Defined contribution plans, more specifically 401(k) plans, have become the primary source of retirement savings for most Americans today. Workers are contributing more money than ever before, and employer-sponsored retirement savings plans represent over one-third of household financial assets. The advantages of these plans include tax-advantaged contributions and qualified, tax-free growth. With the importance and prevalence of workplace retirement savings plans increasing, along with the fact that plans are now providing investment options into the post-employment phase, the Department of Labor has made some recent policy shifts. These changes have important implications for both plan participants and sponsors. Specifically, there is a movement toward providing more insight into income and lifetime annuity assumptions to inform participants as to how their assets can produce income in retirement.

In order to implement Section 203 of the Setting Every Community Up for Retirement Enhancement (SECURE) Act, the Department of Labor (DOL) published an interim final rule effective September 18, 2021. The rule requires plan administrators of ERISA-defined contribution plans to express a participant's current account balance in two ways: as a single life annuity income stream and as a qualified joint and survivor annuity income stream. The purpose of the regulation is to help participants better understand how the amount of money they have saved so far converts into an estimated monthly payment for the rest of their lives and how it impacts their retirement planning. This rule is intended to help employees in defined contribution plans determine their readiness to retire and places great emphasis on lifetime income. These developments represent the most recent phase of the American corporation’s evolution from defined benefit retirement plans (pension plans) toward defined contribution plans (401(k) plans), as 401(k) providers will now need to begin thinking about providing true lifetime income options for employees.

In today’s world of ultra-low interest rates and record-high stock prices, retirees who remain in employer-sponsored plans will be seeking safer options that generate acceptable income, and plan sponsors will be required to comply by expanding their investment options. Generating income and attractive total investment return is what Crawford Investment Counsel (Crawford) has been focused on since day one. Crawford has a 40+ year heritage of providing clients with attractive total returns, reduced volatility, and income. We believe this is accomplished by investing in higher-quality, income-producing securities, being sensitive to valuation, and maintaining a longer-term investment horizon. We also believe that active management can provide an investment edge and help control risk.

We believe that when an investor needs to meet spending needs in retirement, both income generation and preservation of capital are critical to attaining a successful outcome. If spending needs are not met through income and capital appreciation, withdrawals can begin to encroach on the long-term principal value of a portfolio. At the forefront of any defined-contribution investor’s mind should be both a portfolio’s ability to retain and grow income over time and the threat of principal erosion or permanent loss of capital. This question becomes especially crucial as retirement gets closer.

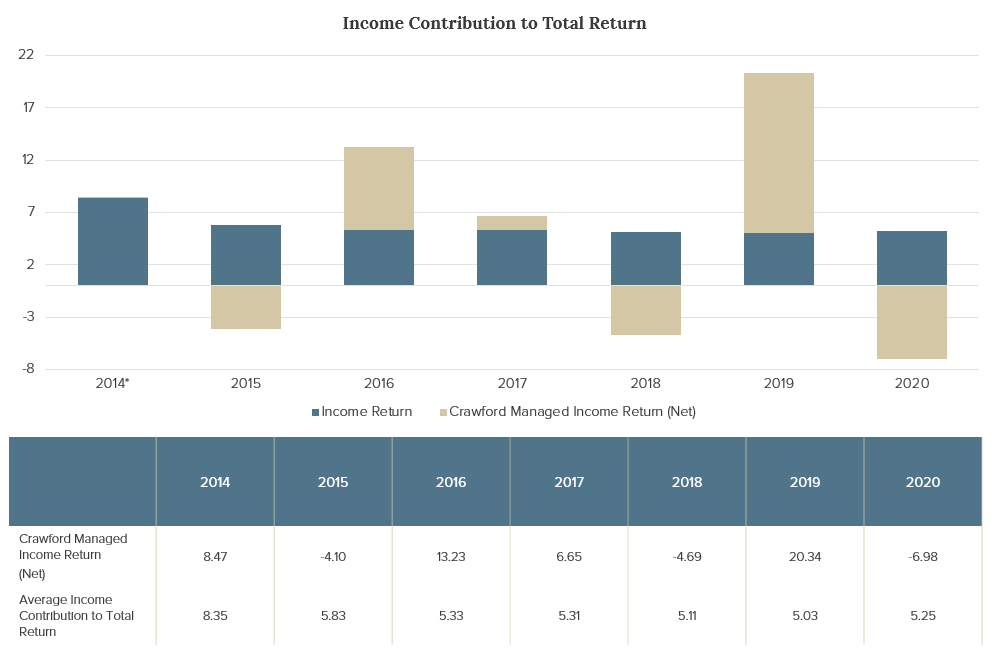

Since 2014, the Crawford Managed Income Strategy has offered its investors protection against both principal erosion and permanent loss of capital, while consistently generating over 5% yield for its investors. For a strategy of this nature, income is the primary investment objective. This is an actively managed portfolio that emphasizes steady and consistent income generation (yield) throughout market cycles. Volatility is part of investing, but this strategy seeks to mitigate the volatility of income by selecting higher-quality securities from the higher-yielding subsets of the capital markets. Steady income, even during adverse markets, protects investors while giving them the confidence to stay with their investment program over the long term.

In the Managed Income Strategy, we continually search for what we believe to be the highest quality securities available in the higher income subsets of the capital markets, while managing the portfolio to strike a favorable balance between current and sustainable income and risk mitigation. We believe that investors who are looking for current income in a lower-yielding environment often times seek yield by investing in lower-quality, high-volatility securities. Although those type of securities may sometimes be higher-yielding, many of these investors make tactical shifts based on bets about which direction certain macroeconomic variables will move, such as interest rates or energy prices. Crawford believes this is a poor risk/reward tradeoff, and instead builds a portfolio that pursues lower volatility through high-quality securities that aim to be risk-controlled with regard to macroeconomic variables. By focusing on risk control, the firm is able to build a portfolio with higher expected yield than the market, while avoiding the volatility typically associated with high-yield investing.

The Managed Income Strategy invests in dividend-paying stocks, real estate, energy infrastructure, preferred equity, and corporate bonds. The variety of income-producing asset classes utilized by the strategy allows its investors the opportunity to achieve greater diversification and in-turn, greater risk mitigation. We have identified four major risk categories including interest rate risk, energy price risk, stock market risk, and credit risk. What we’ve found is that, in this portfolio we can actually offset individual, security-specific risks against one another. Through a process of disaggregation and analysis of the various risks associated with specific holdings in our portfolio, we mitigate risk through diversification and balancing.

Essentially, we attempt to offset as much of the portfolio risk against itself as possible. For instance, we may control for interest rate sensitivity by offsetting Utilities with Regional Banks; Utilities are traditionally interest rate sensitive while Regional Banks tend to be interest rate sensitive in the other way. What you end up with is two sets of securities that provide handsome yield and possess opposite behavior patterns with regard to the factor of interest rates. In addition, concerning credit risk, energy risk, and market risk, we utilize a quantitative model and work to mitigate as much risk as possible while generating the income that we need.

Source: eVestment, Factset.

*Only 9 months of performance in 2014. Average Income Contribution to Total Return taken as an average of the reported monthly dividend yields during a calendar year. Past performance is not indicative of future results. The composite returns are shown as supplemental information to the Managed Income GIPS Composite Report.

We believe the goal of a successful 401(k) program should be to maintain portfolios with a balance between current yield, income quality (consistency), income growth, interest rate exposure, and risk. Since its inception, the Crawford Managed Income Strategy has done just this, while consistently providing a yield over of 5% for its investors.* For 401(k) participants seeking income, the Crawford Managed Income Strategy is an attractive solution, which can exist as a standalone strategy, part of a multi-managed daily valued income model, or as a complement to a more traditional mix of stocks and bonds. In today’s environment of low interest rates, the current yield that this strategy offers its investors certainly stands out.

*Using average annual quarterly yield since product inception.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

The opinions expressed are those of Crawford Investment Counsel Inc. Investment Team and are subject to change without notice. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Crawford Investment Counsel Inc. reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no guarantee that Crawford Investment Counsel Inc.’s assessment of investments will be correct. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not take into account specific client investment objectives.

CRA-21-395

Neutralizing Interest Rate Sensitivity

Given the potential for rising interest rates in the year ahead, the Crawford Managed Income Strategy is a compelling option for 401k participants.

Generating Income and Exploiting Inefficiencies

Our Managed Income Strategy generates attractive, income-oriented returns with lower risk by exploiting these opportunities in higher-yielding securities.

T-CRUTs After the SECURE Act

T-CRUTs can be a useful strategy that blend tax efficiency, income, control, and philanthropic intent.