At the end of 2020 there were over 10 million electric vehicles (EVs) in service globally. Remarkably, despite a pandemic-driven 16% decrease in global automobile sales in 2020, electric car registrations increased by 41%, reaching a 4.6% market share of vehicles sold. Driven by supportive regulatory frameworks (tax credits, emissions standards, and zero-emission vehicle mandates) and falling battery costs, these trends are likely to accelerate in the coming years. In fact, under the International Energy Agency’s “Stated Policies Scenario,” which incorporates all existing announced or legislated global policy ambitions, the global stock of EVs will grow from 11 million in 2020 to almost 145 million by 2030. This represents an annual average growth rate of nearly 30%, reaching annual sales of nearly 15 million vehicles in 2024 and over 25 million vehicles in 2030, representing 15% of all vehicle sales!

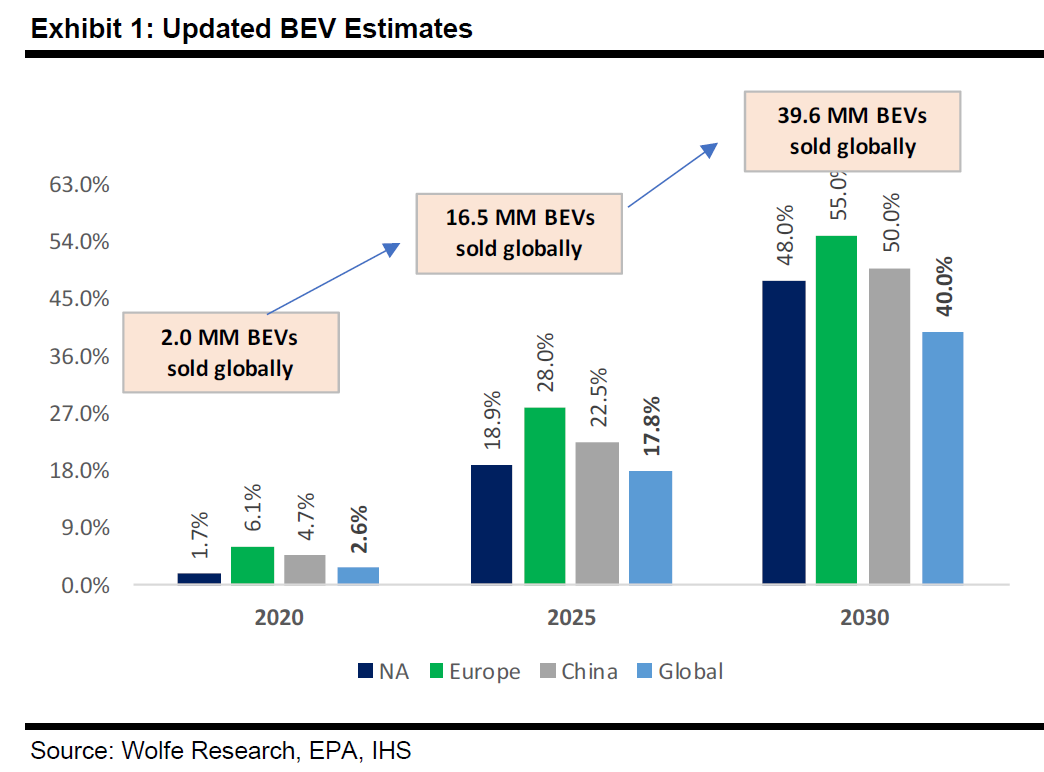

Wolfe Research paints an even more aggressive picture of the future for EVs. They forecast production of 17 million vehicles by 2025 and 40 million vehicles by 2030. This transition is to be supported by nearly $50 billion in CapEx and Research and Development spending by major auto manufacturers.

Given the global scale of this transition, how can investors take advantage of this opportunity? The implication and opportunity are far-ranging, spanning multiple industries and sectors. At Crawford Investment Counsel we focus on high-quality, more predictable, dividend-paying companies. These securities are combined into portfolios with the intent to deliver superior risk-adjusted returns, downside protection, and current income in order to deliver successful outcomes to our investors. Here are three examples of dividend-paying portfolio holdings that both meet our stringent investment criteria for quality, while also standing to benefit from the impending global transition to EVs.

TE Connectivity (TEL), 1.23% dividend yield, Core Strategy

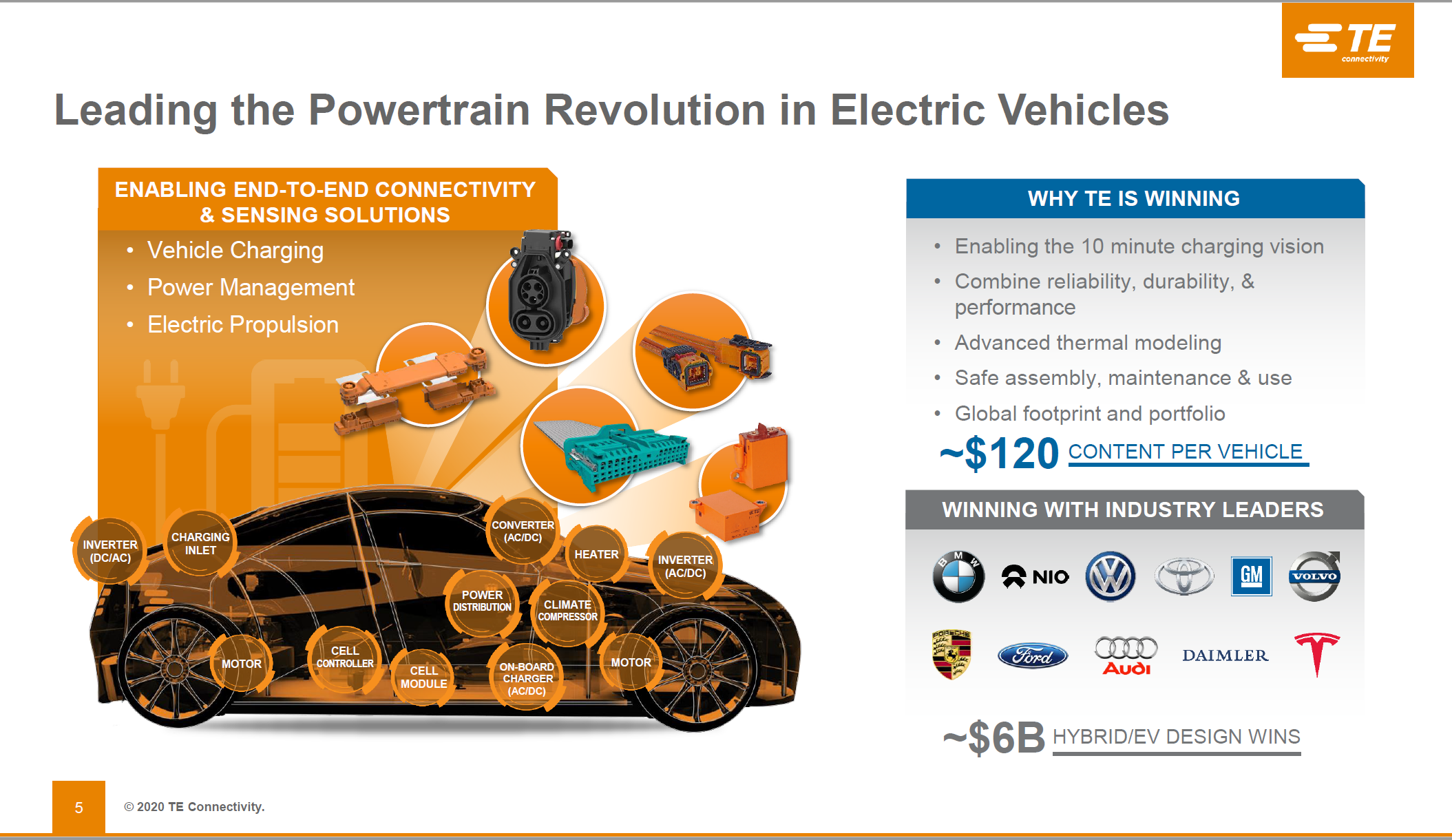

Self-described as an “Industrial Technology” company, TE Connectivity is well-placed to participate in EV transition alongside their automobile manufacturing customers. TE Connectivity enjoys the leading share (30-35%) in the automotive connectors market and generates 60% of sales from the Transportation Solutions segment. The company has over 4,000 engineers co-innovating with transportation customers on a daily basis to design components for tomorrow’s vehicles. With respect to EVs, TE Connectivity describes their solutions as the “stewards of the movement of an electron” – from charging inlets, to battery management and protection systems, and isolating high-voltage systems through motor connectivity and sensors. This is mostly layered on top of the needs they address in regular passenger vehicles including advanced driver assistance connectivity, infotainment connectivity, and normal, low-voltage systems. TE Connectivity’s “dollar content per vehicle” averages around $70 for a normal internal combustion engine vehicle and scales up to $180 for an average Tesla. In general terms, TE estimates a 2x uplift for an EV providing a long-term tailwind for above-industry growth. Driven by this exposure we expect that the company will be able to sustain strong revenue growth and profitability with additional leverage to any further acceleration in EV industry trends.

Source: TE Connectivity

Littelfuse (LFUS), 0.7% dividend yield, Core, Small Cap, and SMID Strategies

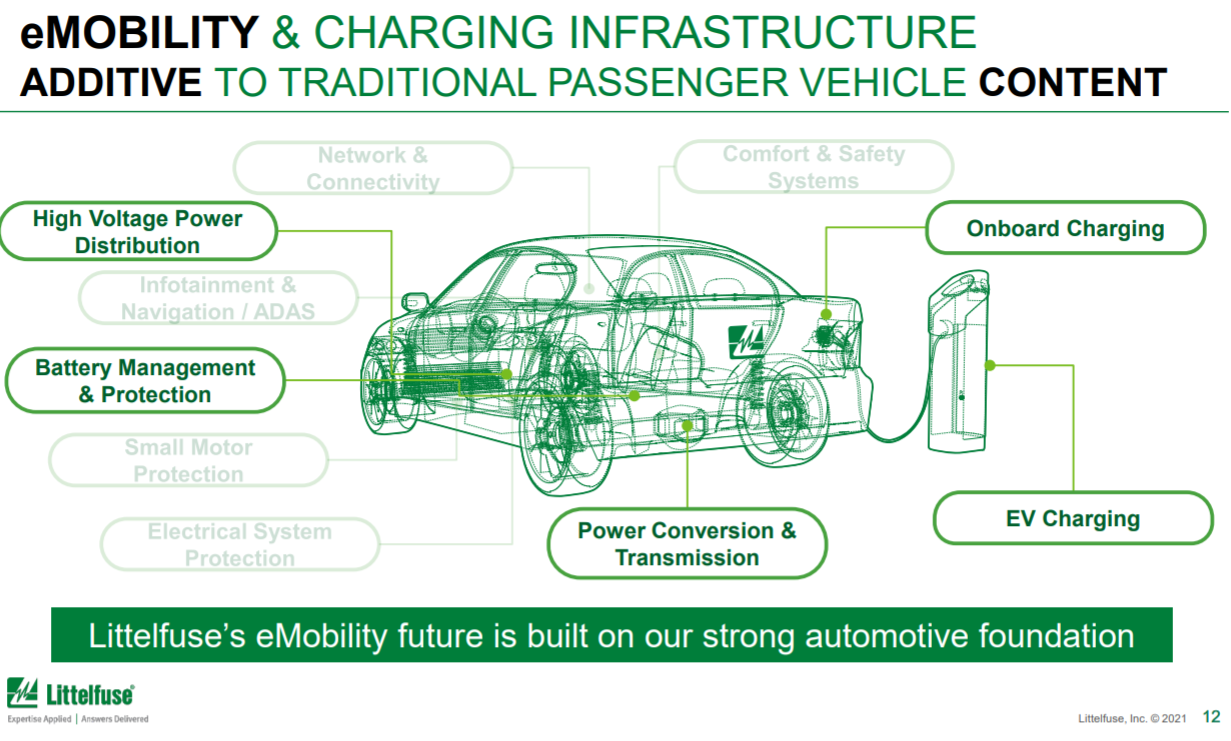

Littelfuse, Inc. designs, manufactures, and sells circuit protection, power control, and sensing products worldwide into automotive, industrial, medical, and consumer end markets. The company’s automotive product segment comprises about a third of total company sales and is expected to be a major contributor to corporate organic growth, rising at a high single-digit rate through 2025. Automotive growth and profitability catalysts include participation in the high-growth eMobility and commercial vehicle markets, growing content in EVs, and geographic expansion in Asia.

Source: Littlefuse

Standex (SXI), 0.9% dividend yield, Small Cap and SMID Strategies

Standex is an industrial conglomerate with 40% of company sales attributable to a range of electronic products. Through product development and acquisition, Standex has positioned itself as a valued supplier to BMW, Audi, Tesla, and other global EV manufacturers, and its content in these vehicles is currently 2x that on conventional engines. The company has indicated substantial growth over the past year in these highly profitable products, which is helping to support a low/mid-teens % profit growth outlook in coming years.

Source: Standex

Given the pace of change in the global vehicle markets and the rapid adoption of electric vehicle technologies, it’s an exciting time to be an investor in industrial and technology companies. At CIC we are able to take advantage of these opportunities by identifying individual companies that both meet our stringent quality requirements AND participate in these secular growth markets. While we are not thematic investors, certainly we seek to identify businesses that can benefit from larger trends in the economy. These investments can be found among many other high-quality equities in our Small Cap, SMID Cap, and Core Equity strategies. Other Crawford strategies have companies that will participate in EV proliferation to varying degrees, but their business mix is more varied or their participation a bit less direct.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. There is no guarantee of the future performance of any Crawford investment strategy. Material presented has been derived from sources considered to be accurate and reliable, but makes no representation thereof and accepts no liability or any loss arising from use or reliance herein. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy.

CRA-22-032

Innovation & Transformation: Investing in AI

Given the pace of innovation and the rapid adoption of generative AI technologies, now is an exciting time to be an investor in companies with AI exposure. At Crawford, we can take advantage of these opportunities by identifying individual companies that both meet our quality requirements AND participate in these secular growth markets.

Stocks: Rent or Own?

Today, many are effectively “renting” stocks in an attempt to create short-term trading gains, rather than owning equities for long-term total investment return.

Demise of the Mall

With the secular trend of e-commerce continuing to grow at the expense of traditional retail, we find what we believe is a long-term investable theme.