BACKGROUND. Since the Global Financial Crisis (GFC) and Recession of 2008-09, structural changes in the U.S. high-grade bond market are exposing passive fixed income investors to a heightened level of interest rate risk. Characteristics typically associated with the composition of the bond market, including: size (PAR value outstanding), credit ratings, average coupon, and maturity length, have been influenced by the nature of the crisis and the monetary and fiscal policies enacted to encourage economic recovery. One of the most profound changes in market structure impacted by the recovery is the increased maturity length of the bond market. We believe this represents a risk which may go unnoticed, but deserves to be fully understood. We find this to be particularly true for investors acquiring their fixed income investment exposure passively through instruments like mutual funds and exchange traded funds (ETFs), which are intended to replicate the composition of the bond market.

CAUSE. The economic recovery and expansion period following the GFC was the longest U.S. growth cycle in modern history. Its length was attributable, in part, to the time needed for recovery due to the severity of the financial crisis. It was also, arguably, due to the comparatively benign level of fiscal response enacted by the Federal Government (e.g., T.A.R.P, and the American Recovery and Reinvestment Act), and the nature of the extraordinary monetary stimulus measures enacted by the Federal Reserve (e.g., zero-bound interest rate policy [Dec. 2008 – Oct. 2015], quantitative easing I, II, and III, and Operation Twist). Monetary policy actions were unparalleled in terms of scale and scope, from a historical perspective. They had the effect of both suppressing short-term interest rates and influencing long-term rates lower, as real market yields projected a low Federal Funds rate into the future, and the traditional “term premium” which compensates investors for the uncertainties associated with longer duration securities was effectively nullified. Irrespective of the arguments touting the success or failure of Federal Reserve actions, a tangible consequence of interest rates remaining low for an unprecedented length of time was an exponential increase in bond issuance.

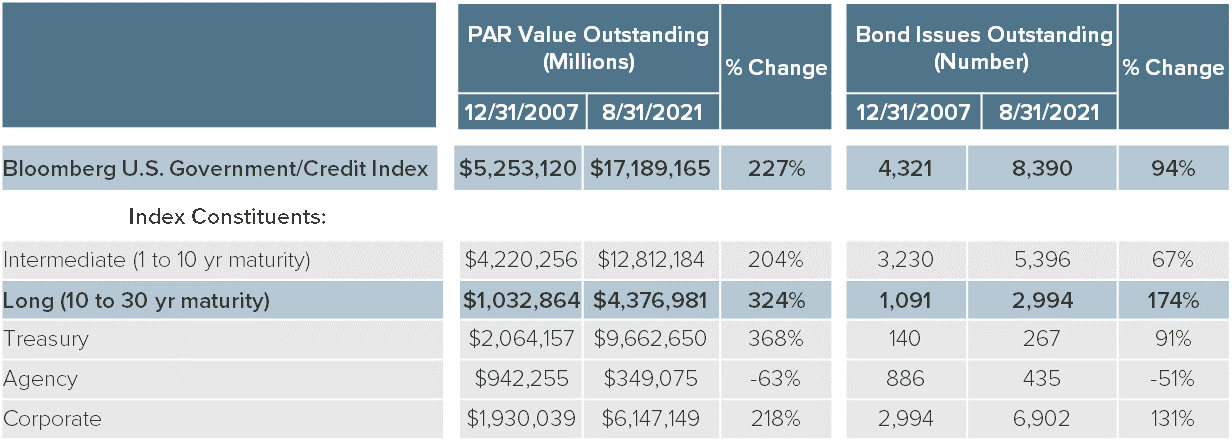

EFFECT. Historically low interest rates lasted a remarkably long time following the GFC. This fostered a ripe environment for bond issuance across fixed income sectors. The data in the table below illustrates structural changes in the high-grade bond market as seen through the agnostic lens of the Bloomberg (formerly Barclays) U.S. Government/Credit index. This index is intended to be an unbiased reflection of the U.S. Treasury, Government Agency, and Corporate bond sectors. It represents investment-grade issues 1 to 30 years in maturity length with over $300 million in PAR value issued and outstanding. The dramatic increase in the PAR value and number of bond issues outstanding between December 31, 2007 (pre-GFC) and the most recent month-end, are testament to the influence of the rate environment over that period.

Source: Bloomberg (Data Through: 8/31/2021)

It is particularly interesting to note the increase in the Long-Term portion of the Index, which substantially outgrew the Intermediate-Term portion on a percentage basis. This largely reflects issuers taking advantage of the low rate environment to lock-in long-term financing.

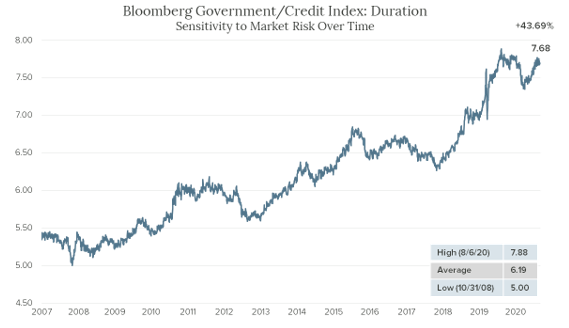

IMPACT. For passive fixed income investors focused on simply tracking the overall bond market, post-GFC changes in the composition of the funds and ETFs meant to reflect the index are profound. For example, if a passive investor purchased an ETF which mimics the Bloomberg Government/Credit Index at the beginning of 2008 with the belief the duration (sensitivity to interest rate risk) of the portfolio would remain within a reasonably narrow range, they may feel very differently now given their increased exposure to market (interest rate) risk. With the post-GFC increase in the amount and proportion of long-term securities represented in the index, the sensitivity to market risk (portfolio duration) has increased substantially, as demonstrated by the following graph:

Source: Bloomberg, Bloomberg U.S. Agg Gov/Credit Statistics Index, Daily (Data Through: 8/31/2021)

This graph illustrates a 43% increase in interest rate risk which grew steadily higher over the course of the post-GFC era. The question posed to the investor now is whether that is an acceptable level of risk exposure given their investment objectives, and in view of the potential for higher interest rates going forward. As rates move higher, instruments like the ETF mimicking the Bloomberg Government/Credit Index are exposed to a higher level of price downside risk relative to lower duration strategies.

RESPONSE. We believe it is an appropriate time for the passive index investor to consider declaring victory by locking-in gains enjoyed from good performance earned over the course of the post-GFC era. We also encourage investors to transition to a more dynamic active management approach in order to navigate the potential challenges ahead posed by an increasing rate environment. This is precisely the approach we employ in managing fixed income portfolios at Crawford Investment Counsel, Inc.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-224

Interview with Boris Kuzmin, CFA: Small Cap Portfolio Manager

How did you first get interested in small cap investing, and how has that developed in your time at Crawford?

Is Your Portfolio Ready for Winter?

Currently, there is a dramatic shift occurring in the global financial markets. Unlike a fantasy novel, it is not as definitive as the first snowfall.

The State of the Consumer

At Crawford Investment Counsel (Crawford), we believe the financial condition of the U.S. consumer has rarely been better.