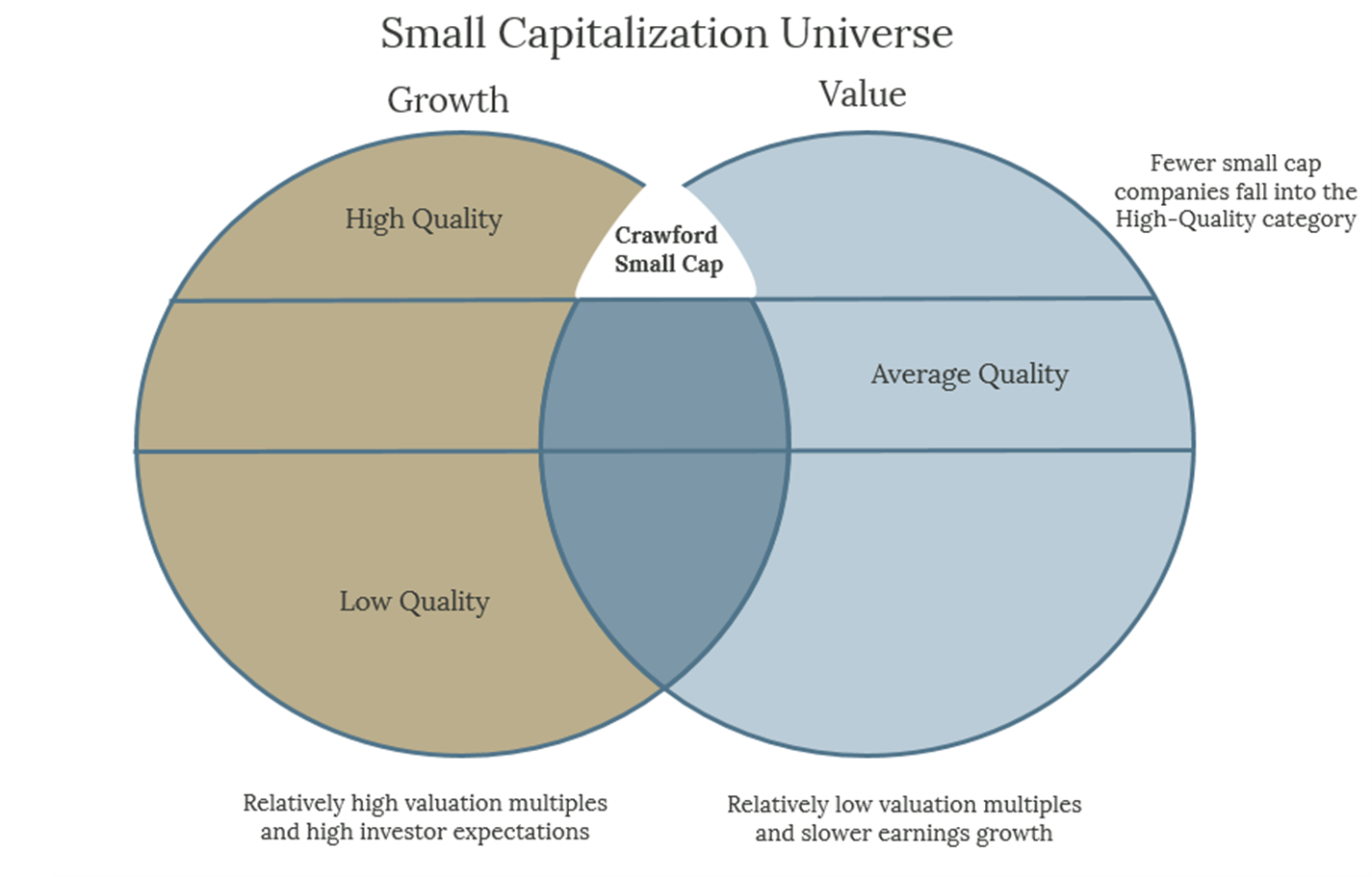

Today there is probably a disproportionate amount of emphasis put on classifying investments as belonging to one of two styles: Growth or Value. Growth investing is focused on seeking out companies that have the potential to outperform the overall market because they can compound earnings at a faster rate. Value investing, on the other hand, is focused on identifying companies that trade below what they are really worth and that can generate superior returns as the valuation gap is eliminated. Traditionally, stocks in the Value category have been associated with relatively low valuation multiples and slower earnings growth while, conversely, Growth stocks often feature relatively high valuations and high investor expectations.

Both styles can lead to successful investment outcomes, but they can also go in and out of favor depending on macroeconomic conditions and the stage of the economic cycle. History shows that periods of underperformance by a particular style can stretch over multiple years. Additionally, myopic focus on only a couple of investment attributes (valuation and/or projected growth) can lead to painful surprises down the road.

To address some of the weaknesses associated with the two investment styles, a new approach was developed that combined the best features of both Growth and Value investing. It became known as Growth at a Reasonable Price or GARP. Essentially, GARP investors seek to obtain superior growth characteristics while trying to avoid paying excessive valuation multiples.

From our vantage point here at Crawford, neither of these approaches adequately captures the most durable outperformance factor in small cap investing – Quality. At our firm we have developed a rigorous investment process that puts Quality at the center of our decision-making, an approach we call Quality at a Reasonable Price or QARP for short. In a nutshell, this approach entails identifying the highest-quality businesses that are positioned for attractive earnings growth where investor expectations (and, by extension, valuations) have not become excessive.

We define quality businesses as those with less cyclical earnings, high profitability, low debt levels, high free cash flow generation and consistently growing dividends. There are many reasons why these types of small cap companies outperform in the long run, but perhaps one of the most underappreciated factors has its roots in investor inability to adequately account for risks inherent in small cap investing. We have observed that even professional investors often approach the small cap space with a “swing-for-the fence” mentality and a focus on earning outsized returns. These types of returns can only be obtained from lower-quality, deep value, or speculative growth stocks. However, many of these companies have compromised balance sheets, outdated or unproven business models, and require a favorable external environment (e.g., low interest rates) to perform well. These characteristics can ultimately lead to a much wider range of outcomes than what investors might be betting on.

We fully realize that stocks with the attractive quality characteristics mentioned above rarely trade at cheap valuations. Furthermore, we believe it is important to distinguish the concepts of Value and Valuation. Traditional Value investors can become overly focused on finding stocks that trade at low valuations (such as low price-to-earnings or price-to-book ratios) while paying little attention to whether these stocks represent actual value, i.e., undervalued relative to their growth prospects. A classic (and perhaps somewhat extreme) example of the Value and Valuation disconnect would be a retailer with a high fixed cost base in the form of real estate leases that borrowed heavily during a period of low interest rates but is subsequently challenged by the change in consumer shopping habits. A stock like this would typically trade at low valuation multiples, but its value would be approaching zero due to a looming bankruptcy.

At Crawford, we prefer to purchase high-quality companies that can create shareholder value by consistently compounding earnings over time. These businesses could still represent good Value even when they trade at less attractive valuation multiples given higher likelihood of fundamental improvement and lower probability of negative surprises. That said, we are keenly aware that the price (valuation) paid at the time of stock purchase can have a meaningful impact on the investment outcome. Thus, we perform extensive due diligence on all companies we invest in that also involves a comprehensive valuation assessment.

We believe our investment in U.S. Physical Therapy (USPH) is a great example of the application of our QARP philosophy. USPH is one of the largest operators of outpatient physical and occupational therapy clinics in the U.S. The company does not own the buildings where its clinics are located, which allows it to generate an above-average Return on Invested Capital (ROIC) versus other asset-heavy facility operators like hospitals. The company’s business model is further enhanced by its partnering approach, where local management and acquired clinics retain equity in individual facilities as a part of compensation. The company benefits from steadily growing and recession-resistant demand for physical therapy services. It has also been taking share in the fragmented market by acquiring physical therapy practices. Our investment thesis was formed around our belief that USPH had sufficient runway to continue consolidating the industry and enjoy increasing benefits of scale. When we purchased USPH, the stock traded at a P/E ratio of 16x or 20% premium to the Health Care sector, which would have put the stock outside of the traditional Value category. However, we felt that valuation multiples were very reasonable relative to the business quality and long-term growth potential. We have owned USPH for approximately 10 years, and during this period the company has compounded earnings at an annual rate of 7.2% while the stock delivered total return of 216%, handily beating the 80% return generated by the Russell 2000 Index (both figures are for 10 years ending 10/3/23). At the time of purchase, USPH had a market cap of ~$300M vs. ~$1.4B today.

In summary, as adherents of the QARP approach, we are price-sensitive investors who seek growing enterprises that demonstrate fundamental progress year in and year out. Our insistence that all purchase candidates exhibit key quality characteristics leads to a narrower range of potential investment outcomes and increases the likelihood of capital appreciation. This approach has helped us avoid the pitfalls of other prevalent investment styles and deliver attractive, risk-adjusted returns over time.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

This material is distributed for informational purposes only. The company identified above is an example of a holding and is subject to change without notice. The company has been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment recommendations or decisions we make in the future will be profitable.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-198

The Perpetual Accumulation Approach: Can You Have Your Cake and Eat It Too?

At Crawford, we believe that by investing in quality, employing a price sensitive approach, and establishing reasonable spending policy, our investors can have their cake and eat it too.

The Grand Experiment

While equities are our asset class of preference, we believe the best approach for many investors often includes a mix of both stocks and high-quality bonds.

The Important versus the Easy

The level of consistency in free cash flow generation is an important criteria in our quality screening process.