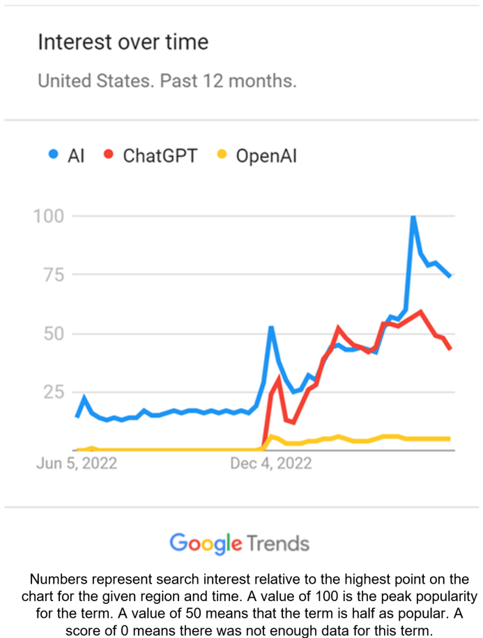

In November, the release of OpenAI’s ChatGPT marked the beginning of the commercial phase of the global race in artificial intelligence. This activity is driving increased investor, public, and media interest.

Below we have highlighted the notable spike in Google searches related to this topic.

More recently, the company’s release of its latest model, GPT-4, has increased the stakes. GPT, or Generative Pre-trained Transformer, models are specialized algorithms that find patterns in data and generate creative output. Prior AI models were best applied to decide the “next best actions,” while GPT models can now write essays, draft emails, handle routine customer interactions, and even create works of art. Generative AI is currently being used in many novel ways, from writing fortune cookies to processing Wendy’s drive-thru orders.

According to the International Data Corporation, annual global spending on AI services and cognitive systems reached $57.6 billion in 2021, and it is expected to reach $126 billion by 2025. Further, PwC estimates that AI could contribute up to $15.7 trillion to the global economy in 2030 including $6.6 trillion from increased productivity and $9.1 trillion in consumption side effects. These staggering figures are too significant for investors to ignore. Given the global scale of this spending, how can investors take advantage of this opportunity?

At Crawford, we focus on high-quality, more predictable, dividend-paying companies. These securities are combined into portfolios with the intent of delivering superior risk-adjusted returns, downside protection, and current income. Ultimately, we believe these factors lead to successful outcomes for our investors. Here are three examples of dividend-paying portfolio holdings that both meet our stringent investment criteria for quality, while also standing to benefit from ballooning global AI spending.

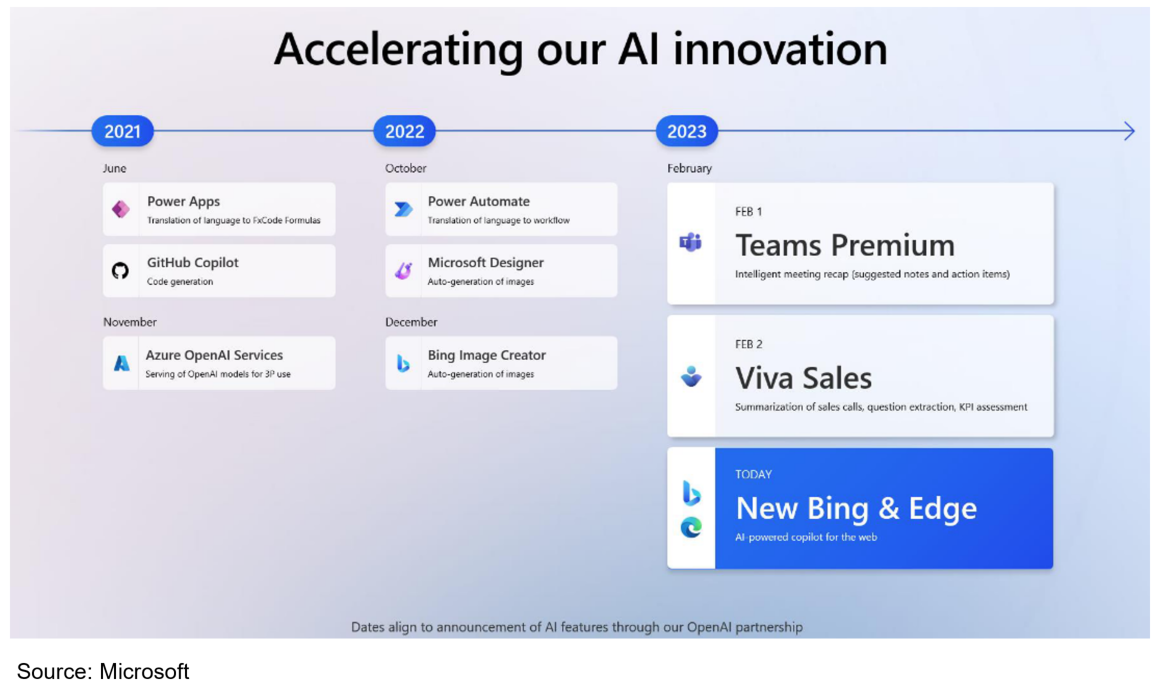

Microsoft Corporation (MSFT): Supported by over $200 billion in annual sales, Microsoft is a global leader in enterprise software and cloud computing. We believe Microsoft is strategically positioned to lead the charge in enabling enterprises to benefit from generative AI. The company is OpenAI’s largest investor and has an exclusive license to utilize its technologies across its product suite. Under the visionary leadership of CEO Satya Nadella, Microsoft originally invested $1 billion into OpenAI in 2019 and invested an additional undisclosed amount in 2021. In January of this year, the company agreed to invest up to $10 billion.

This year, Microsoft created waves by adding ChatGPT technology to enhance their internet search capabilities with the creation of Bing Chat. Further, the company is already monetizing generative AI for computer programmers through their Copilot for GitHub. Other Copilot offerings are being expanded throughout their software stack including Copilot for Office 365, Copilot for Dynamics, Copilot for Viva sales, and Copilot for Secure. In addition, through its Azure cloud platform, the company offers direct access to OpenAI’s models. We believe the long-term revenue opportunity for Microsoft is immense. In fact, on their last quarterly earnings call, they noted that Azure was already seeing a tailwind from increased consumption in AI, which should add 1% to growth next quarter.

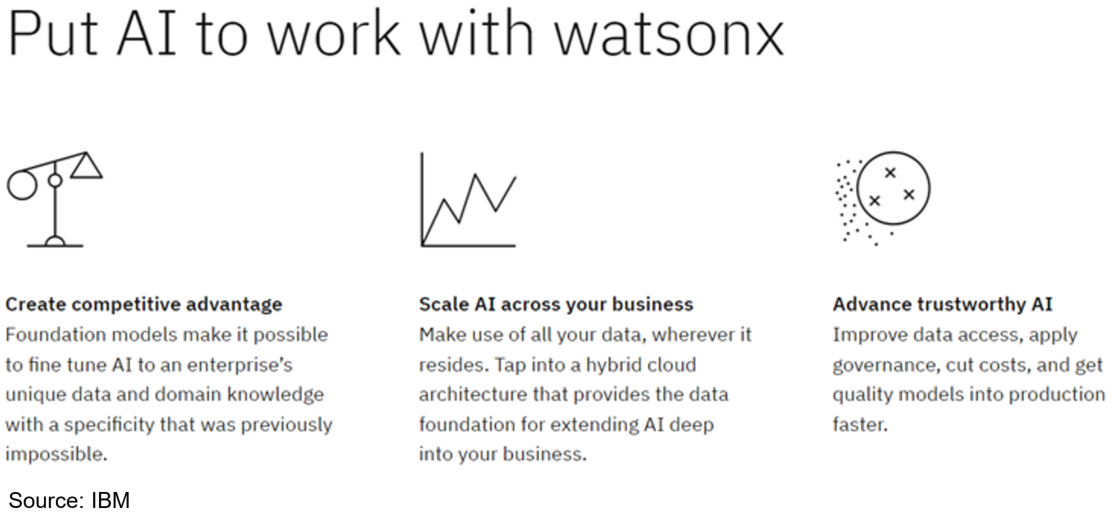

IBM Corporation (IBM): IBM is also a stalwart in enterprise information technology and services. The company’s customers include 90% of the world’s top banks, 9 of the top 10 oil and gas companies, 40 of the top 50 global retailers, and 92 of the top 100 global healthcare organizations. This month at its annual Think conference, IBM unveiled its enterprise-focused AI platform called watsonx. The platform is a new AI and data platform that will allow enterprises to scale and accelerate the most advanced AI with trusted data. It includes three major components which allow users to 1) train, validate, train, and deploy AI models, 2) store data optimized to scale to the massive levels required by AI models, and 3) be alerted of data changes and detect bias. Importantly, watsonx will pull from disparate data sets, both internal and external, while providing comprehensive security and transparency. We believe that IBM will monetize these capabilities by leveraging a subscription model. IBM also announced a new consulting team to assist customers as they begin using its generative AI platform. This opportunity appears to be material to IBM’s growth prospects, and we look forward to progress updates as the year progresses.

Broadcom, Inc. (AVGO): Broadcom is the sixth-largest global supplier of semiconductors. The company is comprised of market-leading franchises across communications, semiconductors, and software, and AVGO dominates the market for merchant silicon in wired networking. The demand for AI is expected to require significant high-speed networking and electro/optical networking capabilities, both of which are areas of strong leadership for Broadcom. Recently, company management highlighted that they estimate 2022 sales of Ethernet switch silicon deployed into AI use cases totaled over $200 million, a figure they expect to grow to well over $800 million this year. Generative AI is also driving the demand for computation offloading accelerators. This business achieved over $2 billion in revenue in 2022, and it is on track to exceed $3 billion in fiscal year 2023. We expect the company to continue to innovate and retain their leadership positions in these markets.

Given the pace of innovation and the rapid adoption of generative AI technologies, now is an exciting time to be an investor in technology companies. At Crawford, we are able to take advantage of these opportunities by identifying individual companies that both meet our quality requirements AND participate in these secular growth markets. While we are not thematic investors, we certainly seek to identify businesses that can benefit from larger trends in the economy.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-106

Generating Income and Exploiting Inefficiencies

Our Managed Income Strategy generates attractive, income-oriented returns with lower risk by exploiting these opportunities in higher-yielding securities.

Virtues and Constraints of High Quality Stock Ownership

It is rare to meet an investor who openly admits a desire to invest in low quality stocks.

Green and Growing Income

The consistency found within utilities is a function of the fact that it is a regulated industry that enjoys fairly constant and growing demand.