Was it Yogi Berra who said, “The best way to stay ahead is not to get behind?” He might have, but if so he would have been talking about baseball, not investing in stocks. His simple words of wisdom, however, are appropriate for this subject: downside protection in the stock market. One of the more favorable aspects of investing in dividend-paying stocks is their ability to help protect capital in declining stock markets.

For long-term investors, nothing disrupts investment returns like periods of significantly negative returns. Dividends can represent a meaningful offset to these periods because they assist in the powerful phenomenon of compounding. Albert Einstein once called compound interest the “eighth wonder of the world,” but for compounding to work to its fullest benefit, positive returns, or at least smaller negative returns, must occur year in and year out. The reason downside protection is so important is because of asymmetry and simple math. For a given percentage decline in portfolio value, the gain must exceed the loss to get back to even. For example, an investment portfolio that goes down by 30% has to increase by 43% to get back to the previous level of value. We believe that both Yogi and Einstein would agree that downside protection is an important consideration for investors.

Dividend-paying stocks have historically declined less when the market goes down. This has to do with a number of features of dividend-paying stocks, and three in particular:

- The simple fact that the return from dividends is always positive,

- Greater stability and profitability is typical of businesses that can sustain a dividend over time,

- Investor sentiment becomes more positive toward dividend-paying companies during a market decline.

There are two components of return from stocks: income and either appreciation or depreciation. If a company pays a dividend and is able to maintain it, the income portion of the return will always be positive. When all stocks are declining, the decline in dividend-paying stocks will be mitigated by the cash distributed to shareholders, which provides a cushion to the return each year. The amount to which the decline is reduced is dependent upon a number of factors, not the least of which is the amount of the dividend.

It is also significant that dividend-paying companies tend to have more stable underlying businesses. The implication is that a less risky company will imply a share price that is less volatile. Many of the traditional dividend-paying sectors of the market are thought of as less volatile than the average stock (e.g., Consumer Staples, Utilities, and Health Care). These businesses tend to be less volatile since their products are in continuous demand and are less influenced by the state of the economy. They reflect their more stable nature by having very strong and consistent dividend records, often with annual increases in the payout. These are thought of as “defensive” sectors, and typically they act as such in a market decline.

To the third point, investors tend to appreciate dividends more when markets decline and volatility is heightened. The reason for this is simple: the dividend component of return is always positive and people tend to appreciate certainty to the greatest extent in periods of instability. While we believe underlying company fundamentals are crucial to the success of any long-term investment, investor sentiment can have a significant effect on stock market returns. While we appreciate the dividend and maintain a consistent philosophy in all market environments, this tendency to seek assurance in times of market stress only further serves to reduce our strategies’ losses in a down market.

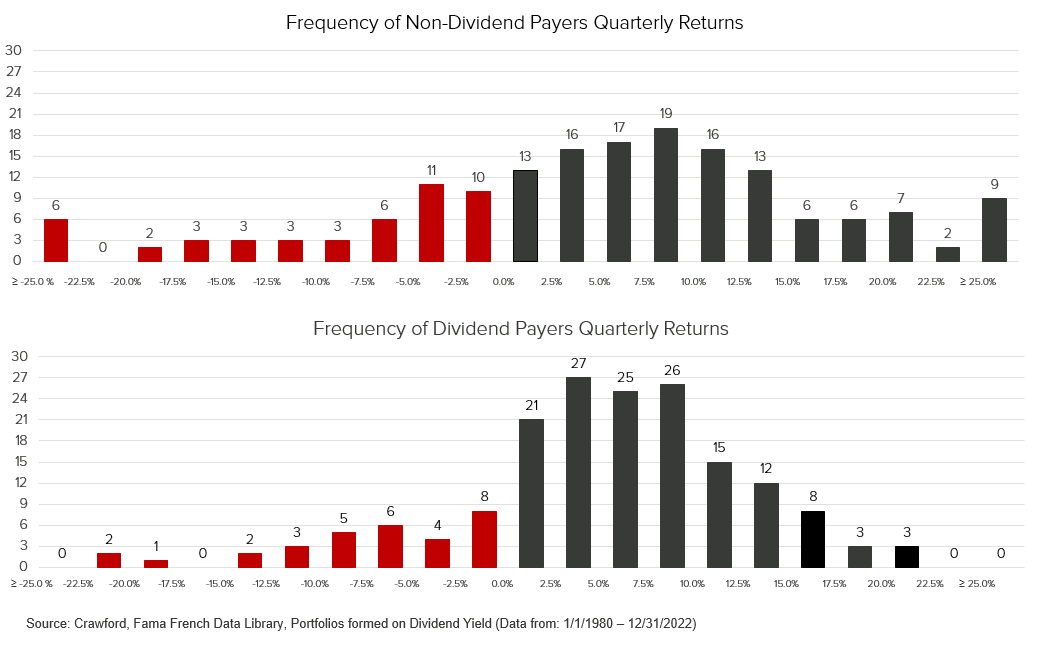

The Power of Protection. Over time, consistent dividend-paying companies have proven to be much better investments than companies with less-than- consistent dividends or none at all. We looked at the performance of dividend-paying stocks versus that of non-dividend-paying stocks since 1980, the year our firm was founded. What we found is that dividend payers experienced more months, quarters, and years of positive returns. As previously mentioned, the more frequently investments can earn positive returns, the greater the extent to which compounding can work wonders for a portfolio.

Of course, this means they experienced fewer periods with negative returns, as well. Dividend payers experienced 41 fewer months and 16 fewer quarters of negative performance than their non-dividend-paying counterparts, to be exact. Not only that, but the degree of decline between dividend payers and non-dividend payers was quite significant, as well. As previously mentioned, no two periods of negative returns are alike, and the greater the degree of negativity, the greater the required return to recovery. In quarters where non-dividend payers went down more than 10%, dividend payers outperformed by approximately 8%. This is a tremendous differential, given the power of reverse compounding. This vivid example represents a good part of the relative return superiority of dividend payers over the longer term.

Conclusion. It is difficult to overstate the importance of downside protection for a long-term investment program. We feel preservation of capital should always be a part of one’s investment goals. Investing in dividend-paying stocks, especially those that maintain and raise the dividend consistently, is an excellent way to achieve investment objectives. Dividends provide income, and as the dividends grow, they can force the price of a stock upward while protecting capital on the downside. Serious, long-term investors should carefully consider the merits of investing in companies that have the ability to pay dividends and raise them consistently.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-062

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

What is a Preferred Stock?

Preferred stocks are equity securities that are required to pay interest or dividends before common dividends are paid to common stockholders.

The Corporate Juggernaut: Can It Be Stopped?

Many observers of the stock market seem to be amazed at how well common stocks have done over recent years.