In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- We remain optimistic about the potential for a "soft landing."

- We also remain realistic regarding the likelihood of a cyclical downturn. Given the role we believe high-grade bonds play in our client portfolios, we will continue to:

- Maintain a defensive credit bias with higher weighting to consumer non-cyclical corporate, tax-backed and essential service municipal, and government agency credits.

- Maintain opportunistic yield curve positioning by extending our maturity spectrum to 15 years.

- Maintain a defensive credit bias with higher weighting to consumer non-cyclical corporate, tax-backed and essential service municipal, and government agency credits.

- A recent example of our approach is the sale of our U.S. Bank and Charles Schwab corporate bond positions in favor of a longer-term Johnson & Johnson holding. This allowed us to further mitigate exposure to financial capitalization and funding challenges posed by the current rate environment, in favor of investing in a non-cyclical “AAA” rated medical device and pharmaceutical company, locking in an attractive yield at the longer end of our maturity spectrum.

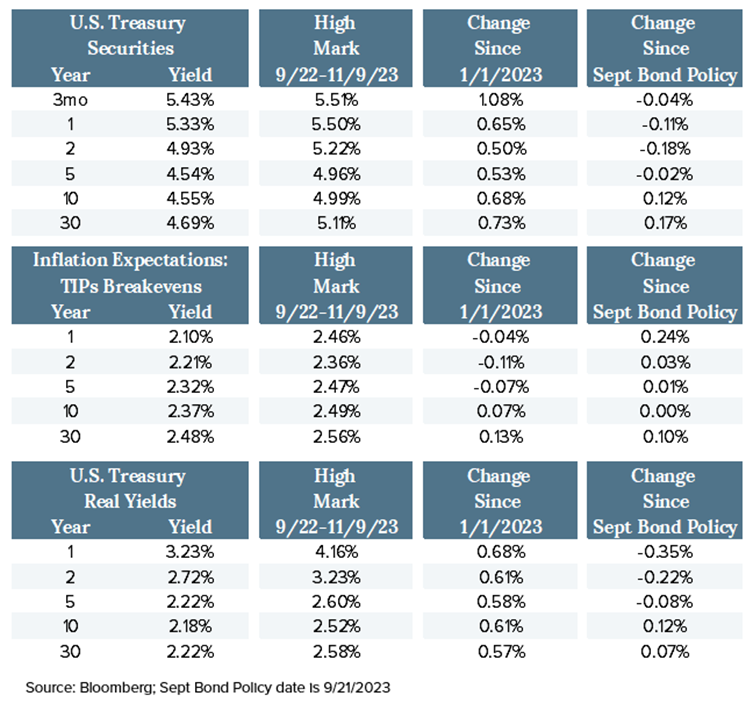

Treasury Yields as of 11/8/2023 (Post-Fed Meeting)

- Nominal Treasury yield movement has been mixed across the curve since our September Bond Policy meeting.

- The 3mo/10yr Treasury yield curve inversion (beginning in November 2022) flattened by ~17 basis points, and the 2yr/10yr inversion (beginning in July 2022) flattened by ~31 basis points.

- Market inflation expectations, as reflected in TIPs (Treasury Inflation Protected securities) “Breakevens,” moved higher in 1yr and 30yr maturities, while the belly of the curve was virtually unchanged.

- Real yields were mixed with declines in short maturities and modest increases further out the curve.

- Nominal yields declined significantly from their recent highs over a short time period based on:

- A drop in term premium resulting from a surprise Treasury refunding announcement which skewed issuance to shorter-term securities.

- The Fed maintaining rate policy backed by less hawkish rhetoric regarding further policy tightening.

- A weaker than expected October employment report.

- The bond market is exhibiting increasing confidence that the Fed may have reached the Fed Funds Terminal Rate for the cycle with the help of financial conditions tightening due to Term Premiums rising on longer-dated securities.

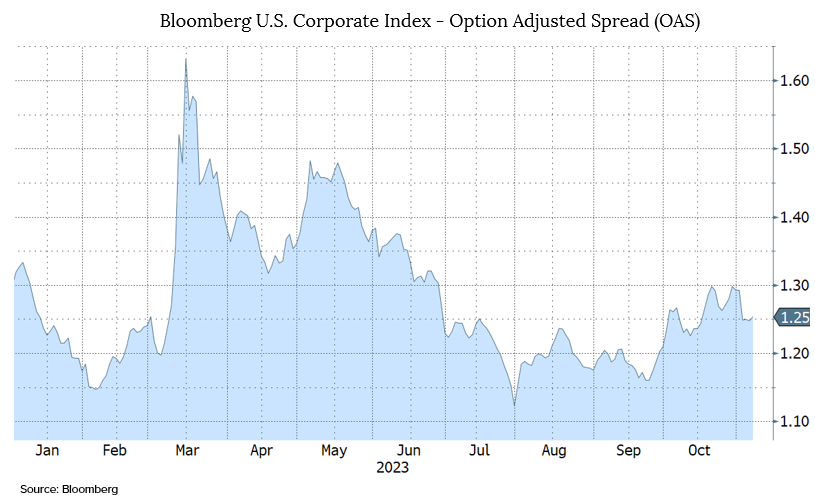

Corporate Bond Market

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- Investment Grade Corporate OAS has widened since our September Bond Policy meeting. However, it has performed very well relative to the increase in market volatility.

- Correlation between OAS and volatility has declined. This performance has been supported by continued strong demand and manageable new issue supply. Despite the increase in spreads, OAS has remained below its 30-year average of 1.32.

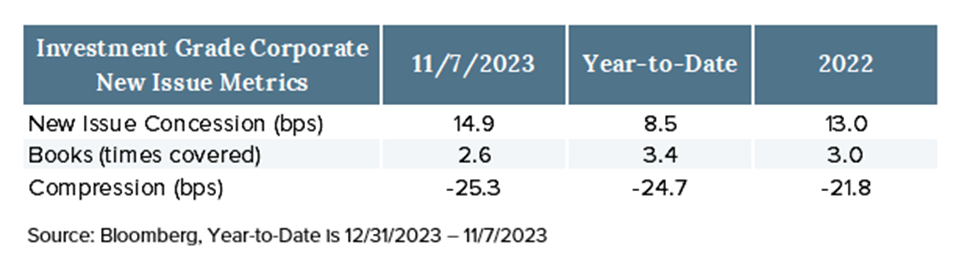

- Yield spreads continue to be supported by strong demand, as illustrated in new issue statistics below.

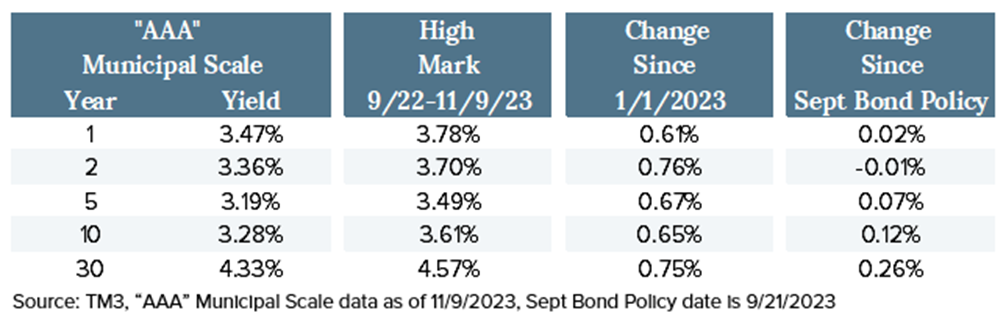

Municipal Bond Market

- Like Treasury securities, Municipal Bond yields are down significantly from recent highs, but are modestly higher since our September Bond Policy meeting.

- Municipal relative value metrics remain in “rich” territory from a historical perspective, but have improved recently.

- Factors supporting municipal bond prices include:

- Attractive absolute yields

- A net-negative supply outlook for the balance of 2023

- Factors supporting higher municipal bond yields include:

- Continued net fund outflows

- Tax-loss harvesting

The Term Premium Effect

Conclusion: Term Premium is back in market lexicon helping to define the attribution of yield movement. It has re-established its importance in explaining yield changes at a time when market and consumer inflation expectations are contained, but other monetary and cyclical forces are pushing yields higher. With higher yields come tighter financial conditions, helping the Fed achieve its policy goal. It remains to be seen whether higher term premiums have provided a means for the Fed to have reached the Terminal Funds rate for the cycle.

Term Premium is defined as investor compensation for risk associated with a long-term security. It is also regarded as the portion of interest rates not attributable to expectations for future Fed policy. Multiple models exist which estimate the level of term premium. Ultimately, however, the term premium is a hypothetical figure, similar to the Natural Rate of interest. As the yield curve steepens (long-term rates moving higher more than short-term rates), the market is discounting factors beyond anticipated future Fed policy (reflected in 2-year Treasury yields). These factors may include compensation for an expected increase in real economic growth, and/or a general increase in perceived risk.

- Recently, term premiums are believed to have moved higher due to factors including:

- The increase in current and projected Federal fiscal deficits.

- The decrease in U.S. Treasury security demand due to the Fed’s quantitative tightening program.

- Diminished capacity/demand from U.S. financial institutions and other central bank buyers (e.g., China and Japan).

- And, (as Chair Powell put it) the market's overall view of the strength of the U.S. economy.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-209

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

December Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.