There are few stocks that have been held for 41 years at Crawford Investment Counsel. One is Johnson & Johnson (J&J). Over this time, we have not always agreed with every decision made by management but remain invested because the strength of J&J’s franchises have led to consistent growth in profits and dividends. Recently, J&J made a significant announcement of its intention to separate their consumer segment to stand alone from the other businesses. While we do not necessarily fully agree with this decision by management, our investment thesis around J&J still holds.

The separation of its Consumer Products division will be done in a tax-efficient manner. The transaction is expected to be completed in late 2023 with more details forthcoming. While the Consumer Products division is only 16% of revenue and even less of operating profit, many of the company’s iconic brands – Tylenol, Band-Aid, Listerine, Zyrtec, Neosporin – will be in a separate offering.

J&J was founded on the idea of improving healthcare with its initial products being the mass production of sterile bandages. From its roots in sterile surgery, J&J grew into Consumer Products, Medical Devices, Pharmaceuticals, and Biotechnology products over the next 130+ years. Perhaps J&J’s greatest strength is management’s willingness to constantly transform itself by divesting underperforming businesses and acquiring new businesses. In this way, J&J acts as a healthcare conglomerate rather than a single entity company. Part of investing in J&J stock is ceding some control to the management team to make decisions with regards to investing capital in various sub-sectors in healthcare in order to achieve the best long-term returns.

Our opinion is that management’s operational discipline and capital allocation has been efficient in turning around the Consumer Products division in the last decade. On January 15, 2010, the FDA issued a warning letter to J&J regarding manufacturing deficiencies in its McNeil consumer plant, resulting in massive recalls in Tylenol, Motrin, and Benadryl products. This was a self-inflicted setback that was much more difficult to overcome than the Tylenol tampering scandal in the early 1980s. Over a period of several years, J&J fought back from these manufacturing problems, re-instating trust in its larger consumer brands. Over the long term, management has successfully deployed capital into their Consumer Products division with acquisitions of Tylenol (1959), Motrin (1984), Neutrogena (1994), Aveeno (1999), Listerine (2006), Zarbee’s (2018), and Dr. Ci:Labo (2019). As investors, the Consumer Products division’s ability to fight back operationally, position in a market ripe for additional capital investment, and durable long-term brands, make it a business J&J should continue to own and operate, in our opinion.

So why are we continuing to invest in J&J despite what we view as a management misstep? Our investing philosophy is to find quality companies that pay consistently increasing dividends so that we can enjoy compounding growth over the long term. J&J has satisfied this for more than 40 years. In fact, J&J has one of the most prolific long-term records of compounding returns for investors, and we continue to believe that the combination of their area of focus, balance sheet strength, and long-term orientation will reward shareholders in the future.

J&J’s share price has outperformed the S&P 500 since Crawford Investment Counsel’s founding in September 1980. If $100,000 were invested in J&J shares on October 1, 1980, that amount would be worth $9.9 million at the end of 2021, versus $3.8 million for the S&P 500.

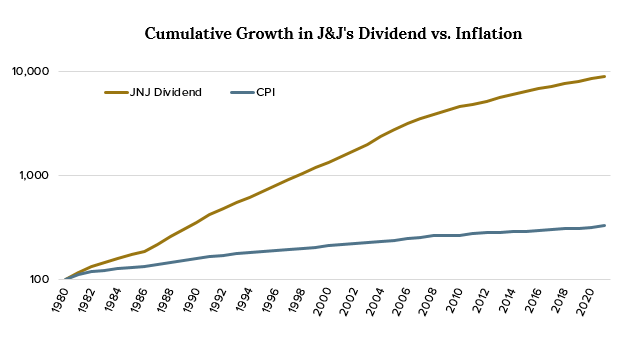

More impressive is J&J’s dividend track record, as the dividend provides income for investors. The first full year after investing (1981) the annual dividend income was $3,095, which grew to $243,605 in 2021. This dividend income is almost five times greater than the original investment would have received from dividends from the S&P 500 in 2021 of $50,403. Below is a chart showing the annual growth in J&J’s dividend versus inflation. It is easy to see that a J&J investor with income needs would have vastly outperformed inflation, with the J&J income stream growing more than twenty-five times greater than inflation. There are very few better examples of compounding dividend growth leading to higher income.

Source: Crawford, Factset

Source: Crawford, Factset

In addition to any conversation about the Consumer Products Division, we also are bullish on J&J’s other businesses, especially its Oncology and Immunology franchises within the Pharmaceutical division. J&J has long followed a business model that allows for both internal and early business development to bring new drugs to market. J&J invests almost $10 billion annually on drug discovery. Almost half of its innovation comes externally, demonstrating the value the company brings to smaller innovators in helping to clinically develop products. J&J's Pharmaceutical division is growing more than twice that of the industry, and the growth is largely attributed to volume, with very little due to price increases.

We expect that J&J will follow through on its consumer division spin. Despite not fully agreeing with all management decisions, we remain steadfast in our belief of the power of this company to continue to compound returns and raise dividends for investors. Our diligence and monitoring will continue, including whether to participate in the soon-to-be spin as a standalone investment for Crawford Investment Counsel clients.

Why do we view Johnson & Johnson as QUALITY? Johnson & Johnson leads healthcare with 59 consecutive years of dividend growth. Over two-thirds of revenue is generated from products that lead their respective categories. J&J is also one of only three companies with an “AAA-rated” balance sheet.

How do we view Johnson & Johnson’s VALUATION? Johnson & Johnson is currently trading at an approximate 20% discount to the market (S&P 500) on both earnings per share and enterprise value to EBITDA. The company also boasts a dividend (2.5%) that is almost twice that of the S&P 500 (1.3%).

Why is Johnson & Johnson in the portfolio? Johnson & Johnson’s diversified business model (Pharmaceutical, Medical Devices, and Consumer) is unrivaled in healthcare and typically allows for more consistent growth. There is potential upside to current forecasts from a more robust, long-term pharmaceutical pipeline, continued cost reductions in medical devices, and further acquisitions to drive growth in Pharma and Consumer.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. There is no guarantee of the future performance of any Crawford investment strategy. Material presented has been derived from sources considered to be accurate and reliable, but makes no representation thereof and accepts no liability or any loss arising from use or reliance herein. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy.

The S&P500 Index is the Standard & Poor's Composite Index and is widely regarded as a single gauge of large cap U.S. equities. It is market cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization.

CRA-22-031

The Long-Term Destruction of Income: What To Do?

John Maynard Keynes was a 20th Century economist most famous for his work on economic cycles

Can Cryptocurrencies Pay Dividends for Investors?

The recent surge in cryptocurrencies has many wondering if they should join the rise.

Interview with Jon Christiansen, CFA: Dividend Growth Portfolio Manager

Interview with Jon Christiansen, CFA: Dividend Growth Portfolio Manager