In an effort to examine a number of changes occurring in the capital markets, we have been considering the theme of pendulum shifts. Many longstanding trends and series, some of which have been in place for decades, have shifted in an opposite direction. When considering the past few years, perhaps the most significant change in the capital markets has been the recent increase in interest rates. The rise in rates has been dramatic and had a pervasive effect across financial markets. The swift nature of the rate changes has heightened the intensity of its impact, made more profound by the near zero interest rates experienced across the yield curve just two years ago.

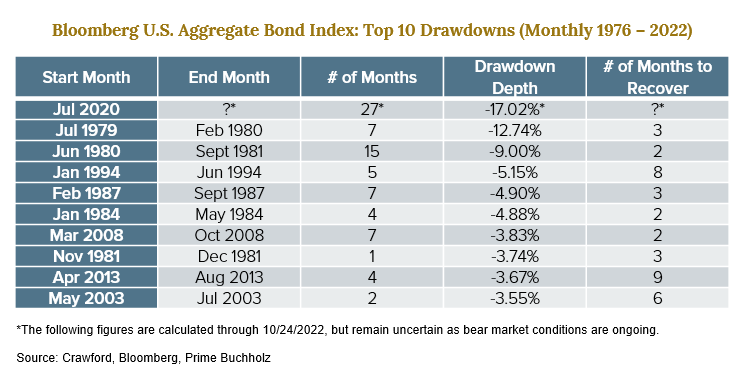

Using the Bloomberg U.S. Aggregate Bond Index as a proxy for the bond market, the table below puts the current bond bear market into perspective. Compared to the 10 worst performance periods experienced over the past 50 years, the past 27 months represents the worst period for bond total returns by a significant margin. Bonds have been in a negative return environment for over two years, but the vast majority of the interest rate increase occurred this year driven by Fed Policy tightening and the worst inflation readings in 40 years.

It is worth noting, if today was the last day of 2022, this year would represent the worst single calendar year for bond investors since at least the early 1900s.

As mentioned earlier, the impact of inflation and rising interest rates has been pervasive across financial markets. Currency and stock markets have also experienced declines as the higher inflation and interest rate environment has compressed the values of non-U.S. currencies and earnings multiples on stocks. For more information, read this and this.

So, why has the pendulum shifted? The most obvious answer is inflation, which is currently running at over 8%, an unacceptably high level for a developed economy such as ours. Inflation began its steep ascent in the second quarter of 2021 due to a combination of pandemic-induced supply chain pressures and insatiable consumer demand born of strong personal balance sheets and federal stimulus. In March of this year, the Fed began its campaign to fight inflation by raising the Fed Funds Target Rate, the overnight lending rate between banks. It is their primary policy tool and acts as a base rate for credit markets in the U.S. As of this writing, they have raised the rate from near 0% to 4%. This is a remarkable increase for markets to digest in less than a years’ time. It is safe to say additional rate increases are likely at future Fed meetings with their stated determination to tame the inflation beast.

Prior to the pandemic, inflation in the U.S. had experienced a secular decline that started in the 1980s with the inflation crushing monetary policy of the Paul Volcker Fed and the advent of globalization, which reduced labor costs and goods prices. With the pendulum now appearing to shift toward some degree of de-globalization, the longer-run effects could be higher inflation and interest rates than the economy experienced during the post-financial crisis cycle. The near-term answer lies in knowing the portion of the current inflation issue that is cyclical and influenced by Fed policy, and the portion that is structural and more difficult to tame.

We believe a silver lining exists in the current environment for investors with a long-term investment perspective. Yields are higher in the bond market and signs are pointing to a stage of the economic and interest rate cycle when it has historically been advantageous to extend maturities in securities less credit-sensitive to an economic downturn. One of the signs is the shape of the U.S. Treasury security yield curve. Typically, a flat, or inverted yield curve where short-term securities have the same or higher yields than long-term securities has been more rewarding for investors in the longer-term securities over a similar investment horizon. For example, in August 2006, 2-year and 10-year Treasury securities had approximately the same yield of 5.14%. If an investor bought the 2-year bond and rolled it over 4 times, their simple average yield over the 10-year investment horizon would have been 1.83% as opposed to 5.15%. We believe now is a good time to consider extending maturities to lock in attractive yields.

Amidst the aforementioned declines in the bond market, Crawford has maintained its longstanding bias to high quality. This coupled with a common sense approach to maturity management, adequate diversification, and prudent utilization of spread sectors to increase yield, has helped preserve capital in a very difficult environment. We believe successfully navigating market environments like the one we are currently experiencing demonstrates the true quality of a bond manager. Fortunately, our client portfolios have maintained protection from credit and market risk, and experienced losses much lower than the popular averages. We believe this contributes to the avoidance of any permanent loss of capital and sets the stage for a more expeditious recovery when markets begin to appreciate again.

Please reference our related Podcast for more detail:

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio.

This material is not financial advice or an offer to sell any product.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-264

The Tale of Transitory Inflation

Our goal with this piece is not to comment on this ongoing debate, but rather to question whether transitory inflation is, like the Boogeyman, imaginary.

Prevailing Through Challenges: Interview with Small Cap Manager

We are really pleased with our strategy’s recent outperformance, because there have been several underlying trends in the market working against us.

New Year's Resolutions for Your Portfolio

The good news about these resolutions? We are certain we will keep them. We have a time-tested philosophy and a 40+ year history of sticking to it.