We live in an uncertain world that is full of surprises. In 2022, Ukraine was invaded, spending patterns rapidly shifted in the aftermath of the pandemic, and we witnessed the highest inflation in decades. All of these factors influenced the markets and economy, and very little of this could have been predicted in advance. Given the Federal Reserve’s (Fed) strongest ever response to inflation and an inverted yield curve, most were calling for recession as we entered 2023. In fact, consensus expectations stated that the Fed would be cutting rates by now. Yet, the economy is on firm footing today and monetary policy is still restrictive. Once again, we are reminded of the unpredictability of the investment landscape. This only serves to underscore the importance of our long-held objective of seeking to bring as much certainty as possible to the investment equation.

Since most were predicting a recession in 2022, the outlook for stocks was poor coming into this year. These expectations were rooted in historical patterns and what has traditionally occurred in the aftermath of rapid monetary policy tightening. However, this has not been the case. Instead, the stock market is up solidly, at least as measured by the S&P 500 Index. It should be noted that many are still expecting a recession, although the possibility of a soft landing has improved. At Crawford, we remain on recession watch.

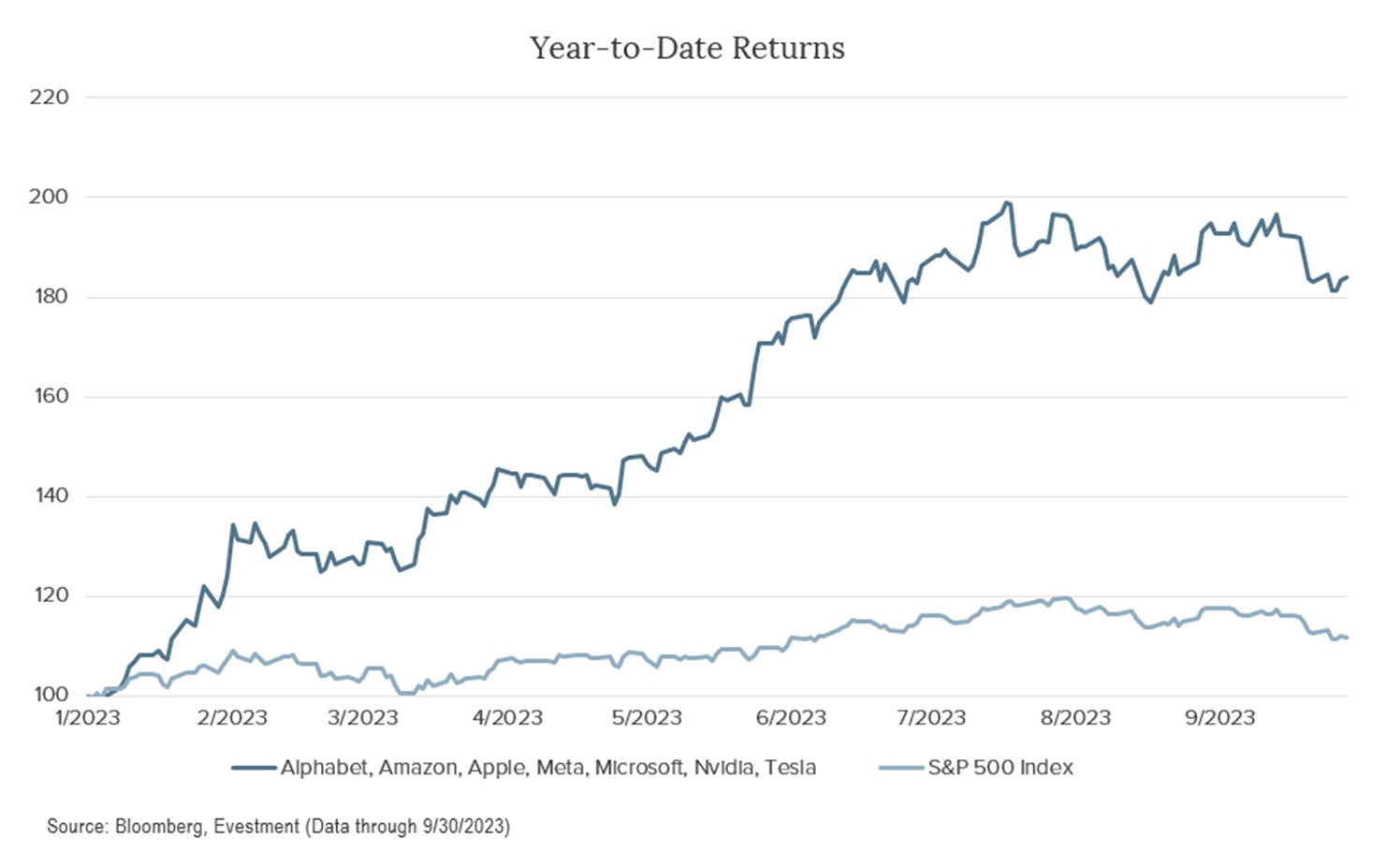

The S&P 500 Index is up roughly 13% for the year-to-date period, which means it has experienced a significant recovery since the market drawdown in 2022, although it remains below its all-time-high level achieved on January 3, 2022. Again, very few would have predicted such, particularly against the backdrop of a potential recession. What might be missed is that while the index is up substantially, the recent strength of the stock market has been exceptionally narrow and driven by a small number of stocks, many of which are expected beneficiaries of AI (Artificial Intelligence). This narrow nature of the market’s recent advance is not a common phenomenon, but it does occur periodically, most typically in the later stages of the economic cycle.

Stock investors have reacted to the current period of uncertainty by investing in index funds and strategies that mimic the S&P 500 Index. What these investors are doing is, in essence, flocking towards seven very large companies, some of which are richly valued with high, embedded expectations. The recent performance of the S&P 500 Index has been dominated by these seven stocks, commonly referred to as the “Magnificent Seven.” These companies, which include Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla, have done inordinately well this year and now comprise nearly 30% of the index.

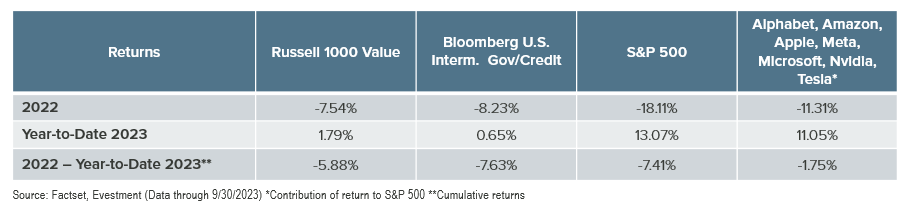

To give some more context on the disparity of returns between these seven companies and the rest of the market, we can share that for the first three quarters of the year, the S&P 500 Index returned 13.07%. However, if we look at an equal-weighted measure of the index, where position sizes are equally distributed across all constituents, the year-to-date performance is only 1.79%. Or, it might be helpful to explain that these seven companies have produced returns of ~84% for this year, while the remaining 473 constituents have earned far more modest returns. The display below illustrates the performance of these seven stocks alongside the performance of the entire S&P 500 Index thus far in 2023. By looking at the chart, one can begin to understand just how great of an impact these seven companies have had on overall index performance.

While the S&P 500 Index’s returns have been strong this year, investors must remember that the return experience, overall volatility, and downside risk of an investment matter. The index’s return for the past 21 months (since the beginning of 2022) is still negative at -7.41% on a cumulative basis. The table below demonstrates that, while the S&P 500 Index’s returns in 2023 have been high and largely driven by these seven companies, they have not been strong enough to counteract the negative returns experienced in 2022. The table also demonstrates that the lows of 2022 were largely driven by negative returns from the same seven companies that have driven recent performance up.

We will refrain from prognostication about how this might end, but we do not expect it to be favorable for all investors. Market weakness led by these seven stocks may portend difficulty for the stock market, but we are confident that our investors will be protected through their investments in more consistent, predictable companies with lower embedded expectations and strong business models. We also know our investors will continue to receive dividends regardless of the market environment, many of which will be increasing regularly. We believe this will help get them through a potentially difficult period for stocks, just as it did in 2022.

At Crawford, our strategies are engineered to embrace the reality of uncertainty. We prefer to pursue an active management process that seeks diversification across sectors, industries, and position sizes. We expect to participate when markets surprise on the upside and protect when markets disappoint on the downside. We believe this enables our clients to better meet their objectives in any market environment, and we intend to continue to invest in this manner.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

This material is distributed for informational purposes only. The company identified above is an example of a holding and is subject to change without notice. The company has been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment recommendations or decisions we make in the future will be profitable.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-204

Uncertainty is Certain

Life is filled with uncertainties, and this reality actually serves as one of the basic premises for Crawford Investment Counsel’s investment philosophy.

The Total Shareholder Return Trifecta

We invest to achieve an investment trifecta by selecting stocks that provide our investors with all three components of total investment return: fundamental business progress or growth, dividend yield, and valuation improvement

Quintessential Quality

While there are examples of high-quality companies across the market, few sectors are so densely populated with quality as the Consumer Staples sector.