Dividend Integrity is the ability of a business to consistently pay, sustain, and increase dividend payouts to shareholders over time. We believe a company’s ability to do this is often indicative of business stability and underlying financial strength. Investing in companies of this nature is one of the hallmarks of our approach and a primary way we manage risk at Crawford Investment Counsel (Crawford). This is our preferred initial measure of quality. We believe Dividend Integrity is unique in that it favorably impacts return while also reducing risk. This orientation has led to both industry-leading risk management and loss mitigation in difficult market environments. Over time, these factors work together to produce positive alpha for Crawford’s strategies.

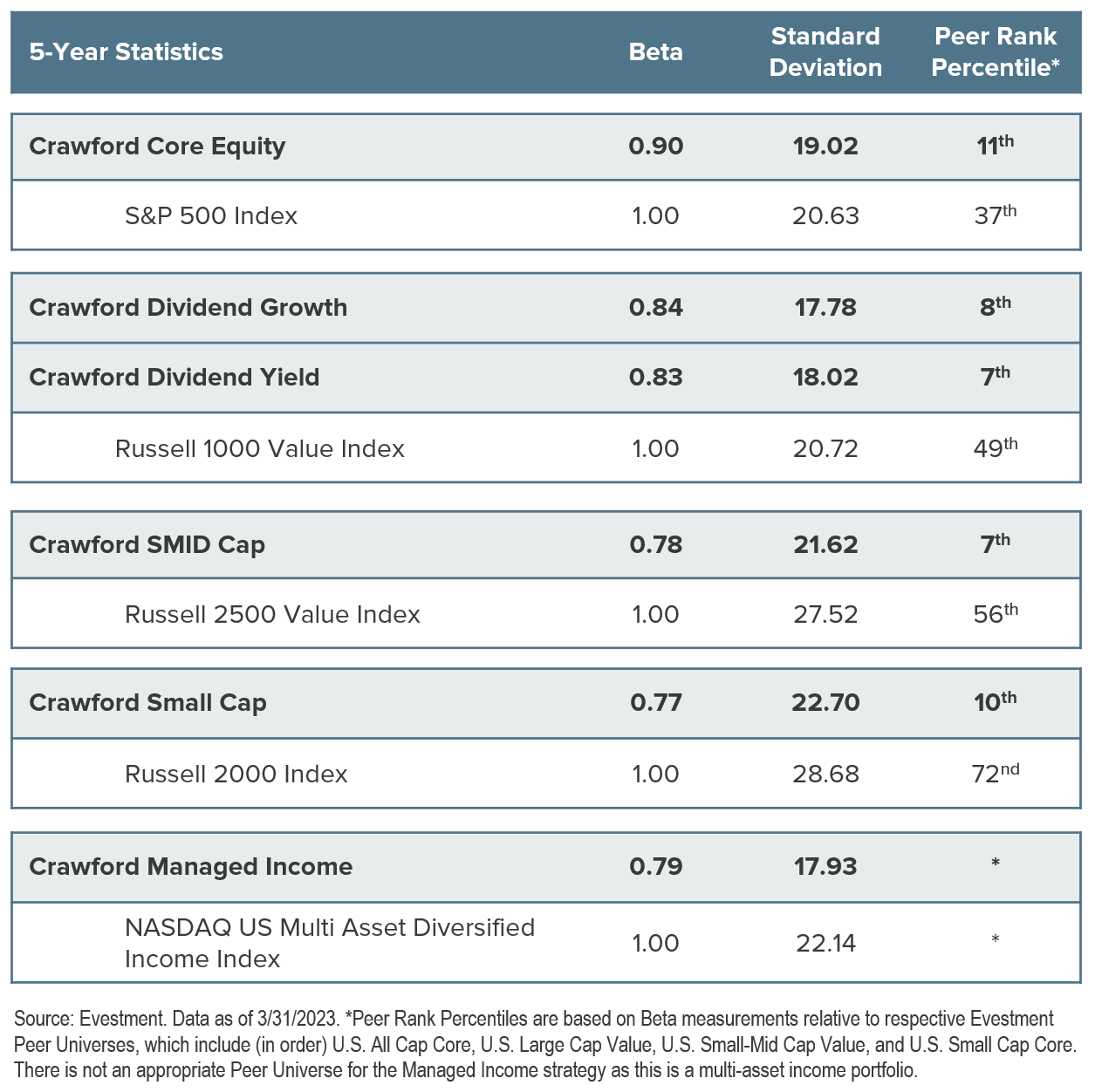

While Dividend Integrity is not the sole manner in which we manage risk, it is an important component. Again, it is the initial quality screen we run. Once we isolate companies with the ability and propensity to pay and increase dividends regularly, we then analyze other fundamental business characteristics, obtain a deep understanding of the business dynamics, and apply a price-sensitive and value-oriented stock selection process. Through this framework of investing in high-quality companies at attractive valuations, we narrow the range of investment outcomes, improve the chance of success, mitigate the likelihood of adverse returns, and enhance the return pattern. The table below quantifies the risk for Crawford’s strategies across several measures of volatility and displays a peer-ranked percentile (compares Crawford strategy to other actively managed portfolios with similar investment style characteristics).

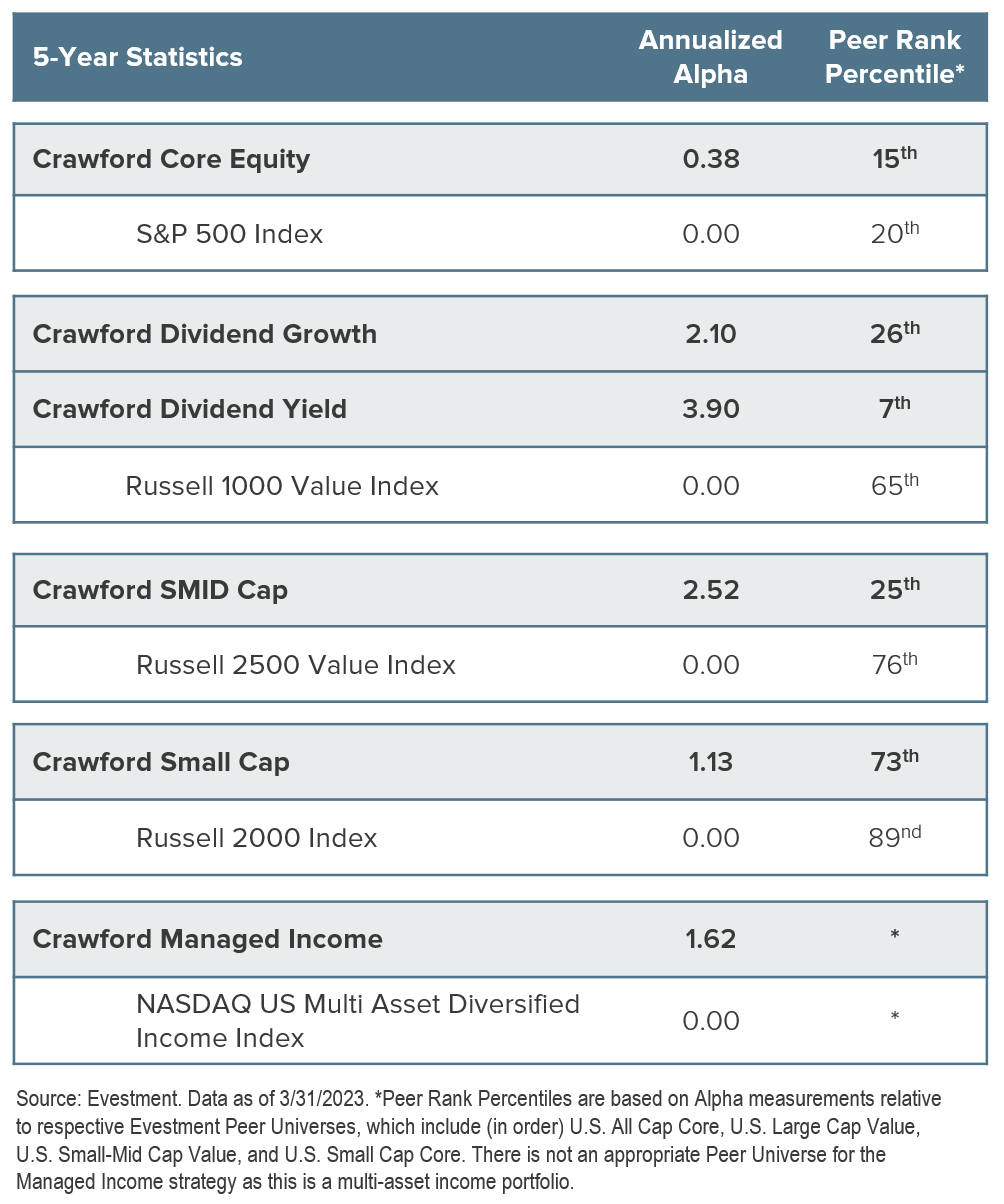

There is a commonly held assumption that higher risk, or more volatile (measured through beta) investments, should provide higher returns over time. The relationship between risk and return in investing as defined by CAPM has two primary components: beta and alpha. Beta (displayed in the table above) is the level of volatility, or risk, of any given investment relative to a benchmark. Beta for the selected benchmark is indexed to 1.00, and a lower beta indicates lower risk, while a higher beta indicates more risk. Alpha (displayed in the table below) represents the excess return earned per unit of risk taken. Alpha for the selected benchmark is always indexed at 0.00, and positive alpha indicates higher, risk-adjusted returns. Calculations for beta and alpha are always produced relative to a chosen benchmark. Academic research suggests that the presence of positive alpha is not sustainable, yet the positive alpha generation of Crawford’s strategies is persistent and meaningful when looked at in relation to the strategies’ primary benchmarks.

Crawford’s positive alpha indicates that our returns are stronger than the benchmark when the degree of risk taken is considered. In other words, we earn higher, risk-adjusted returns, or more return per unit of risk, and consistently add value above our benchmarks. This advantage is quantified by alpha, but it is realized to the greatest extent during periods of market distress. Hence, our conviction that our strategies provide “alpha when you need it most.”

Suffice it to say, the high positive alpha of our strategies is a result of both our industry-leading risk management and the edge we are able to gain through our in-house research and stock selection process. It cannot be emphasized enough that dividend-paying companies provide a lower risk method of investing, and when carefully selected utilizing a rigorous investment process, they can produce alpha. Focusing on Dividend Integrity and avoiding those companies who exhibit Dividend Hubris is an essential component of our philosophy at Crawford. We believe this approach should be employed over full market cycles, but today it is particularly timely.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. The Risk statistics presented above are shown as supplemental information to the equity composite disclosures regularly distributed by the firm. You can access Crawford's composite disclosures here.

CRA-23-107

Shining Light on Retirement Income

One of the significant, real-world issues with investing in retirement is consistency and reliability of income.

Book Review: The Deficit Myth

If you seek perspective on issues related to budget deficits, we recommend reading The Deficit Myth by Stephanie Kelton.

The Uncertainty of Investment Returns

As a stock market investor, there are few guarantees. However, we believe if one has a well thought out discipline and remains invested, suitable results follow.